10 Newest Stocks in the Wide-Moat Focus Index

The Morningstar Wide Moat Focus Index made room for some undervalued consumer defensive stocks in June.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

Every quarter, we reconstitute one subportfolio of the Morningstar Wide Moat Focus Index. When we do this, we re-evaluate the index's holdings and add and remove stocks based on a preset methodology. This helps keep the index true to its aim of providing exposure to competitively advantaged (wide-moat) stocks selling at the lowest current market price/fair value ratios.

The index consists of two subportfolios with 40 stocks each, many of which are overlapping positions. The subportfolios are reconstituted semiannually in alternating quarters, on a "staggered" schedule. Because stocks are equally weighted within each subportfolio, the reconstitution process also involves right-sizing positions.

The Adds After the June reconstitution, half of the portfolio swapped out 10 positions. The index now holds 46 positions.

One discernible theme is that wide-moat consumer defensives look cheap. Companies like

As our consumer sector equity analysts wrote at the end of the second quarter, as sales have continued to languish, consumer product firms are using mergers and acquisitions to drive growth. For instance, General Mills, one of the new positions in the portfolio,

a few months ago.

Cost pressures also continue to weigh on consumer product firms. Even though these operators have focused on cutting costs and improving efficiency over the past few years, inflationary headwinds in the form of increased freight costs and rising commodity prices continue to eat into profits.

These pressures have helped create opportunities for long-term investors who want to build positions in these competitively advantaged names.

Likewise, utilities such as

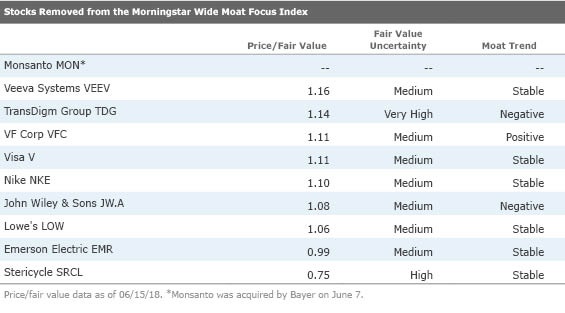

The Drops On the flip side, 10 stocks were removed from the index.

Eight of the stocks were removed because their price/fair value ratios rose beyond our buy range.

There were two special cases among the removals this month: Monsanto was acquired by

the firm's core domestic med-waste operations still enjoy robust competitive advantages rooted in route density. However, changes in healthcare end markets over the past decade (namely consolidation of independent healthcare practices into larger hospital groups) have reached the point where Stericycle is seeing a large portion of its small-quantity account pricing materially bid down. Stericycle isn’t losing its footing against its small regional peers, but profitability concerns keep us from comfortably making the call that excess returns are more likely than not to remain for at least 20 years, the definition of a wide moat, Young said.

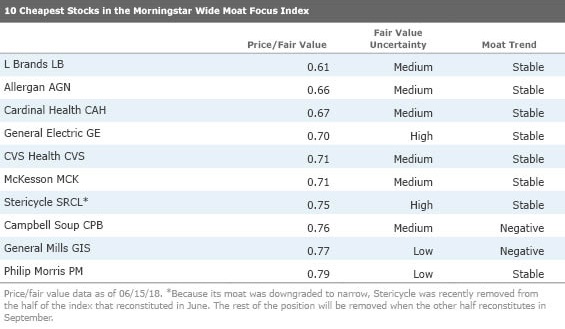

High-Quality Stocks in the Bargain Bin The table below lists the 10 cheapest stocks in the index, ranked by price/fair value. The median stock in the Wide Moat Focus Index is trading at a weighted average price fair/value of 0.84. By comparison, the broad Morningstar US Market Index is fairly valued, trading at a weighted average price/fair value of 1.0.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Neither Morningstar, Inc. nor its investment management division markets, sells, or makes any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)