Jobs Data Shows Coronavirus Pandemic Impact Easing

More strong hiring in March is good news for the economy.

/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)

The U.S. job market continues to power along, signaling continued health for the economy as the impact of the omicron coronavirus variant shows signs of easing.

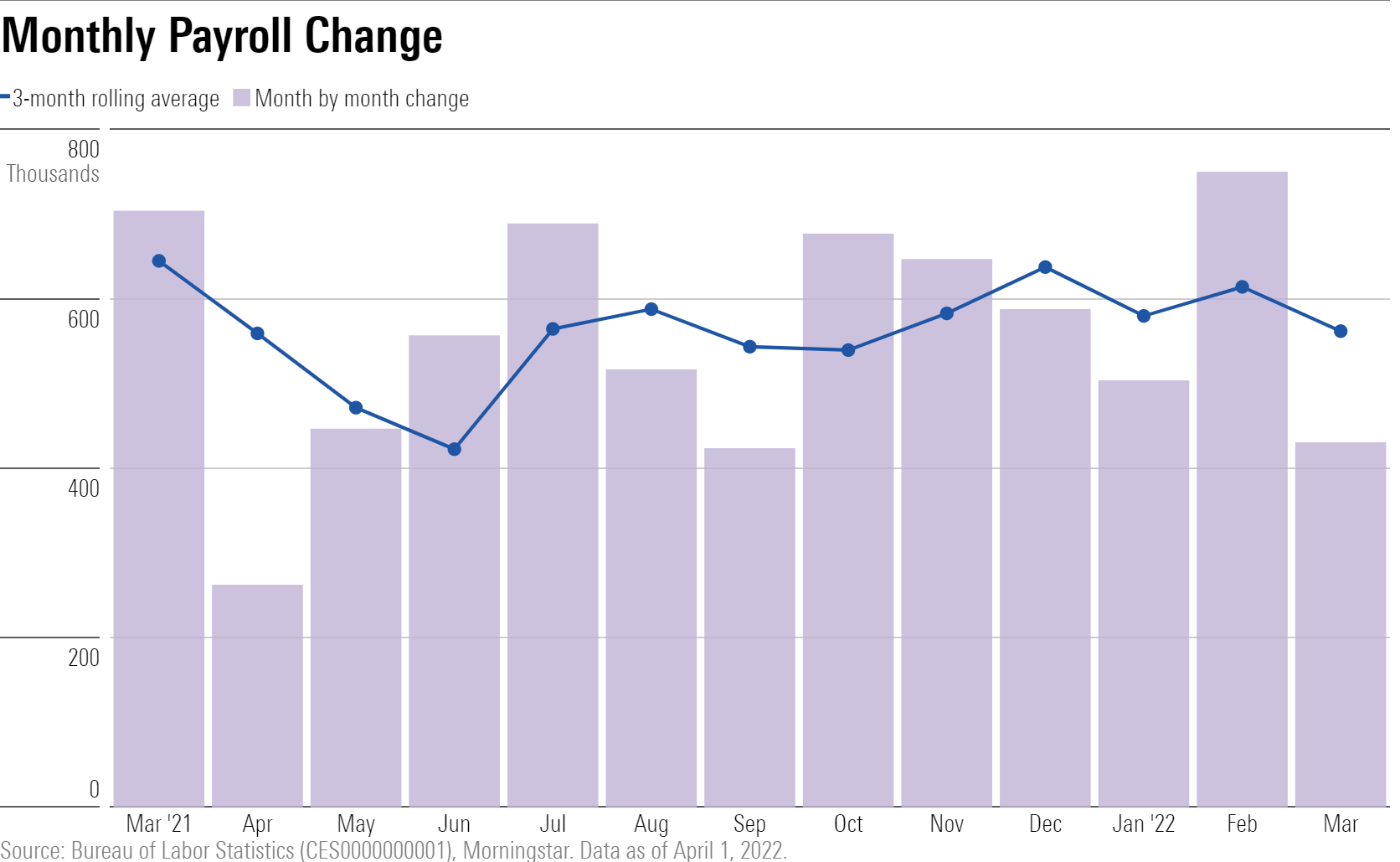

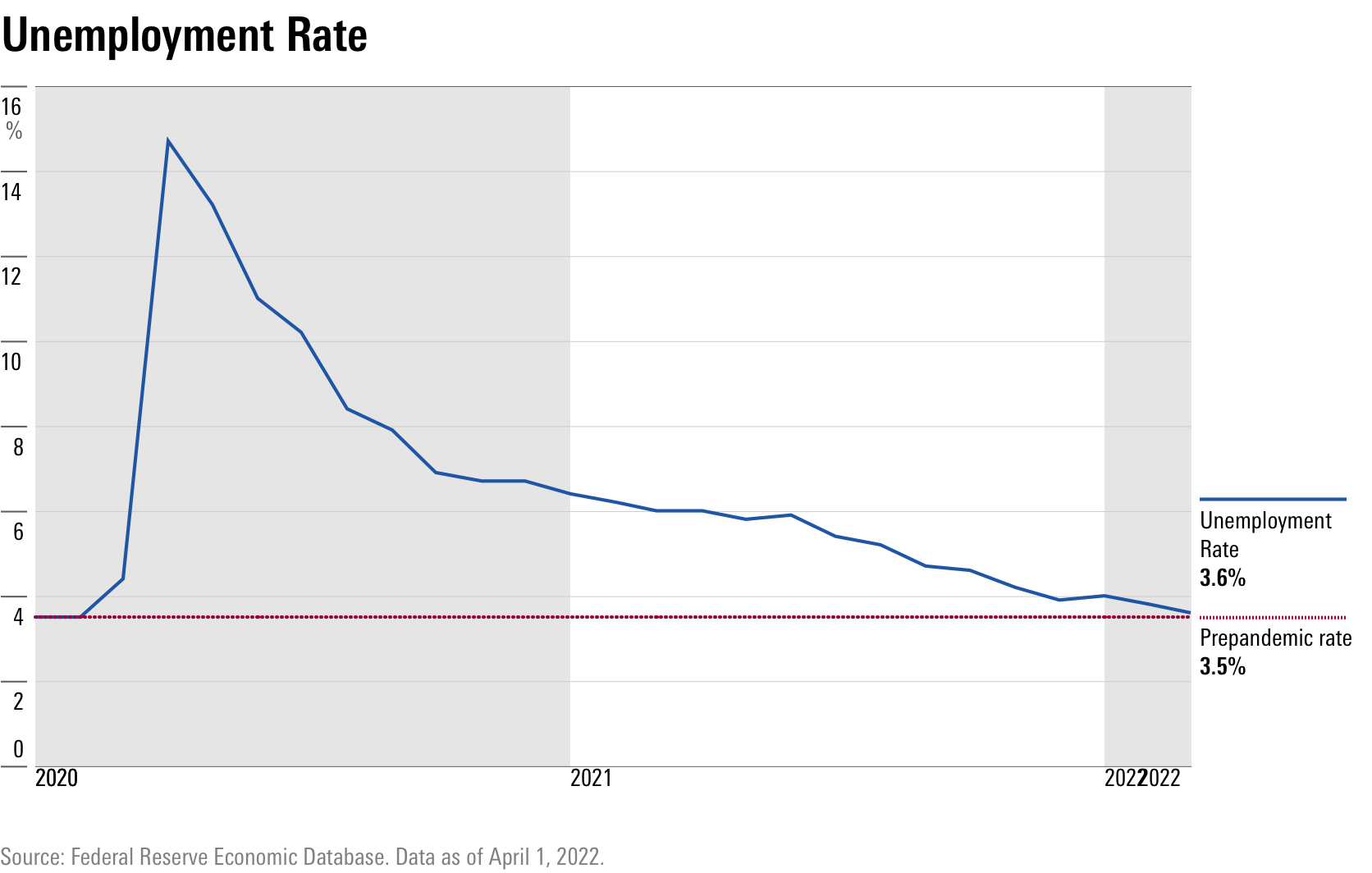

Businesses added 431,000 jobs in March, roughly in line with economists' forecasts. At the same time the unemployment rate fell to 3.6%.

In addition to the overall strength in hiring, the report also provided glimmers of hope that some of the bottlenecks in the labor market caused by the pandemic are beginning to ease, says Preston Caldwell, Morningstar’s chief economist.

“Today's report showed that the labor market recovery is continuing,” he says. “Some of the abnormalities of the recent job market, namely the limited response of labor supply to attractive wage gains and record job openings, appear to be correcting.”

“Our bullish view on labor supply expansion going forward was manifest in today's report, given the solid gains in labor force participation along with moderate wage growth,” Caldwell says. “We ultimately expect labor force participation to surpass pre-pandemic levels, which is a key driver in our bullish economic outlook."

Job Growth Continued in March

The 431,000 gain in payrolls builds on increases of 750,000 in February and 504,000 in January, continuing the steady pace of strong job creation.

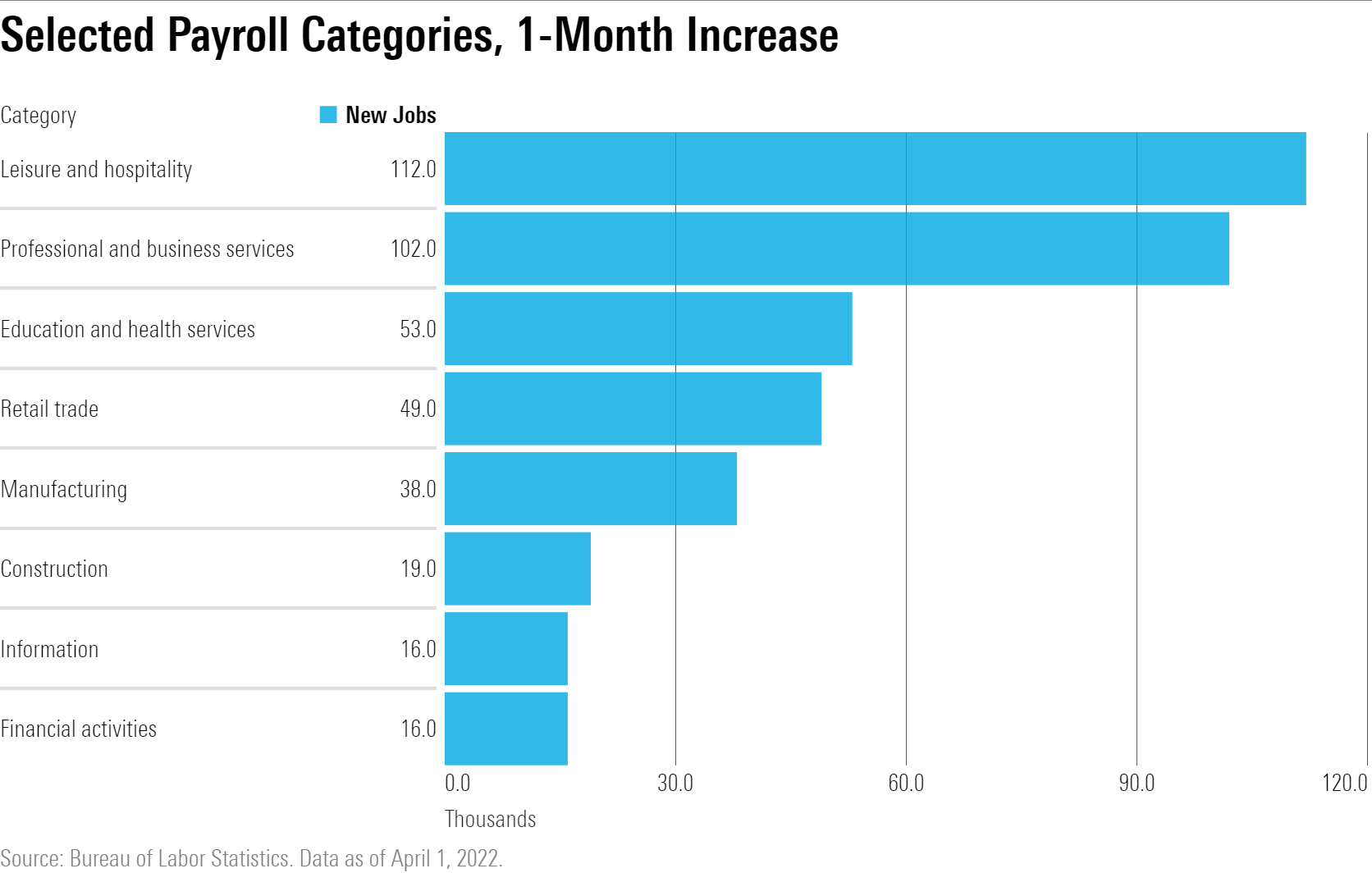

The Labor Department pointed to strong hiring growth in leisure and hospitality, professional and business services, retail trade, and manufacturing.

“The fading effect of omicron was evident, as leisure and hospitality accounted for one-fourth of the nonfarm payroll gains,” says Caldwell.

Still, there remains room for continued growth in the jobs market. While overall employment is now approaching pre-pandemic levels, industries such as leisure that took a big hit from the economic lockdowns of 2020 haven’t yet fully recovered.

Unemployment Nears Pre-Pandemic Lows

With the latest drop in the unemployment rate, this key measure on the economy is approaching levels seen before the pandemic--and levels that are well below where unemployment has for the most part been in recent decades.

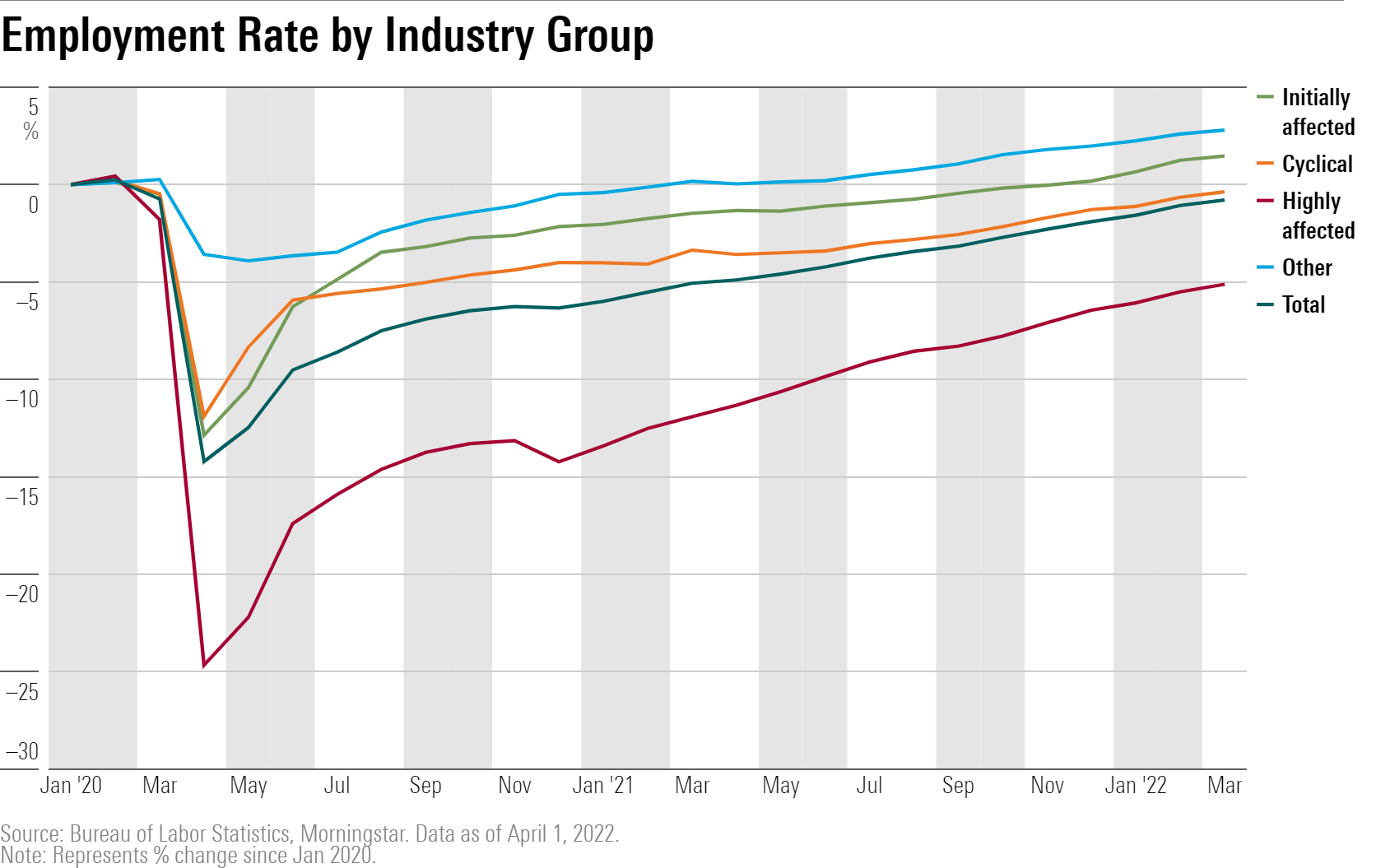

Another sign of health for the jobs market was an increase in the labor force of 418,000 in March. That, says Caldwell, is “a sign that constraints on labor supply are lifting.” He notes that the participation rate for prime age workers--ages 25-54--increased by 0.3%, and now stands just 0.5% below pre-pandemic levels.

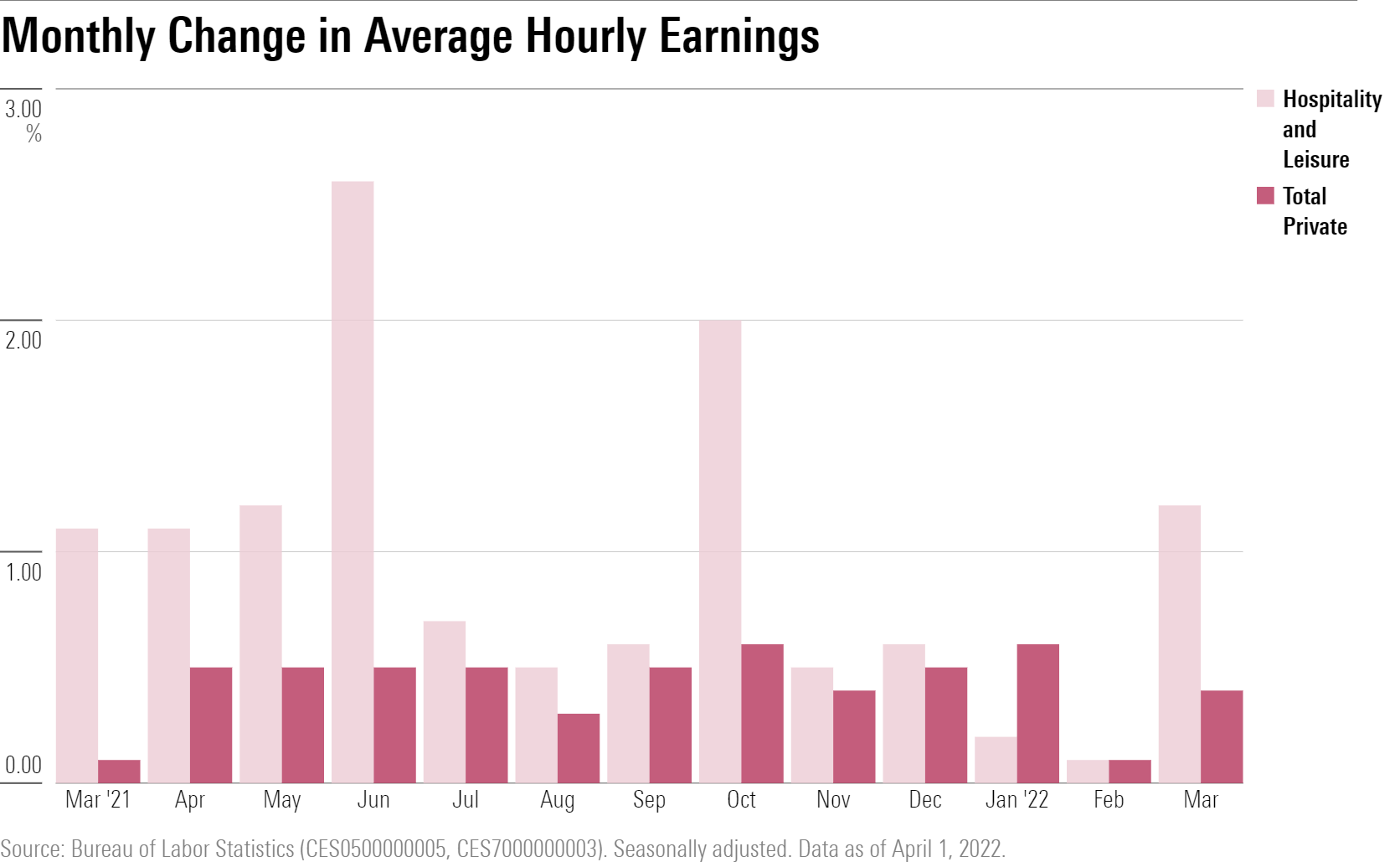

Wage Increases Cool Off

On the wages front, average hourly earnings rose by 13 cents, or just over 0.4% in March. That follows an essentially flat reading for wages in February, where hourly earnings rose by just 1 cent.

The small increases in wages for February and March could help ease concerns about a wage-price spiral that would further fuel already high inflation rates.

“Improvement in labor supply kept wage growth at a moderate pace of 0.4% in March,” says Caldwell. “Given last month's low reading of 0.1%, it's possible that wage growth is now trending downwards.”

Still, one sign of ongoing upward pressure on wages came from leisure and hospitality.

“The rapid rate of hiring in this industry led to a 1.2% increase in leisure and hospitality wages, far outpacing the average,” Caldwell notes.

Jobs Report Leaves Fed on Track for Rate Hikes

The continued strong readings on employment come as the Federal Reserve is shifting gears away from the easy-money policies set in place to support the economy during the pandemic. In March the Fed kicked off its tightening of policy with a quarter-point increase in the federal-funds rate from zero. Bond markets are currently pricing in half-point increases at both the May and June policy-setting meetings.

“Today's report probably doesn't change the Fed's near-term plans, with the Fed expected to bring the Fed Funds Rate to 1.75% by its July meeting--up from 0% at the beginning of the year,” Caldwell says. “However, if wage growth continues to trend down, that could lead to a slower pace of monetary tightening in the second half of 2022 and onwards, depending on other factors, such as resolution of supply chain issues and oil prices.”

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ba63f047-a5cf-49a2-aa38-61ba5ba0cc9e.jpg)