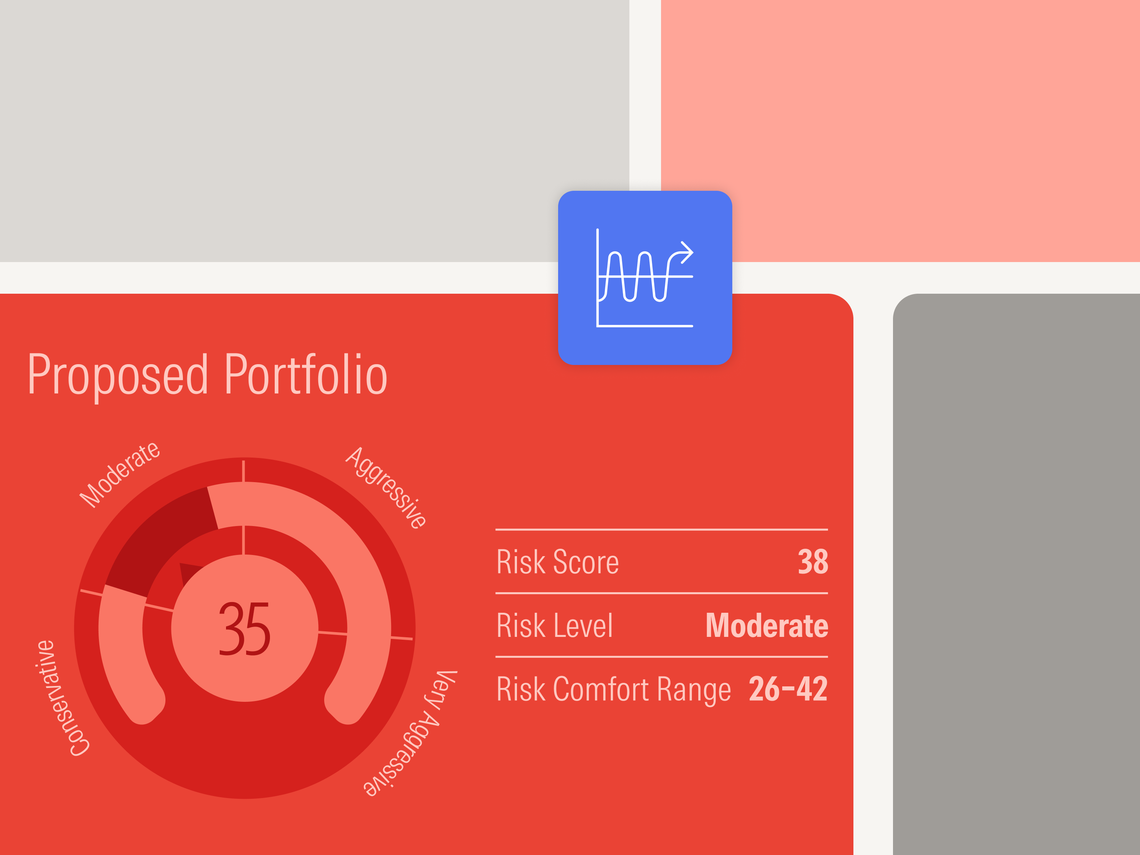

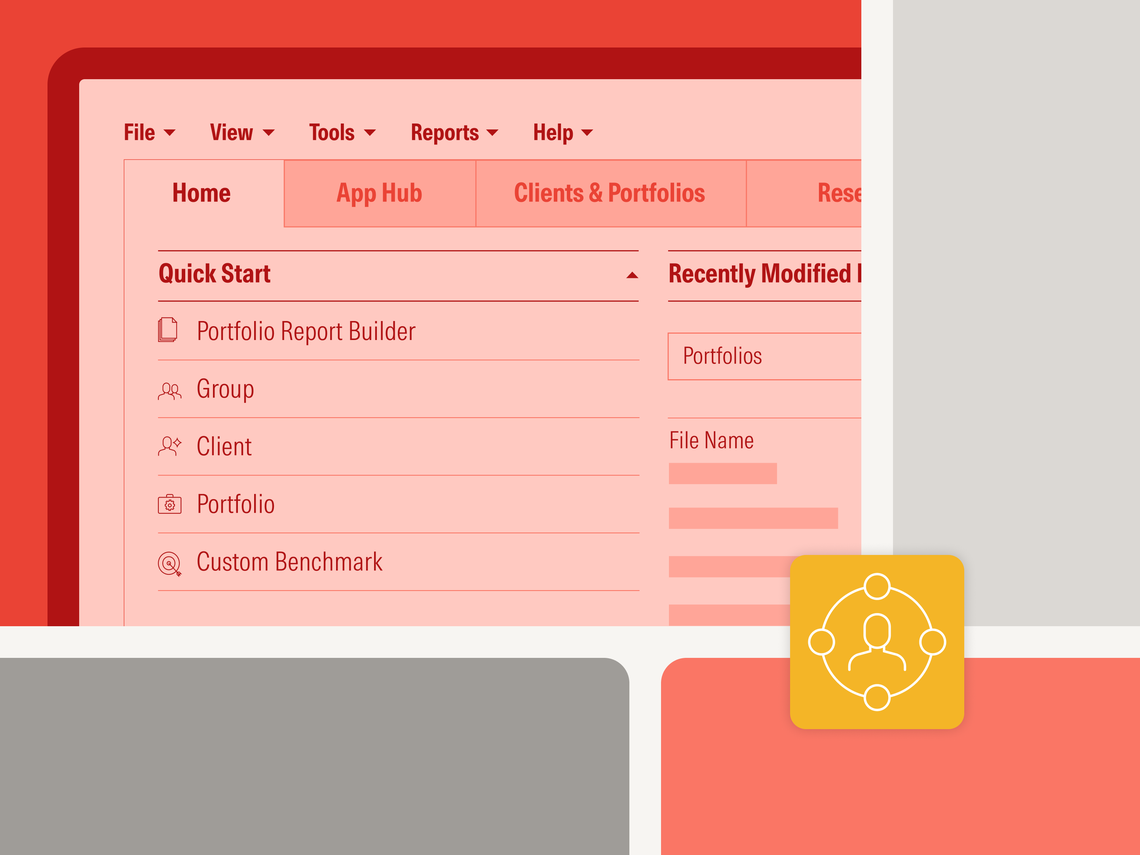

Third-party model portfolios are closing in on $1 trillion in assets under management. Are they worth it?

Structural limits may confine Starlink's true market opportunity to complementary connectivity segments rather than the full telecom landscape.

AI is everywhere in asset management conversations. But our research shows that real adoption is still fairly limited.

Discover the latest global market analysis, bond and fund performance, economic indicators, and more.