Why the Fed Changed Its Tune on Rates

A strong job market and persistent inflation pressures mean that higher rates will be here sooner.

/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

Federal Reserve officials are closing out 2021 with a hard pivot toward a more-aggressive pace of interest-rate increases next year in response to a strengthening job market and unexpectedly stubborn inflation pressures.

Investors should now expect three interest-rate increases from the Federal Reserve by the end of 2022--possibly starting as soon as March--even as some sources of inflation begin to cool off by later in the year.

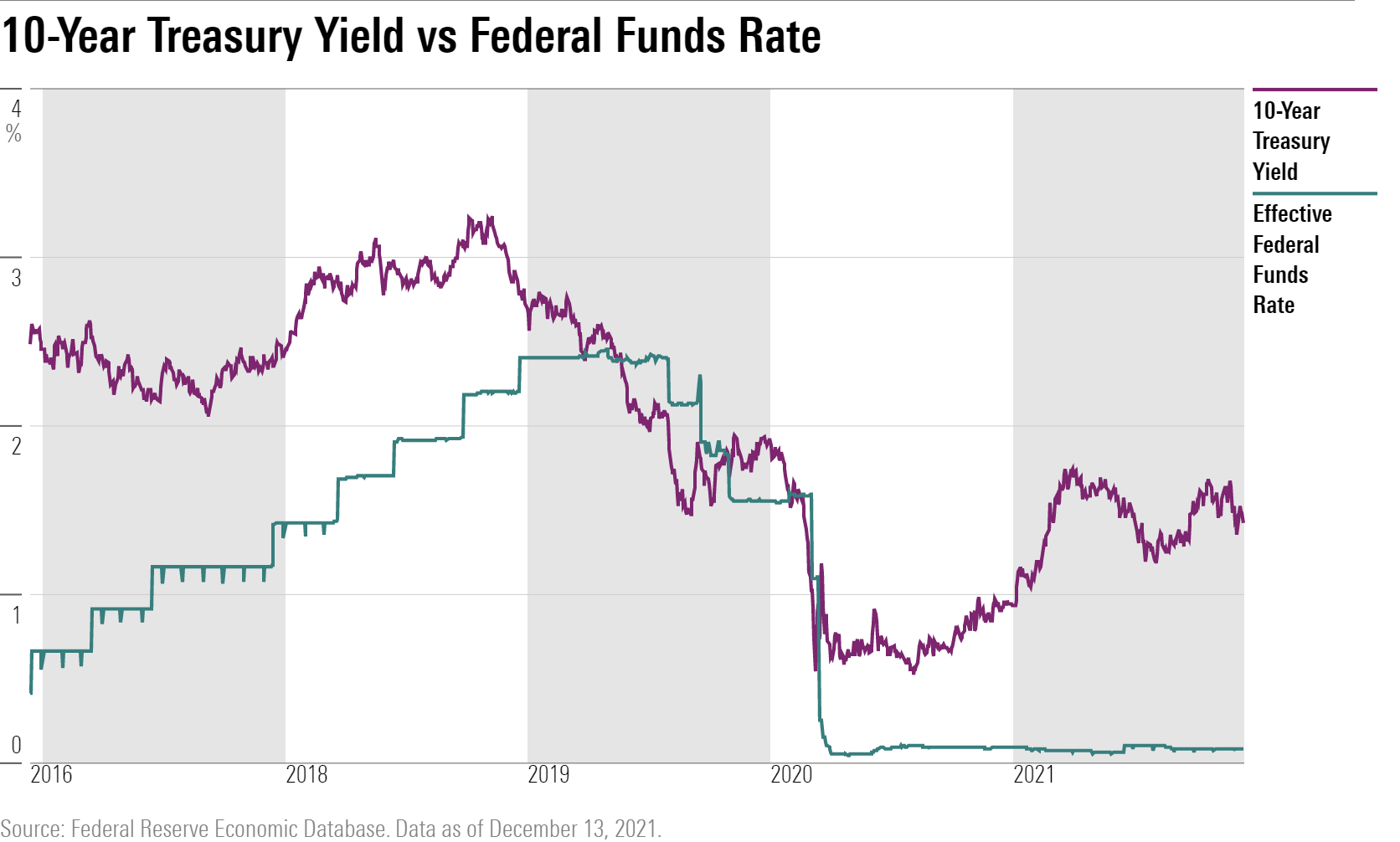

In its final meeting of 2021, the policy-making Federal Open Market Committee held the federal-funds rate at 0.0%-0.25%.

A change in rates wasn’t expected at this meeting; that's a debate we expect will really heat up in mid-2022.

Instead, the main focus this time had been on an expected acceleration of tapering in the bond market purchases that the central bank has been using since early 2020 to inject money into the banking system and support the economy amid the pandemic. But eyes were also on any hints of how the Fed will navigate rate hikes in 2022, and there were a lot of key updates here.

While our read after the previous meeting was that the Fed remained dovish (did not come out ahead of expectations with its tapering or remove “transitory” language), times have changed and the Fed has pivoted rather dramatically since.

This was highlighted by Federal Reserve Chair Jerome Powell's congressional testimony at the end of November, in which he said that they plan to retire the “transitory” language and also foreshadowed an accelerated taper. A lot can change in just one month, and we think it’s good to keep in mind that the Fed can and does change its mind, and the underlying data does change over time as well.

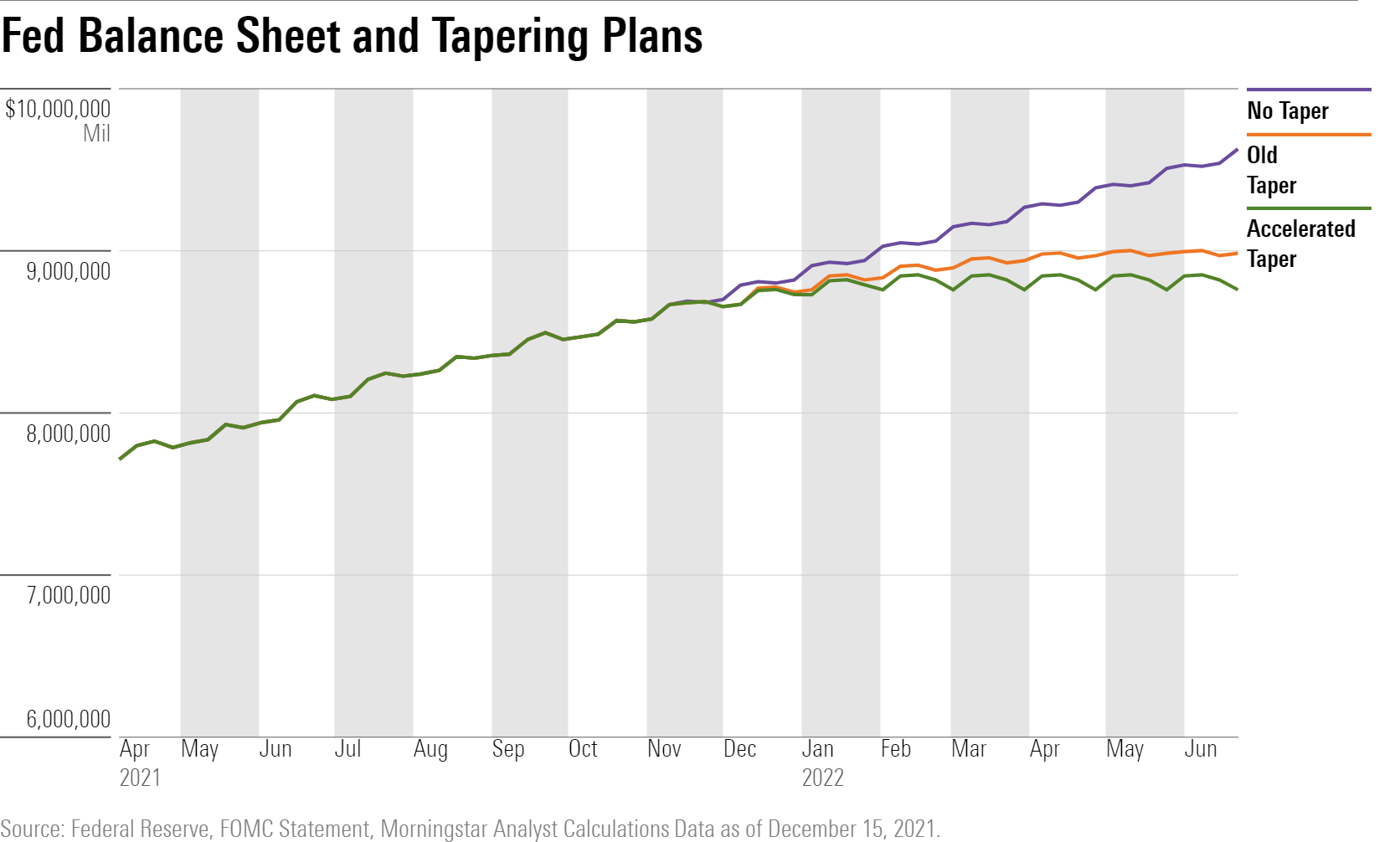

Many market participants expected a doubling of the pace of tapering, and the Fed delivered, increasing the pace of its taper to $30 billion per month ($20 billion of Treasuries, $10 billion of mortgage-backed bonds) from $15 billion. This baseline tapering should lead to the end of asset purchases by late February/early March.

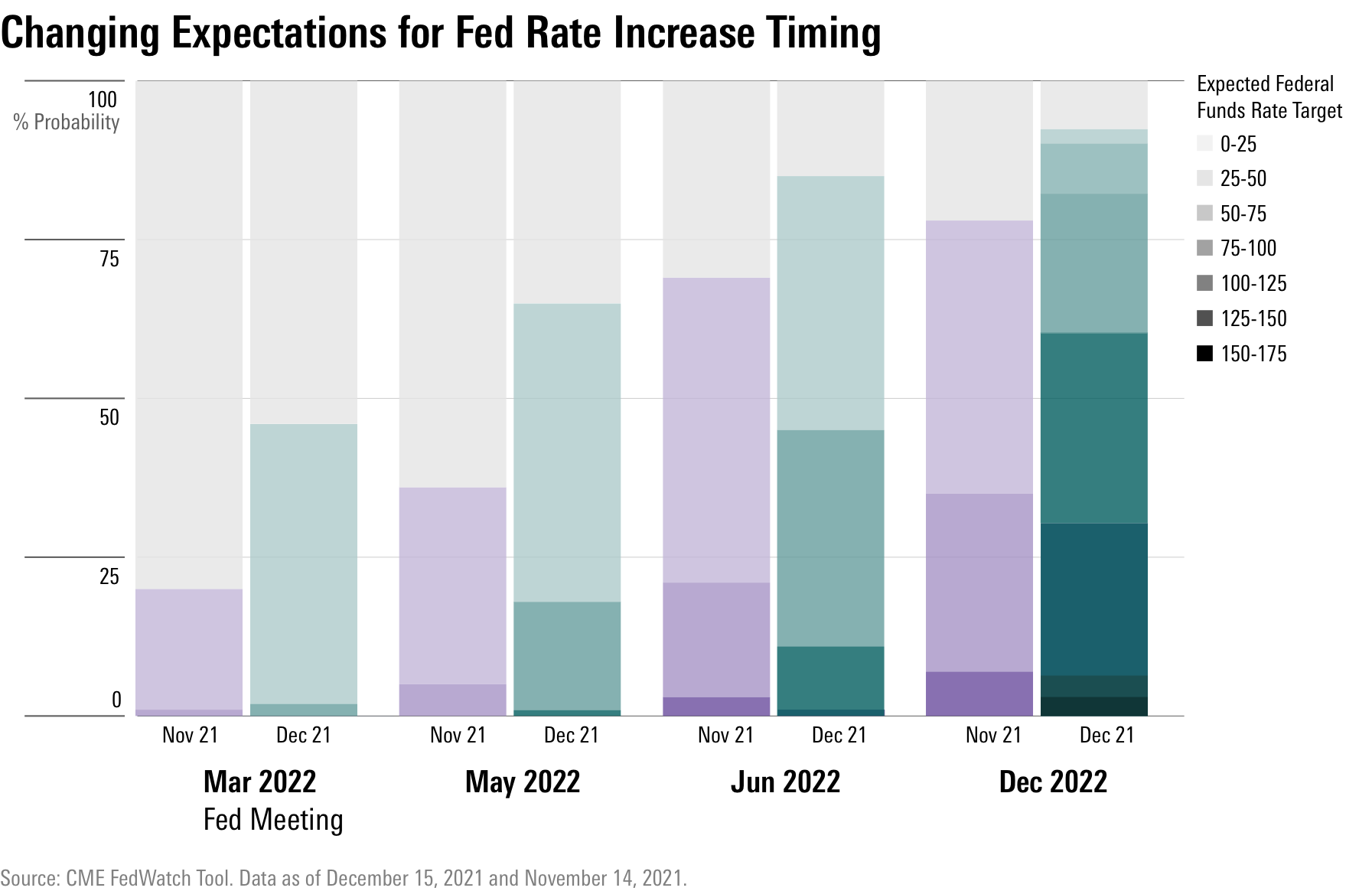

Perhaps the biggest surprise was how hawkish the rate-hike projections turned. Powell is not the only FOMC member changing his stance. The median participant now expects three rate hikes in 2022 (a range of 0.75%-1%), and another three hikes in 2023, bringing the federal-funds rate to a range of 1.5%-1.75% by the end of 2023.

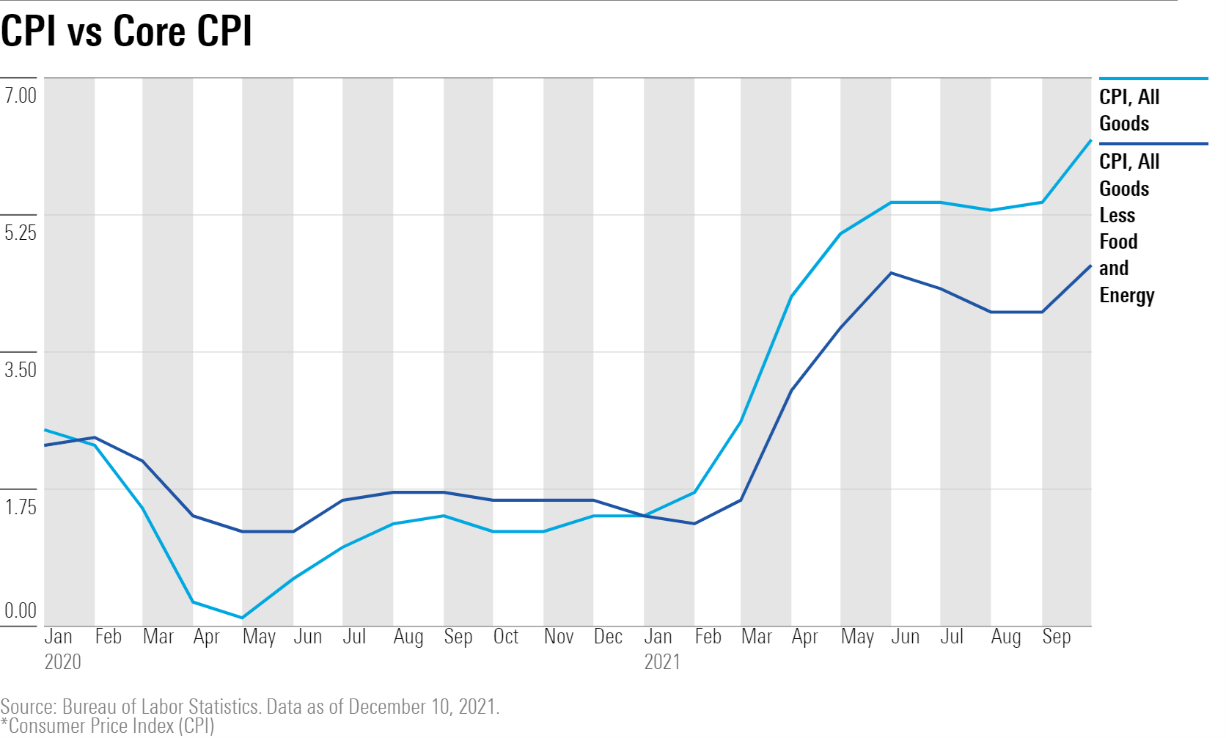

We think the Fed is signaling that it is taking inflation seriously now. After coming across rather dovish for the past several years, the Fed believes inflation is here to stay for a while and the time has come for a hard pivot.

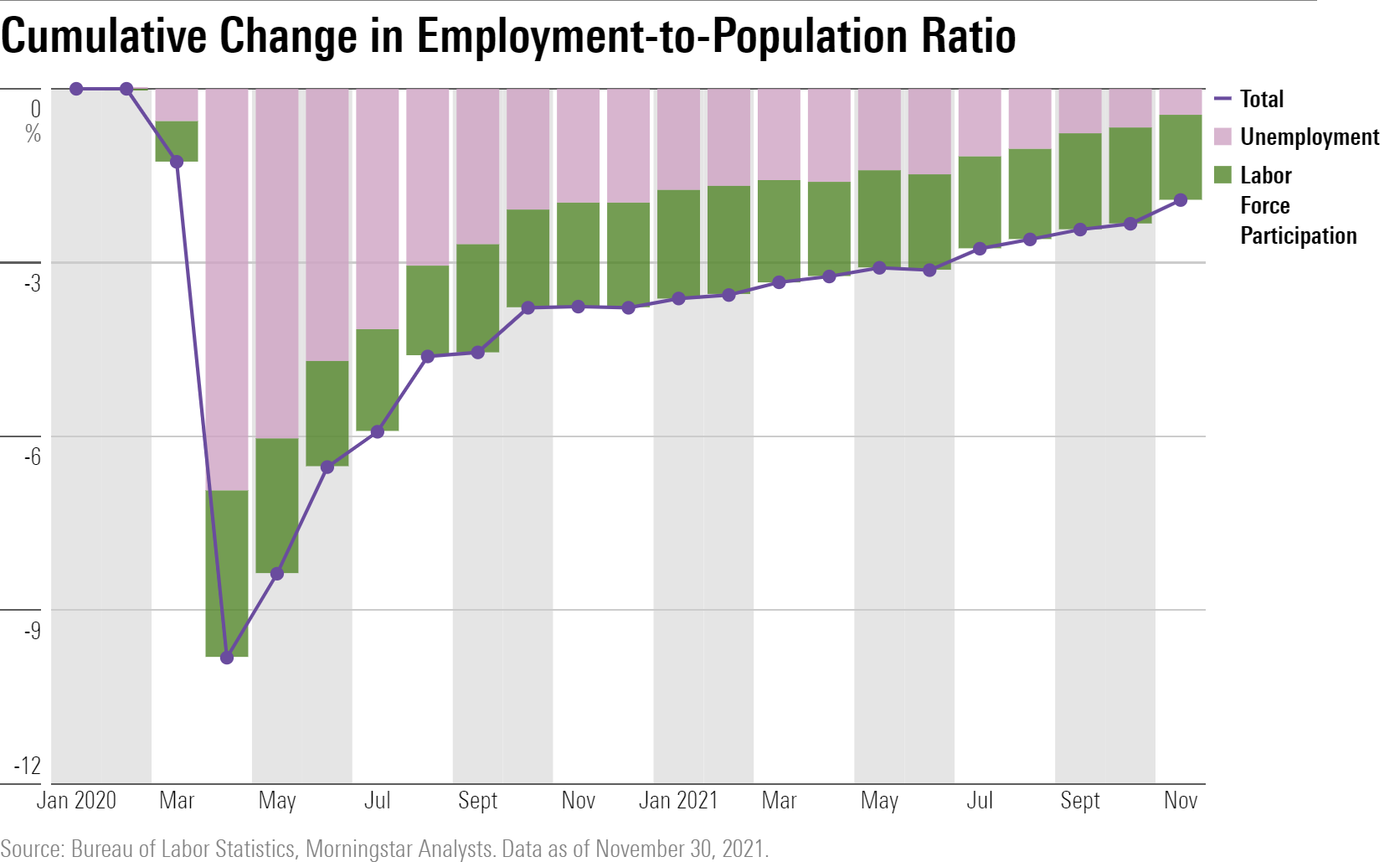

The committee admitted that inflation has “exceeded 2 percent for some time” and stated that it will maintain low rates until “labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment.” We note that unemployment improved to 4.2% based on the November employment summary release, which is within the range of "maximum employment," as estimated by the Fed (3.8%-4.2%). We don’t think there will be anything holding the Fed back from rate hikes once tapering is complete.

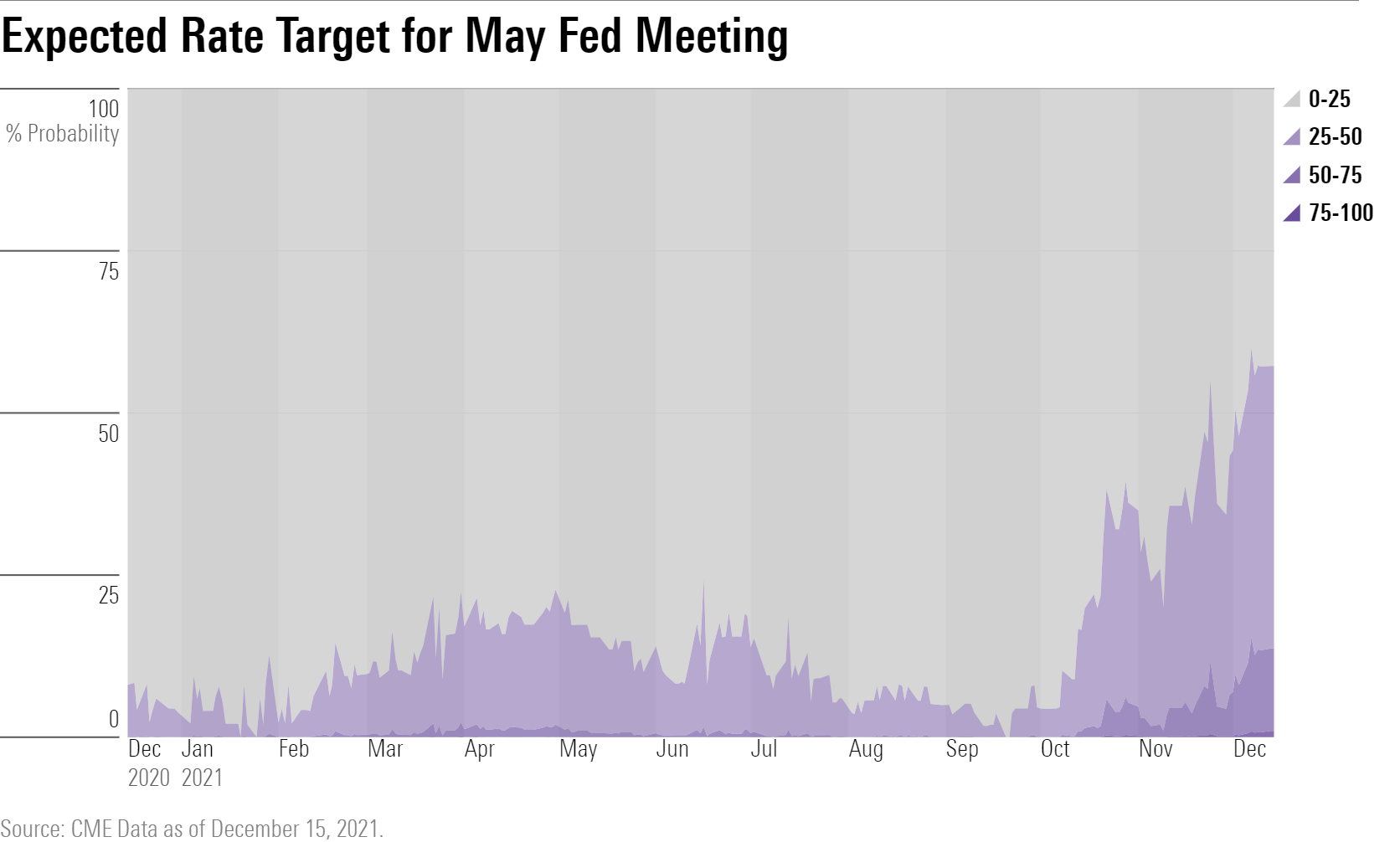

In response to these changes, we now believe the Fed and expect three rate hikes in 2022 (one in mid-2022, one at the September meeting, and one at the December meeting) and three additional hikes in 2023 (January through July); this is a significant change from our previous view where we expected only two hikes through 2023. There is the possibility that the Fed will start hikes even by March, given its taper schedule.

Our original stance was that the Fed would continue to be stuck choosing between “stable prices” and “maximum employment,” as inflation stayed higher than the 2% goal and as the participation rate stayed stuck, and that the Fed would stay dovish under this scenario. However, the latest data is becoming increasingly one-sided, with the participation rate showing some improvement in the December Current Employment Statistics release (to 61.8% from 61.6%, although still below the 63% plus level before the pandemic), unemployment improving to 4.2% (within the range of “maximum employment” as estimated by the Fed), and inflation has continued to soar.

While some sources of higher inflation are likely to ease in 2022 and 2023 (energy and autos), inflation pressure has broadened out, and most importantly, evidence of wage inflation is starting to pick up. We agree that more and more economic data points to the need for less-accommodative policy, and we expect the Fed to respond as such.

We still think the Fed will have to “thread the needle” once into 2023, balancing a retreat in inflation with higher debt loads and what is likely to be a cooldown in economic growth; as such, we still think more-hawkish views for rates to reach 2% or more in the next couple of years could be too aggressive. The Fed’s own updated projections show rates reaching above 2% in 2024 and 2.5% over the longer run, and we wonder whether these may be too high.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e03383eb-3d0b-4b25-96ab-00a6aa2121de.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)