A New Approach to 60/40

And no, it’s not 80/20.

/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)

Much ink has been spilled declaring the demise of the traditional 60/40 portfolio. We have recently published analyses on how investors might rethink traditional approaches to diversification. We’ve also found that there have been few better alternatives to the classic.

But this is not a commentary about the alternatives to a 60/40 allocation to stocks and bonds. Rather, this is a look at a “new” way to keep the tried and true 60/40 exposure in place and still have money left to potentially add even more value. The long-term efficacy of the 60/40 portfolio is indisputable, but so is the tendency of investors to get anxious owning this mix during a period when both bonds and stocks are down, and to fret over whether the prospective returns on offer from stocks and bonds today will be enough to get them to their goal.

Investors who want something more than 60/40 can explore the WisdomTree Efficient Core funds, which use U.S. Treasury futures to obtain leveraged fixed-income exposure. This frees up cash for further diversification or hunting for alpha on top of WisdomTree’s take on the classic 60/40.

How Does it Work?

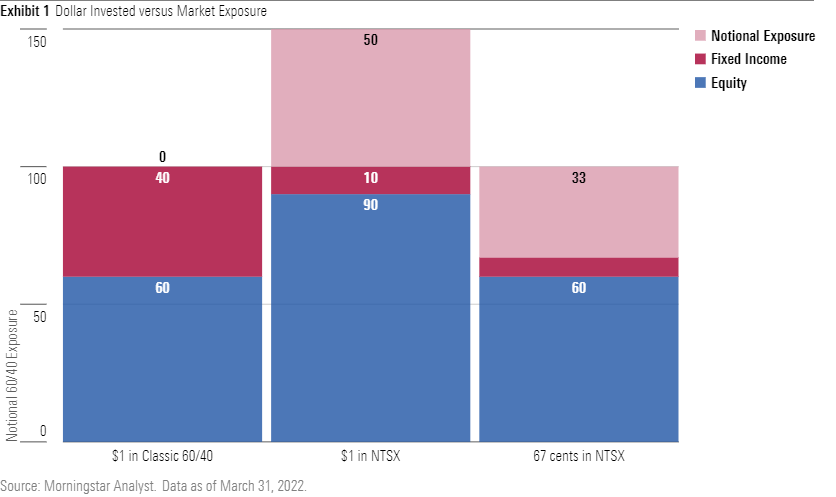

The mechanism is straightforward: For every dollar invested, the fund pays 90 cents for equity exposure and invests 10 cents to collateralize 60 cents worth of notional exposure to U.S. Treasury futures. With leverage, the portfolio’s 60/40 exposure jumps 1.5 times to 90% stocks and 60% Treasuries. This leverage can allow investors to get full exposure to a 60/40 allocation by investing just two thirds of their assets in the 90/60 portfolio. This frees up one third of their money for other uses, such as adding diversifying or alpha-generating assets.

Exhibit 1 plots the total market exposure (including leverage) for money invested in a classic 60/40 portfolio versus the WisdomTree U.S. Efficient Core Fund NTSX.

It is important to note that these funds only have exposure to U.S. Treasuries in their fixed-income sleeve. Investors in a classic 60/40 portfolio can hold a wider array of options that include corporate bonds, and mortgage-backed and asset-backed securities.

This idea isn’t entirely new. Institutional investors have long used leverage to gain exposure to the broad equity or fixed-income market with the hopes of generating alpha with the unlocked assets. However, the WisdomTree funds only aim to provide leveraged exposure to a 60/40 portfolio. How any freed-up funds are used is entirely up to the end investor.

The Nuts and Bolts

WisdomTree currently offers three versions of this strategy, each with a different geographic focus for their stock sleeve. The lineup features the U.S. Efficient Core Fund NTSX, the International Efficient Core Fund NTSI, and the Emerging Markets Efficient Core Fund NTSE. They all share the same structure outlined above. Their differences are limited to the makeup of their stock exposure.

These funds’ equity sleeves mimic the indexes representing each region: the S&P 500 for NTSX, the MSCI EAFE Index for NTSI, and the MSCI Emerging Markets Index for NTSE. Currently, NTSI and NTSE hold representative samples of their target indexes’ portfolios, owing to their smaller asset bases and wider benchmark universes.

The bond sleeve for all three funds consists of a ladder of U.S. Treasury futures with different maturities. The Treasury futures market has ample trading volume and liquidity, which closely aligns its performance with the spot market. The portfolio managers adjust the fund’s exposure to Treasury futures at different maturities to replicate the duration of a typical broad aggregate bond index, such as the Bloomberg U.S. Aggregate Bond Index.

The futures contracts are offered on a quarterly schedule and are rolled forward as they approach expiration. Futures margin, which is a collateral deposit on the contracts, typically represents around 3% to 12% of the notional value of the exposure. This is lower than securities margin, which represents ownership of the underlying stock, bond, or exchange-traded fund, and requires up to 50% of the face value of the position.

Maintenance margin comes into play as the futures contract’s value changes over time. Futures settle and are marked to market at the end of each trading day. Daily losses on the contract’s notional value are taken out of the initial margin funds while gains are added. More cash must be added once the balance breaches the maintenance margin level, which is about 10% below the initial margin requirement. This means that the leveraged exposure to the asset can change as the contract value drops and more cash must be added. Cash management could lead to marginal differences between the actual performance of the fund and a simple 1.5 multiple of the returns on a 60/40 portfolio.

The funds follow a quarterly rebalance schedule but also rebalance whenever their asset class exposure deviates more than 5 percentage points from the target allocation. Typically, the bond sleeve is adjusted, as trading in and out of the stock positions is more complicated and might trigger capital gains.

The “L” Word

It is important to address the elephant in the room. Leverage has a bad reputation. Furthermore, the complexities of derivatives and their response to market volatility can be a source of risk.

To the first concern, Treasury futures have features that can mitigate their risks, but don’t eliminate them. The futures contracts used by these three funds are exchange-traded, standardized derivatives contracts whose prices are re-evaluated daily, which means:

- They are backed by the central clearinghouse, limiting counterparty risk.

- The market is highly liquid, which supports efficient price discovery.

- They are marked to market daily, reflecting any gain/loss in the margin account of market participants.

The more important risk, however, is how they respond to changing market conditions. Any leveraged portfolio will amplify the gains and losses of the underlying strategy by the degree of leverage. Leverage isn’t for the faint of heart.

Track Record

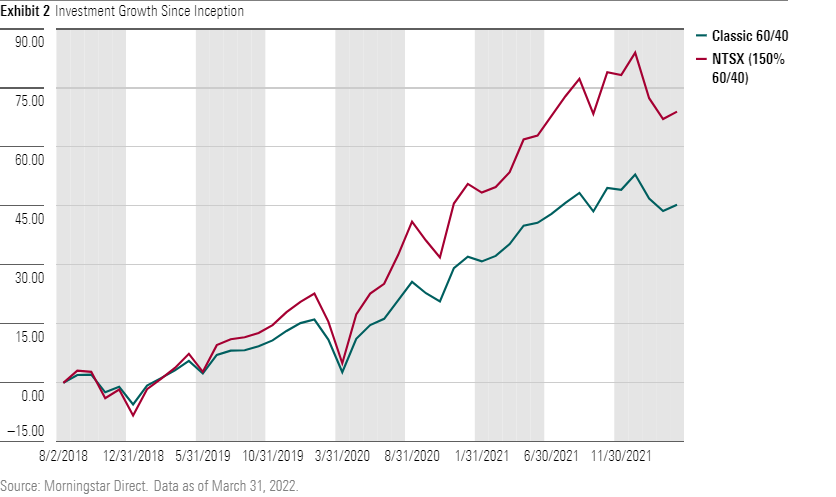

Exhibit 2 plots the since-inception performance of NTSX alongside the classic 60/40 portfolio. The 60/40 portfolio allocates 60% to the iShares Core S&P 500 ETF IVV and 40% to iShares Core US Aggregate Bond ETF AGG, for an asset-weighted annual fee of 0.03%. NTSX carries a 0.20% annual fee.

Since its inception, NTSX has delivered better returns than the classic 60/40 portfolio. The 60/40 portfolio has returned 10.7% annually, while the fund added 15.4% over the same period with higher volatility. As mentioned above, the fund amplifies the performance of the classic 60/40 allocation with its 1.5 times leverage. NTSX experienced ideal conditions during much its short history. Declining interest rates and rallying stocks were a boon to both sleeves of the portfolio.

However, the fund also amplifies the losses of a 60/40 portfolio. This was clear in the first quarter of 2022. The fund underperformed its unleveraged counterpart as inflation and the prospects of higher interest rates sent both stocks and bonds tumbling. During this time, the classic 60/40 portfolio dropped 5 percentage points while NTSX lost about 1.6 times that amount—8.1%.

Leverage as a Tool

Leverage is a double-edged sword that enhances positive returns and compounds losses. However, investors can also use leverage as a mechanism to maintain baseline exposure and free up assets to explore other options. As previously illustrated, one of the use cases for these funds is allocating two thirds of the portfolio to NTSX, and using the remaining one third to add another dose of diversification or seek out some alpha.

At its core, 60/40 is the classic tale of diversification. By adding room for even more diversification, the WisdomTree funds provide investors with the option to enhance its returns or further reduce risk. Leverage does come with operational complexities that increase the margin for error. However, it is ultimately just another mechanism in an investor’s toolkit that, if understood and used appropriately, can be a powerful tool.

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BNHBFLSEHBBGBEEQAWGAG6FHLQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/c00554e5-8c4c-4ca5-afc8-d2630eab0b0a.jpg)