Should I Pay Off My Student Loans?

Is paying down your loans while payments are suspended the best use of your dollars?

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

A version of this article appeared on Oct. 29, 2020.

On April 6, President Joe Biden made it official: Student loan payments are paused through August 2021.

The reprieve on federal loan repayment began back in March 2020 as a feature of the CARES Act. It temporarily set interest rates to 0% and suspended loan payments and collections on all federal student loans through Sept. 30, 2020. (This FAQ on the website explains how the current, automatically granted payment suspension works and which loans are eligible.)

As the pandemic intensified and unemployment numbers rose, the Department of Education extended student loan payment through the end of 2020, and then again through Sept. 30, 2021. As that deadline loomed, however, the DOE said it would issue a final extension through Jan. 31, 2022.

The DOE's action provides some much-needed relief to those who've lost their income in the current pandemic. But if you're in the fortunate position of still being able to make regular loan payments, what should you do with the money? Should you keep paying your student loans, even though no payment is due?

The Pros of Continuing Your Payments If you continue to make your regular payments while interest is not accruing, your payments will be applied directly to the principal balance. (Tip: Be sure to clarify your intention to apply the full payment to principal with your loan servicer.)

This will provide a big leg up when it comes to repaying that loan—not only will you possibly be able to retire the loan ahead of schedule, you will end up paying a lot less interest over the life of the loan. (Also, per the studentaid.gov website, any loan repayments made during the suspension-of-payments period can likely be refunded if need be; contact your loan servicer for more information.)

But though there are clear advantages to continuing to pay your student loan, doing so may not be the best use of the extra cash in your budget. It's a concept in finance called return on investment: Carefully consider all of the things you could do with that money in your budget right now.

Is There a Better Use of the Money? Let's run through some ideas to get the best bang for those student-loan payment dollars, depending on your own financial situation.

1. Save An Emergency Fund If you don't have an emergency fund, set aside a few months' worth of would-be student loan payments to create one.

As my colleague Christine Benz explains, emergency funds are crucial, regardless of life stage or situation. If there’s one thing 2020 taught us, it’s to expect the unexpected. Whether it’s a home repair, out-of-pocket medical expense, or job joss, having a substantial cash cushion on hand will save you from needing to finance big expenses with high-interest credit cards or loans from retirement accounts. And, as Benz advises, keep in mind that the greater your fixed expenses and the harder your job would be to replace (because it's specialized and/or higher-paying), the larger your emergency fund needs to be.

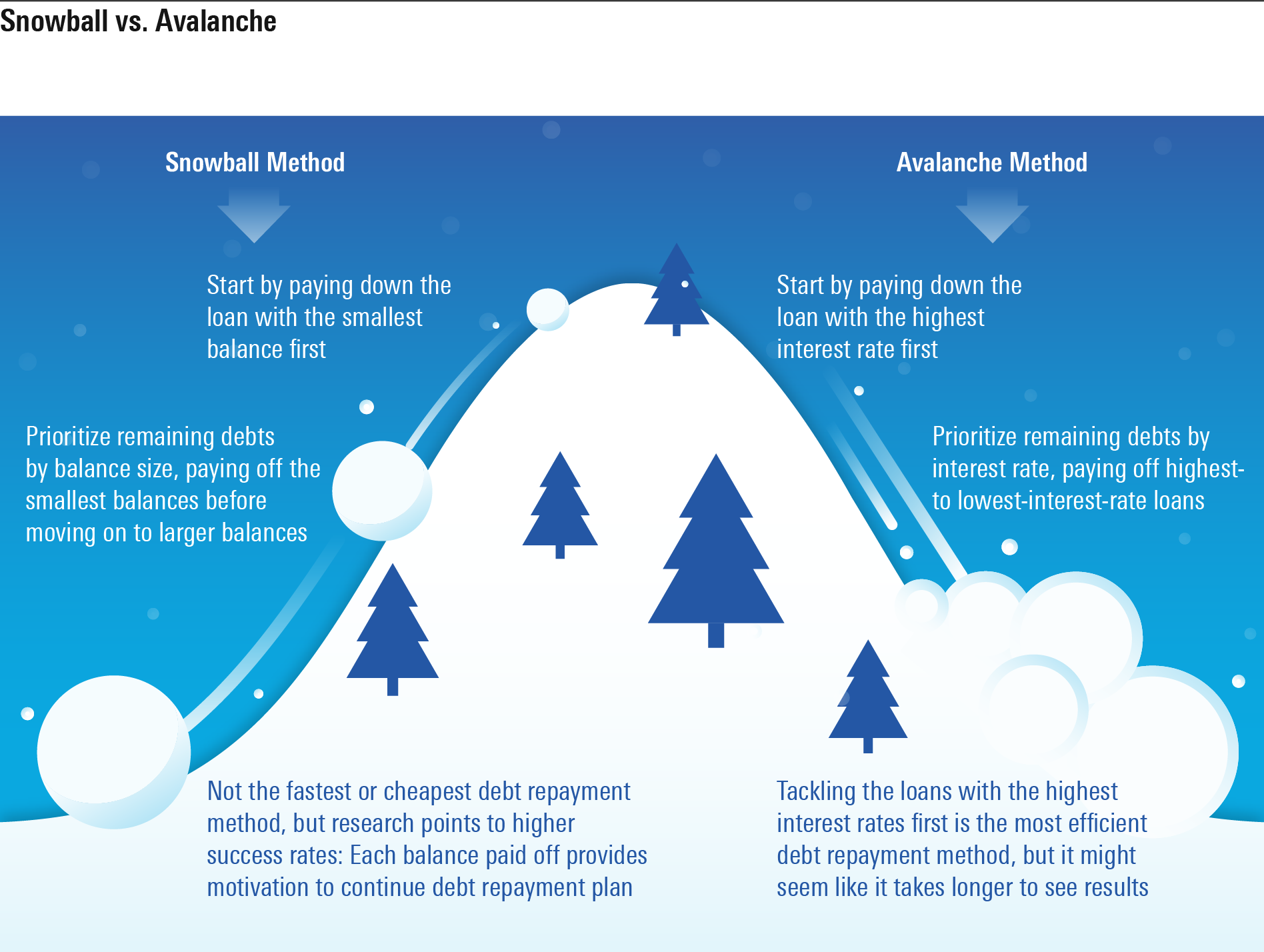

2. Start a Debt-Repayment Plan There are two well-known debt-paydown strategies, the "snowball" and the "avalanche." They both require that you pay at least the minimum due on all your debts every month because missing payments can wreak havoc on your credit score. On top of that, you focus the extra cash on paying down the principal of one loan at a time.

- The "snowball" method. You prioritize paying off the loan with the smallest balance first, regardless of interest rate. You then move on to the loan with the next-smallest balance.

- The "avalanche" method. You focus on paying off the loan with the highest interest rate first, then the loan with the next highest interest rate, and so on. There are pros and cons to each. The avalanche method ensures that you pay the least amount of interest possible. It's the cheapest way to retire your debt, but it's not necessarily a slam dunk for everyone.

If the early wins you get from paying off your smallest balances first provide the necessary motivation for you to see your debt-paydown program all the way through, then the snowball method is the better choice for you.

While I understand the appeal of the snowball, I'm personally #TeamAvalanche when it comes to high-interest-rate credit cards. The average rate charged by credit cards in the U.S. is 15%, according to Federal Reserve data; balances compounding at this rate have the potential to grow like weeds. If you have very high-interest loans (with APRs in the high teens and 20s) I would prioritize paying them first.

3. Take Full Advantage of Your Retirement Plan Some people might think it's counterintuitive to invest money while you owe money. Shouldn't you just pay everything off first, then invest? Again, the answer is that it depends on where you can get the best bang for your buck.

Once you’ve tackled any high-interest debt, consider the rate of return you could earn by investing in the market. Over the past 100 years, stocks (on average) have grown 7% per year on an annualized basis, after inflation. If you start regularly investing small slices of your paycheck compounding at a rate of 7% per year for decades, that is an extremely powerful wealth-building tool.

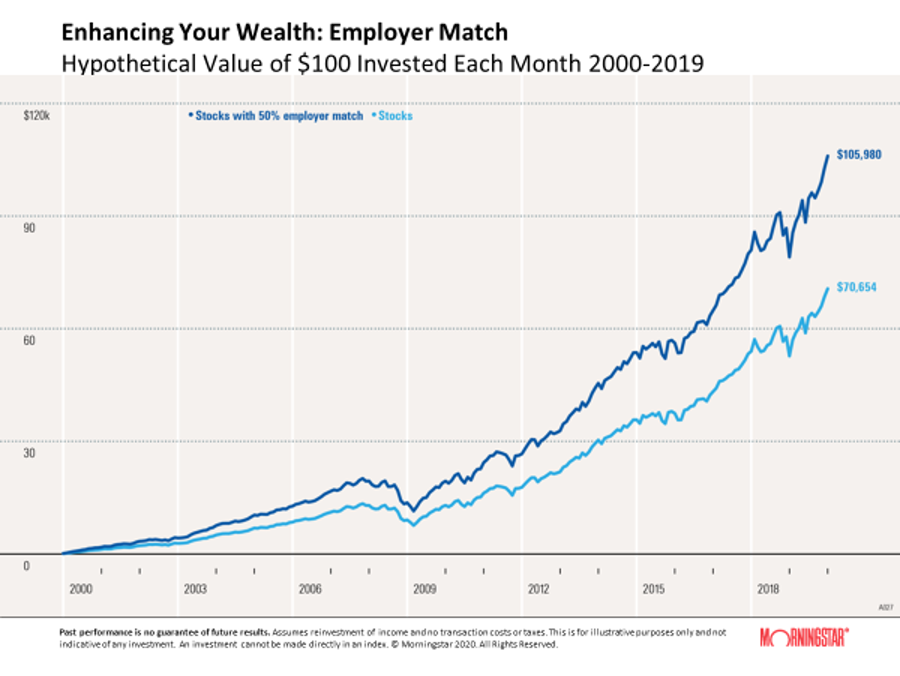

Also note that if your employer offers to match any portion of your retirement plan contribution, you should grab that free money. The image below shows what a big difference the match makes.

The light blue line shows the growth of $100 invested in stocks at the end of each month. The dark blue line represents the same investment with a 50% employer match. (In other words, $150 invested each month as opposed to $100.) Because investment returns grow exponentially and not in a linear pattern, funding your retirement account with as much money as early as possible gives you the best growth potential.

In short, paying off your student loans is a good idea, but you might get an even bigger financial benefit in the long run from applying extra cash toward shoring up an emergency fund, servicing an even higher-interest-rate loan, or saving more for retirement.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KWYKRGOPCBCE3PJQ5D4VRUVZNM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TZEZ6FJNTZEZRC3FBWCWXTXVOQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)