The Risks Ahead for 2024 and How Investors Can Manage Them

Today’s risks feel elevated, so what really matters?

/s3.amazonaws.com/arc-authors/morningstar/1bb3b7d2-89c3-40c6-ad6d-01d4f0004f7a.jpg)

Investors are always walking the tight rope of risk, particularly when risk comes in the form of external shocks. But aiming for accurate predictions around risk is a fool’s game. So, rather than predict, we prepare. The perception of risk can greatly affect market sentiment, often creating opportunities, too. We seek to understand both sides of the coin.

The current market conditions highlight several significant challenges for investors. The key at this juncture is accepting the reality of market risks while not becoming unnerved by them. It’s easy to lose one’s bearings amid the continuous stream of market news and speculation, dubbed as “black swan hunting.” As investors, it is critical to discern this noise from facts, focusing on long-term investment strategies rather than panic-induced decisions sparked by temporary market fluctuations. If anything, lean into the volatility and reframe nervousness as excitement for opportunities.

As we stand on the precipice of 2024, it is crucial for us as investors to harness the power of behavioral science in maneuvering through the risks that lie in the landscape of economy and geopolitics. As a starting point, let’s collectively agree that uncertainty is always present, with at times terrifying headlines dominating our collective consciousness. Nevertheless, equities, which make up the lion’s share of most investors’ portfolios, have managed to return 7.4% per year after inflation over the trailing 100 years (S&P 500 total real return, annualized), allowing investors to compound returns despite two world wars, the Cold War, a global pandemic, and a range of local economic crises. That shift in perspective, from the narrow “what just happened” to the broader “how do market cycles evolve,” is key in helping imperfect decision-makers choose wisely in the face of irreducible uncertainty.

The Market Hates Uncertainty and Negative Surprises

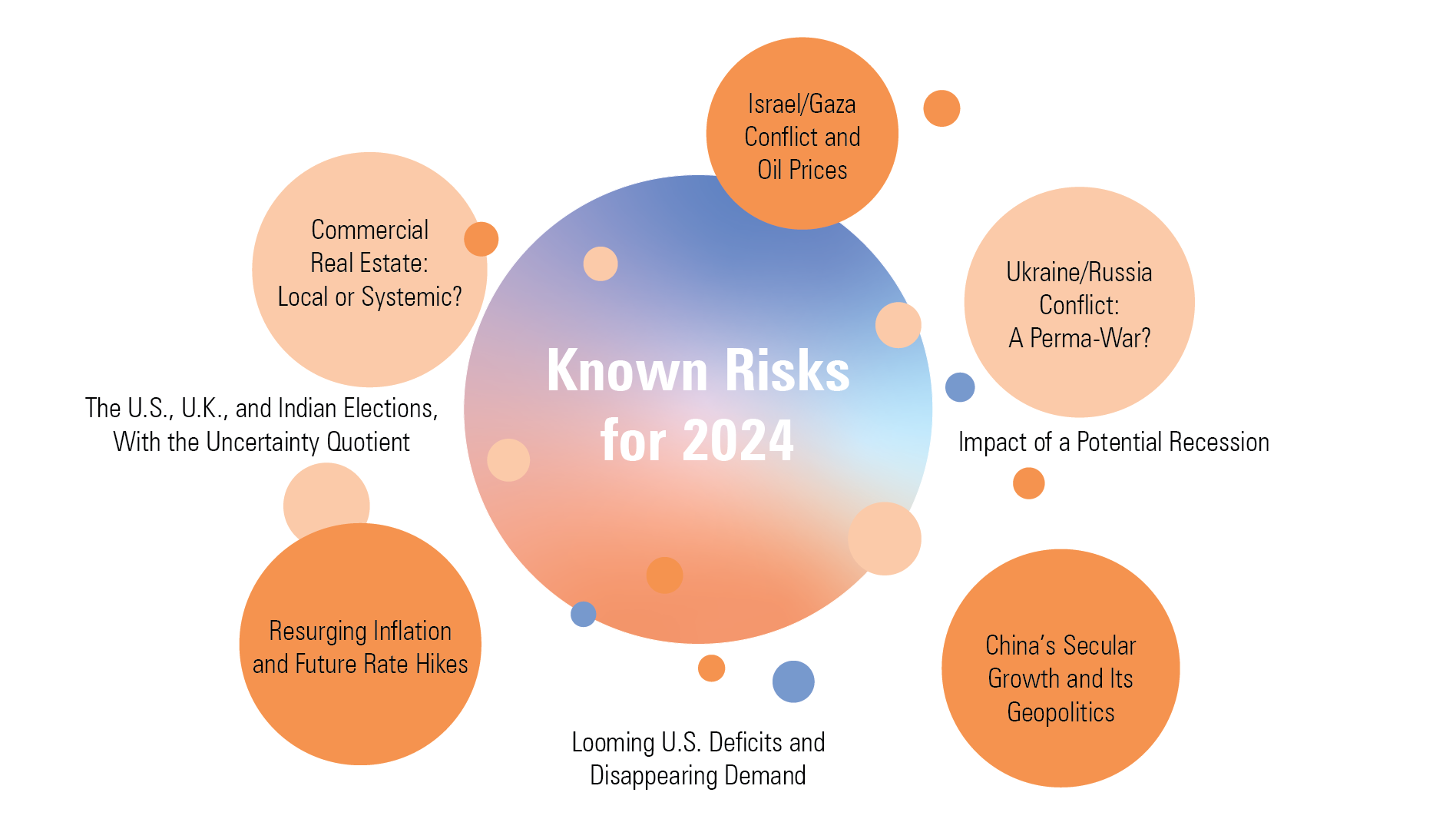

The resilience of the broader markets may be cold comfort as we look at the litany of known risks facing us at the start of 2024, particularly for those with shorter investment time horizons. The samplings below are top of mind for us.

Current Headline Risks Are Plentiful Entering 2024

This collection of concerns is daunting, but it’s worth remembering that not every risk requires a whole new portfolio to survive its realization. A well-calibrated portfolio—a collection of global equities, fixed income across a range of maturities, and, at least for our part, carefully selected hedged strategies designed to limit overall interest-rate risk—should weather external shocks fairly well.

In other words, we can build robust portfolios that can hold up to a variety of different eventualities; we don’t have to have a crystal ball to know what is going to happen next. Rather, we can build portfolios that find and protect value over a wide range of “what ifs.” In fact, to the extent an external shock causes sudden negative sentiment, we likely would consider the price dislocation an opportunity. That was the case during the coronavirus pandemic, for example. Recall that in March 2020, global equities crashed in unison, while liquidity concerns froze bond markets, including the U.S. Treasury market, which is known as a global safe haven. As the pandemic developed and lockdowns ensued, we had no greater foresight than anyone else on the range of potential outcomes. What we did know was that asset prices were getting crushed far beyond our estimates of normalized fair value. As a result, our portfolio managers around the globe added risk—equities (for example, energy stocks), high-yield bonds, emerging-markets bonds, and more—as quickly as we could. The rest is history. After a 22% correction between Feb. 20, 2020, and April 7, 2020, global equity markets rallied tremendously. Despite the massive loss, the Morningstar Global Markets Index managed a 16% return for 2020 in its entirety.

Using Techniques to Manage Portfolio Risks

Not every external shock follows the COVID-19 path. Some really do impair cash flows, meaning that the fair value of the asset permanently deteriorates. A recent, extreme example? Russian equities in the wake of the Ukraine invasion.

In other instances, a portfolio may not be as well calibrated as the investor thinks. Perhaps that’s because a position wasn’t sized correctly given all its risks or the underlying fundamentals of an offsetting position weren’t fully understood. The latter has been the case for U.S. investors who assumed long-term U.S. Treasuries would always perfectly offset the risks of U.S. equities. While big returns from U.S. stocks have helped recoup much of 2022′s losses, it could take fixed-income investors longer to make up for the 6.25% annualized loss over the trailing 2.5 years, given the traditionally lower returns in that market.

Of course, none of that matters if it’s possible to predict with certainty both the risk and the ensuing market impact. However, we argue that’s near to impossible. Think about the most momentous events in recent market history: COVID-19 and lockdowns; global inflation; aggressive central bank policy. Few of these developments were predicted accurately ahead of time, and if a particular investor was able to call one risk, they were unable to predict the rest.

With an appreciation for uncertainty firmly in mind, we believe the best approach to managing external shocks—geopolitical or otherwise—is ongoing fundamental asset-class analysis and careful portfolio construction. So, with these two tools firmly in hand, we’ll walk through the 2024 risks we’ve identified. We include the expected impact of these risks, any opportunities that could emerge, and potential offsets we believe could mitigate possible damage.

Our Approach to Handling New Risks as We Enter 2024

| Risk | Impact | Nature of Risk | Potential Opportunity | Offsetting Positions |

|---|---|---|---|---|

| Commercial Real Estate Crash | Regional bank write-downs | Cash flow impairment: Banks | Oversold regional banks | |

| Expanding Middle East Conflict | Energy market disruption | Oil price shocks, which, in turn, could increase recession risk for vulnerable economies | Cheaply priced energy assets like U.S. MLPs and European energy | |

| Prolonged Ukraine/Russia Conflict | Energy/food market disruption, European economic pressure | Food or oil price shocks, which, in turn, could increase recession risk for vulnerable economies | Cheaply priced energy assets like U.S. MLPs and European energy | |

| China’s Secular Growth Crash | Stagnating or collapsing Chinese economy | Cash flow impairment: Chinese equities, heightened recession risk for trade partners | Oversold Chinese technology equities | |

| China/U.S. Conflict | Rapid reshoring, global economic uncertainty | Global equity volatility | Long-term, high-quality government bonds | |

| Resurging Inflation | Higher interest rates, falling corporate earnings, heightened recession risk | Equity and fixed-income volatility | Short-term, high-quality government bonds & hedged alternatives | |

| Developed-Markets Sovereign Deficits | Increased term premium (investors demanding higher long-term yields) | Cash flow impairment: Longer-term yields reset higher, price loss | Short-term, high-quality government bonds & hedged alternatives | |

| U.S. Contested Election | U.S. political uncertainty | Short-term U.S. equity volatility | Long-term, high-quality government bonds |

Source: Morningstar. Risks assessed as of Nov. 15, 2023. For illustrative purposes only.

A review of this list shows two consistent themes. First, we believe most of these risks result in volatility but don’t necessarily change future return expectations, which means that, in many instances, price dislocation that results from these events could be a broad-based buying opportunity.

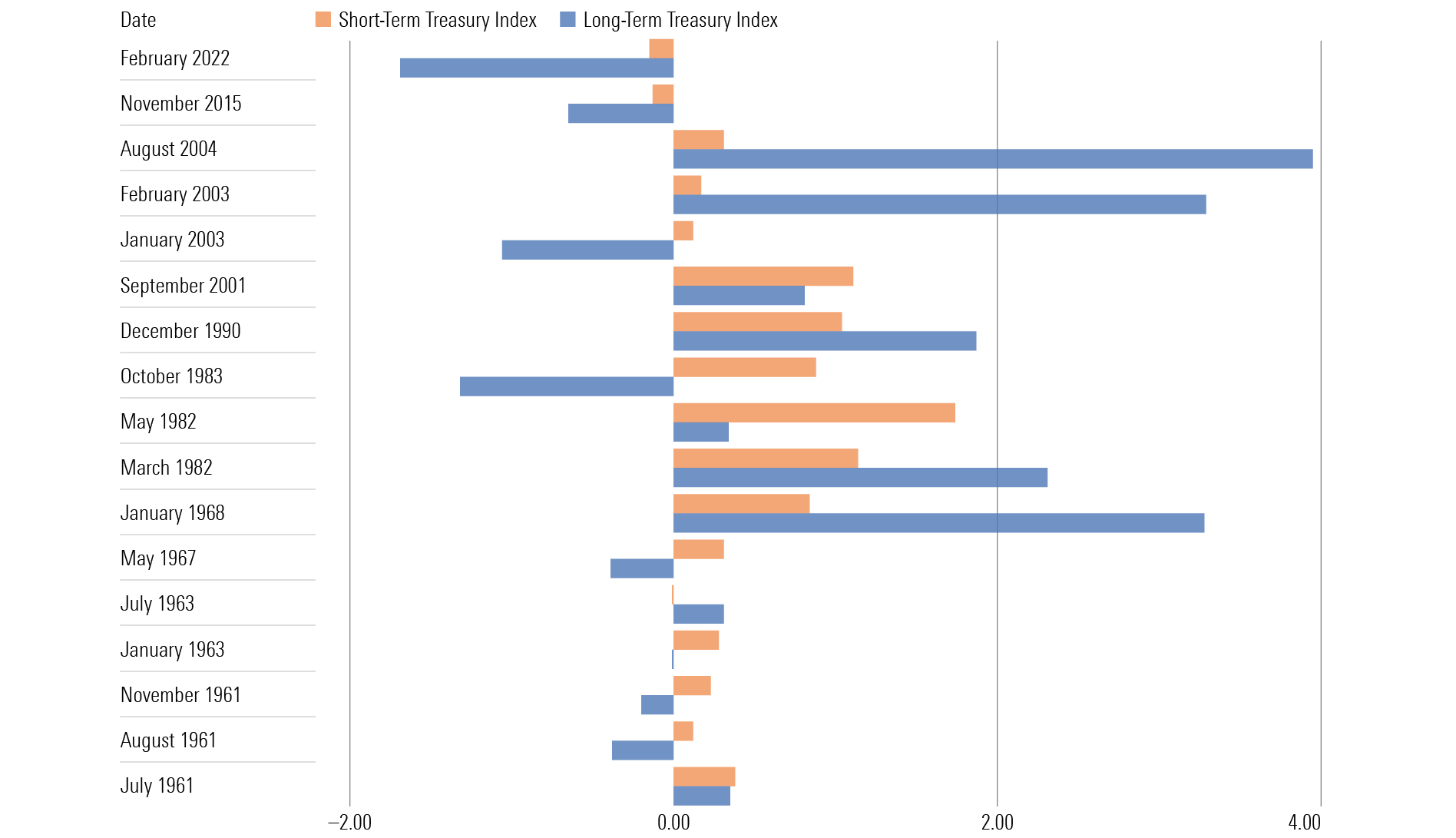

Second, we tend to look to high-quality government bonds to hedge geopolitical risk. Why? It’s a relative safety proposition. Geopolitical events don’t consistently cause equity market selloffs, but when they do, we find more often than not that government bonds—particularly long in duration, but at times short-duration bonds, as well—provide an offset.

U.S. Government Bond Monthly Performance When Geopolitical Risk Spikes

Bonds to Play a Role in 2024 and Beyond

The infinitesimal credit risk of the U.S. government provides shelter when other countries face crisis. It is even more as we enter 2024, with yield levels of the 10-year Treasury now at attractive levels. That added cushion, so to speak, gives the hedging appeal of Treasuries added return potential.

But we’d also argue that longer-term U.S. Treasuries could prove a store of value if volatility ensues from contested U.S. elections. That may seem surprising, since credit risk would seem to flare in those circumstances.

As disconcerting as polarized politics can feel, as we approach the U.S. election in 2024, the two primary questions for investors remain long term in nature and surround fiscal responsibility and the impact of potential policy changes. The direction the wind blows on these issues could determine the course of the market.

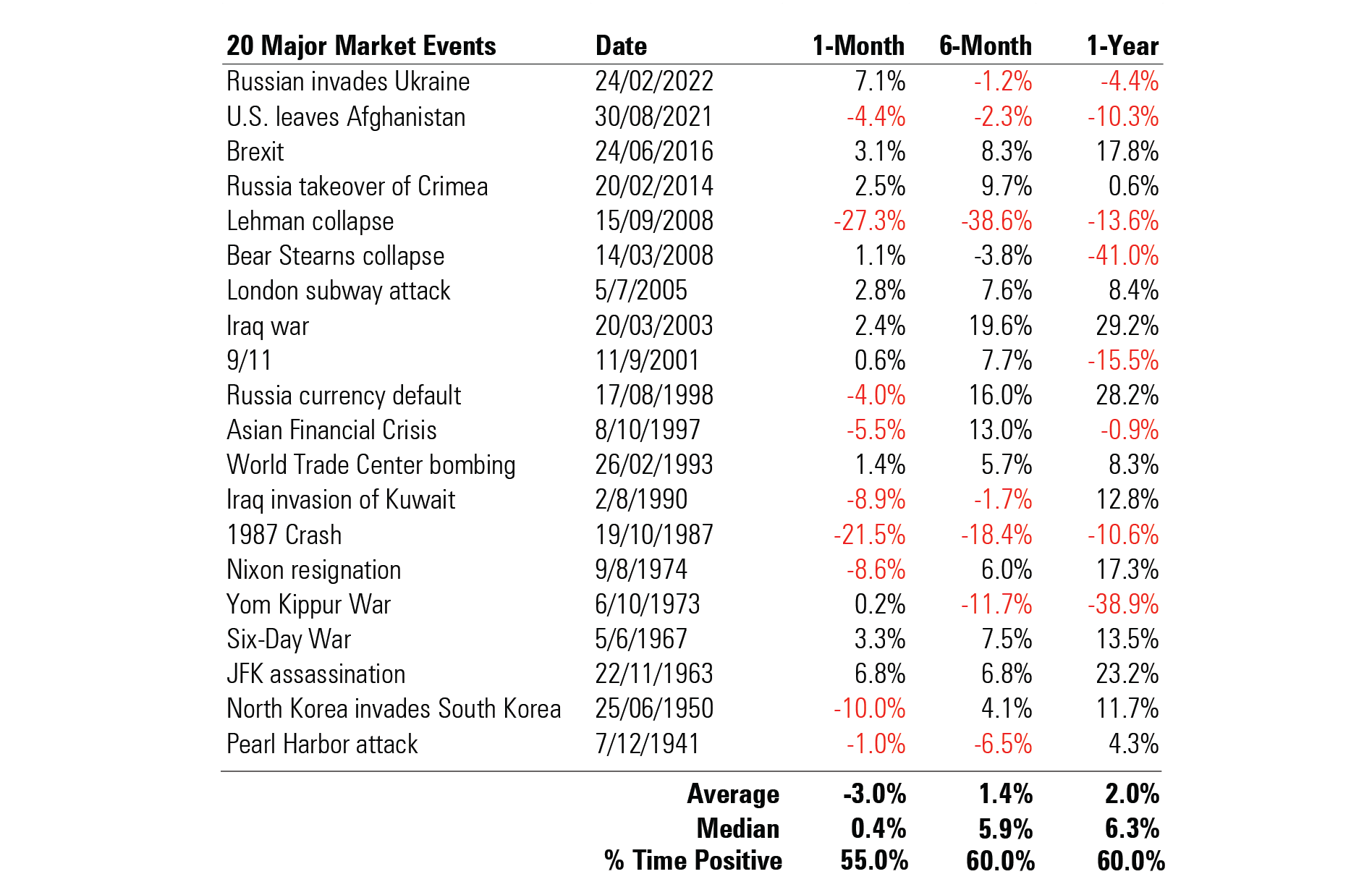

And as we’ve observed from prior short-term crises, whether that’s from government shutdowns or the Jan. 6 U.S. Capitol riot, the uncertainty of the moment tends to cause selloffs in so-called risk assets—equities and corporate bonds as two prime examples. However, over the long run, equities and credit have recovered. Meanwhile, Treasuries tend to act as a store of value because the long-term financial stability of the U.S. government is not in question, and the key risks for Treasuries—inflation and rising interest rates—aren’t necessarily in play.

The Impact of Major Global Events, With Short-Term Equity Moves

It’s worth noting that U.S. Treasuries have risks of their own. Among these are rising rates, inflation, and so-called “technical” or supply/demand concerns, in which the government needs to issue more bonds to fund deficits, while foreign investors, commercial banks, or the Federal Reserve are no longer reliable buyers. The unexpected arrival of these risks can cause yields to rise and prices to fall, as we’ve seen in recent years.

The key word is “unexpected,” which means that prices don’t reflect the risk. If U.S. Treasury bond prices don’t offer much margin of safety for concerns around deficits or the potential for higher inflation or rates, then longer U.S. Treasuries have less appeal for us. In those instances, short-dated bonds or even cash play a greater role in our portfolio construction.

Finally, from where we sit at the time of writing, we see few indications of building risk in credit markets. Commercial real estate is the one exception.

Dangers in Commercial Real Estate, Though We Still See Merit in Banks

As with most other investors, we see the potential for meaningful write-downs within the office space, in large part because of changing work preferences in the wake of the pandemic.

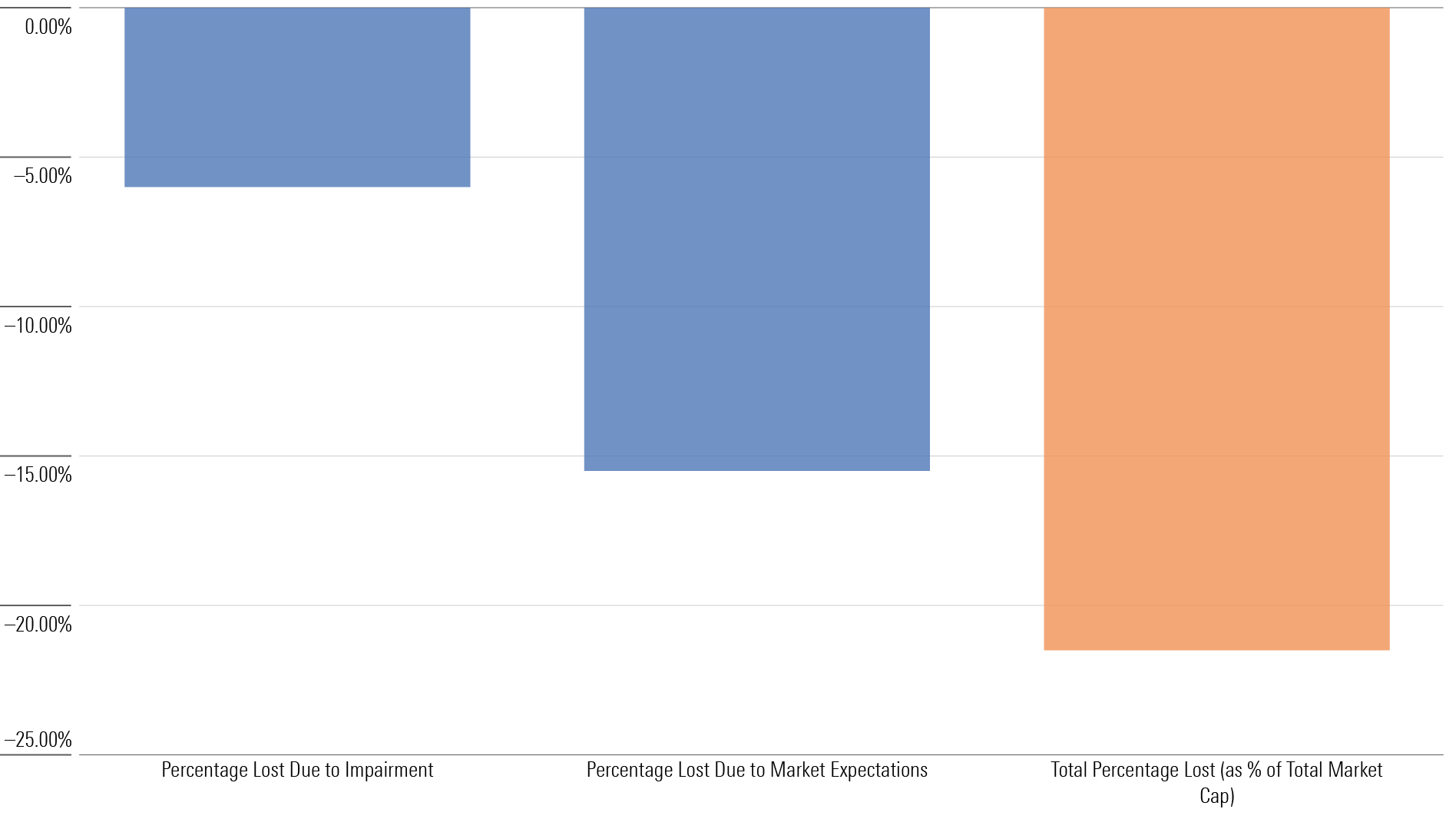

We’ve attempted to identify the various touch points the broader economy has with commercial real estate, and while we see potential pain points for pensions, for example, we think most of the pain for public markets will be localized in regional banks.

Even here, though, we think the risk varies by bank and, in at least some cases, is overdone. To manage the risk while taking advantage of the opportunity, we’ve carefully sized exposure to a collection of bank stocks, screening for commercial real estate exposure and avoiding companies that appear particularly exposed.

2023 Bank’s Market Loss vs. Estimated Aggregate Commercial Real Estate Impairment

Here’s the overarching takeaway for external risks in 2024: They exist, as they always do, but we believe the vast majority relate to volatility and present as much opportunity as loss potential. The very essence of external shocks is their uncertainty, both in timing and magnitude.

Without question, many risks potentially have a higher probability than what’s on this list, but we just don’t know about them yet. It’s with this uncertainty in mind that we think having a robustly constructed portfolio that considers the full range of outcomes is a critical component to investing success.

Valuation Risk Is Often Ignored, but It Really Matters

Overvaluation risk is a real problem that’s never featured on the laundry list of what can go wrong. Everything has a price, with swings in perceived risk creating potential mispricing. No bad news? Likely elevated valuations. A lot of perceived risk? Possibility of attractive prices.

Some great companies have high valuations and need significant growth to deliver on market expectations. In this regard, we believe the very narrow market leadership of large-cap U.S. technology names in 2023 has provided an interesting investing landscape looking ahead to 2024 and beyond. Much of the U.S. market’s gains in the first half of 2023 were driven by the extraordinary returns of just a handful of companies. It is not to say that the so-called “Magnificent Seven″ are not great companies, but they do have high valuations and need significant growth to deliver on market expectations.

Said simply, some markets have no room for error or disappointment. Other markets are priced for a story of despair—for example, China equities—where only a little needs to go right. Fundamentals matter, especially with higher rates, so investing where there is a valuation buffer or margin of safety is key for the years ahead. This is a story that we see play out again and again in markets.

Chinese Stocks Are Perceived as Risky, but Upside Potential Exists

To be clear, we acknowledge the uncertainty that surrounds these markets, and we have no better clarity than others on how it will play out. To manage those concerns, we rely on scenario testing to determine our positioning:

- How much can we own, assuming the worst happens, without jeopardizing our overall portfolio outcomes?

- Do we have overlapping exposure here that we don’t see at first blush? How can we manage these risks?

Valuations are an underrated tool to shift the risk to reward in your favor. And where headline risks are plentiful, we often find tomorrow’s golden opportunities.

New Risks, Consistent Approach

Patience and perspective are key in the world of investing. Before making any move, consider what is already priced in and how the markets have already adjusted. While risk might initially sound intimidating, it isn’t always a bad thing. Risk can be a catalyst for opportunity if managed with care. After all, in the world of investments, risk not only creates a possibility of loss but also forges avenues for gain.

Risk and reward are different sides of the same coin, and investors cannot expect outsize gains without taking on some risk. This does not feel intuitive, as our brains are not wired for patience or for eagerly embracing uncertainty. Histrionic headlines don’t help. However, discipline and long-term perspective are never out of style and investing principles can pay off most handsomely during turbulent times.

While the risks we face as we enter 2024 are significant, they are not insurmountable. The keys are to stay calm, focus on the long term, sift through the noise, and apply robust risk-management techniques. Remember, even in the face of risk, opportunity lies. Armed with a thorough understanding of the market, sound strategies, and a cool head, investors can not only weather the current market conditions but also find potential opportunities amid them.

Morningstar Investment Management LLC is a Registered Investment Advisor and subsidiary of Morningstar, Inc. The Morningstar name and logo are registered marks of Morningstar, Inc. Opinions expressed are as of the date indicated; such opinions are subject to change without notice. Morningstar Investment Management and its affiliates shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Before making any investment decision, please consider consulting a financial or tax professional regarding your unique situation.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1bb3b7d2-89c3-40c6-ad6d-01d4f0004f7a.jpg)