It's Hard to Argue for High-Active-Share Funds

Investors in highly differentiated funds have mostly endured higher risk while paying higher fees for mostly mediocre relative returns.

/s3.amazonaws.com/arc-authors/morningstar/5dd7882e-0413-4eb1-b7f0-3d3ed94328e7.jpg)

A key selling point of many actively managed equity mutual funds is their promise to look starkly different from their benchmarks. Asset managers labeling funds "high-conviction," "best-ideas," "focused," or "opportunistic" put a positive spin on this difference and typically tout the supposed advantages of their investment approaches.

These same managers often suggest that funds closely resembling their indexes won’t outperform. The solution, they imply, is to invest in a fund that diverges widely and gives its management team latitude to invest wherever it thinks the market’s best opportunities await. The degree to which a portfolio invests differently from an index is popularly measured by “active share.”

This intuition comes easily to clients, but until recently they have mostly been unable to contextualize their investment options and gauge whether highly differentiated funds are worth the higher risks and fees they are likely to incur.

That's what Morningstar explored in a new active share study. We surveyed the current and historical active-share predilections of domestic open-end mutual funds and analyzed their performance across the nine U.S.-oriented Morningstar Categories from Jan. 1, 2003, through Dec. 31, 2020. The study sketches a portrait of highly differentiated funds--that is, those with high active share--that is far from attractive. For the most part, we found that clients would have been better off in funds with relatively low active share.

What Is Active Share?

Conceptually, an equity portfolio's active share is the portion of its assets invested in a way that diverges from the index. So, a portfolio precisely replicating the index has 0% active share, while a long-only portfolio full of nonindex holdings has 100% active share.

A fund can achieve active share by owning stocks not found in the index, avoiding stocks in the index, or owning the same stocks within the index but at different weights.

How to Establish a Fund's Level of Active Share

Each Morningstar Category's median active share is closely tethered to the composition and concentration of its benchmark. At year-end 2020, large-growth's 60% median active share ranked lowest of all domestic categories as the combined share of the 10 largest constituents within its category benchmark--the Russell 1000 Growth Index--ranked highest at 44%. All six small- and mid-cap categories are more diffuse and have active shares of 85% and above.

Exhibit 1

- source: Morningstar Analysts

Investment universes circumscribed by top-heavy indexes make it more difficult for active managers to build high-active-share portfolios, at least without taking meaningful out-of-benchmark positions.

The varied active-share distributions across categories is another important context for assessing a given fund's active share. Ranges of fund active shares within the large-cap categories are considerably wider than those in the small- and mid-cap categories.

Exhibit 2

- source: Morningstar Analysts

Proper active-share comparisons across categories are thus more difficult than the simple use of absolute measures often suggests. Indeed, while industry participants often deem active share of 80% or above high, that boundary marks the highest quintile for the large-growth category but the lowest quintile for small-growth. Also, the relatively tight range of active shares within the small- and mid-cap categories raises questions about its relevance as a tool to filter, sort, or select funds.

It is better to distinguish various active-share levels within a particular context, such as Morningstar Categories. "High" active share here describes a fund ranking in its peer group's top or fifth quintile on that measure. "Low" active share describes the bottom or first quintile.

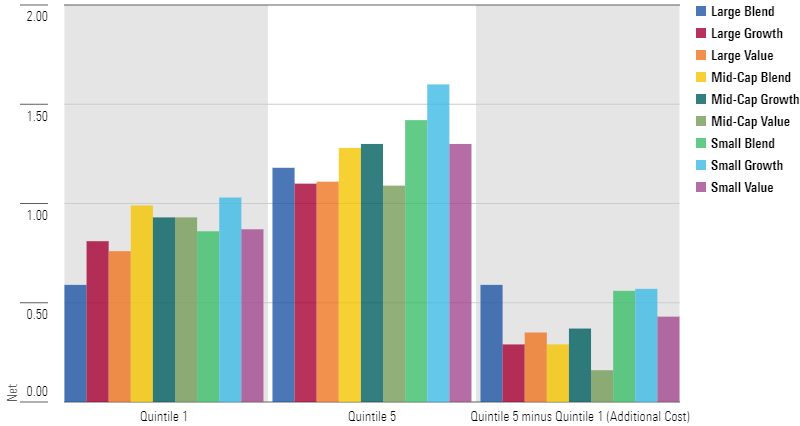

Higher Active Share, Higher Fees

Across all categories and share classes, a typical low-active-share fund (labeled Q1) can be had for between 0.60% and 1.00%, depending on the category. High-active-share funds (labeled Q5) cost between 1.10% and 1.60%.

Exhibit 3: Average Net Expense Ratios at Year-End 2020

- source: Morningstar Analysts

Categories Where High-Active-Share Funds Have an Edge

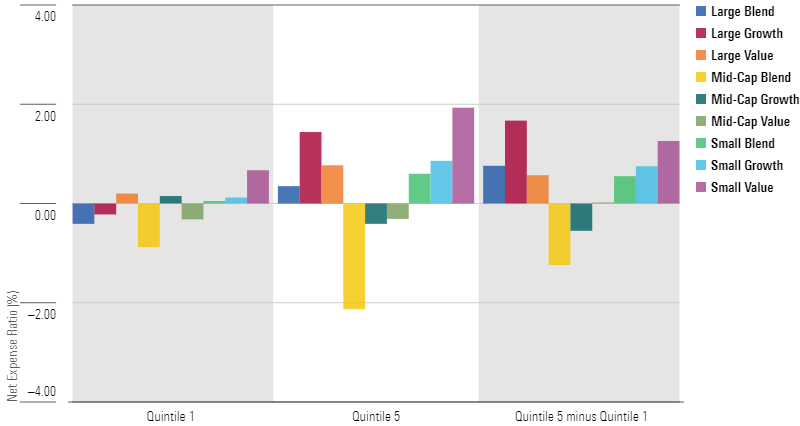

From January 2003 through December 2020, high-active-share funds failed to justify their fee premium in most categories, as measured by their performance over 12-month rolling periods. (Over 36-month rolling periods, their performance was worse.)

Stock-pickers deserve some credit: In five of the nine categories, the highest before-fee excess returns came from the most active funds, which on average exceeded their category indexes between 0.35 and 1.93 annualized percentage points. On the other hand, the high-active-share funds within mid-blend and mid-growth posted their respective category's poorest (and negative) excess returns. Mid-growth's sole cohort to show before-fee outperformance was its lowest active-share quintile.

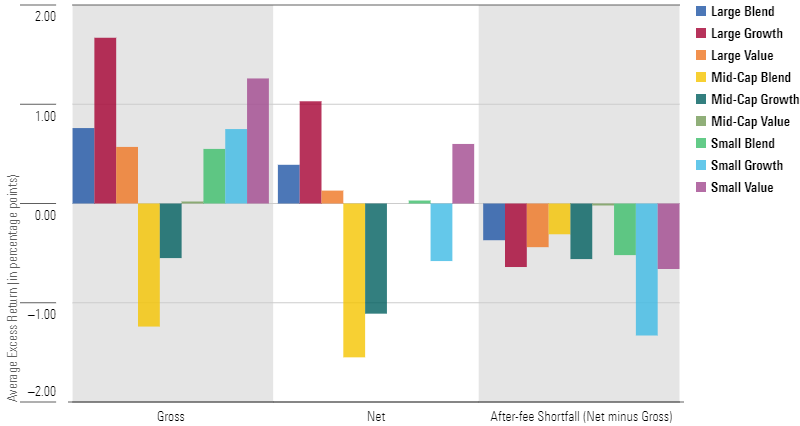

Exhibit 4: Average Gross Excess Returns

- source: Morningstar Analysts

The results implying an advantage for high active share come with a caveat: They are statistically significant only for the large-cap categories. (High-active-share funds' underperformance within mid-blend is also statistically significant.)

The higher costs of high-active-share cohorts so dull whatever performance edge they may have as to raise doubts about their value-add. From before fees to after them, excess returns of the large-blend and -value categories drop to 0.39 and 0.13, respectively, and become statistically insignificant advantages. Within small-growth, the superior gross returns of high-active-share funds become inferior net returns relative to funds with low active shares. There remained a single category whose highly active managers retained a meaningful edge over their low-active-share peers once expenses were settled: large-growth.

Exhibit 5: Average Gross and Net Excess Returns

- source: Morningstar Analysts

High Active Share, High Risk

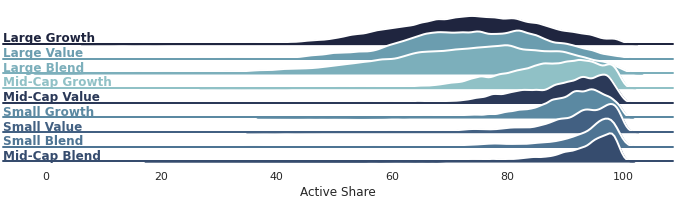

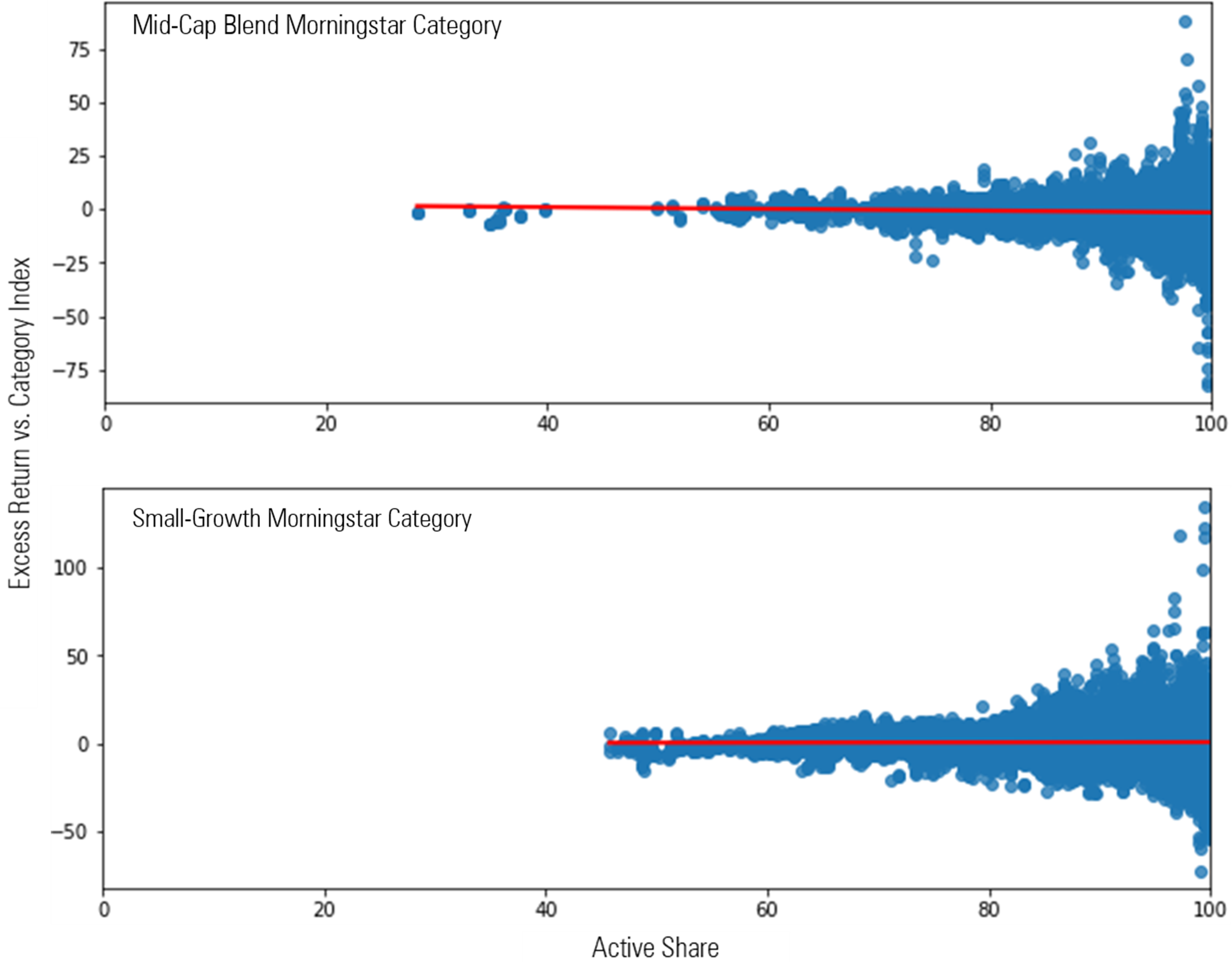

While a fund's category-relative active-share level fails to universally foretell its relative performance, it bears a consistent and tight relationship to a variety of risk measures, such as volatility of returns (as measured by standard deviation), tracking error (the volatility of excess returns versus the benchmark), and portfolio concentration (as measured by percentage of holdings in its top 10).

In the context of both gross and net returns from 2003 through 2020, the highest-active-share funds in all but one category showed much greater volatility and tracking error than those with low active share. Funds' dispersion of returns typically rises as their active share rises.

Exhibit 6: Active Share vs. Rolling 12-Month Excess Return, 2003-20

- source: Morningstar Analysts

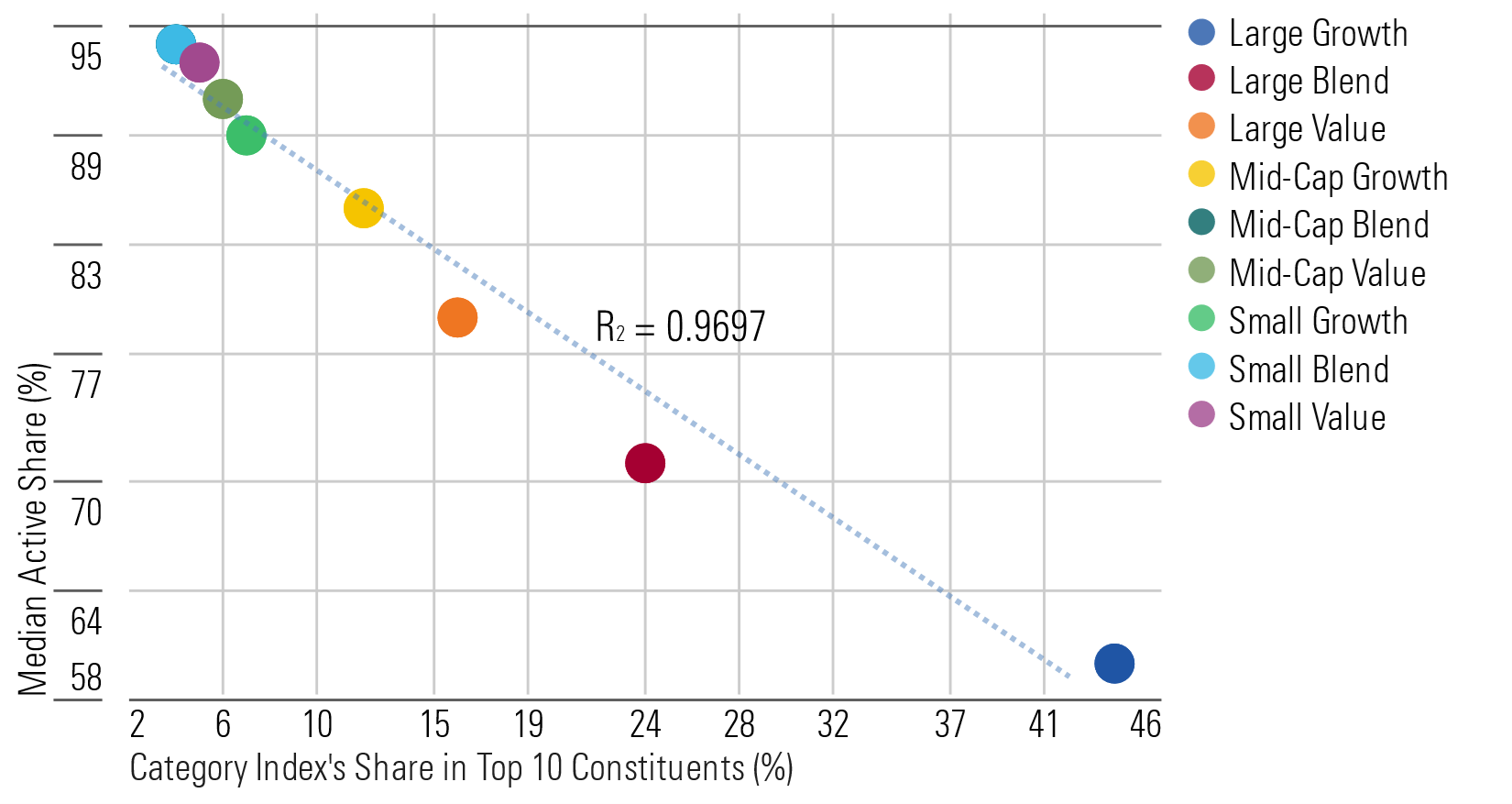

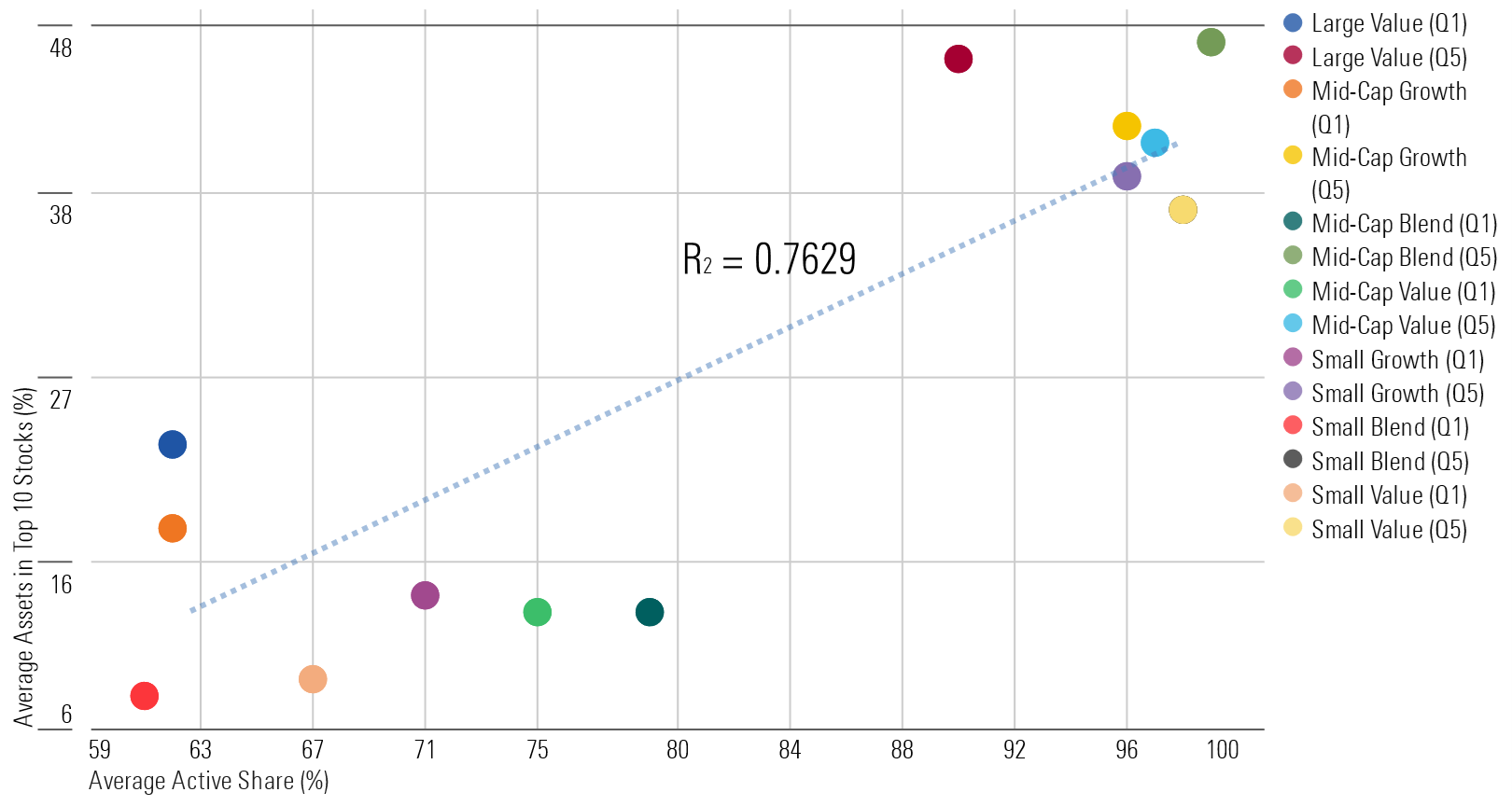

Funds often achieve their high active shares (and higher volatility) by holding relatively few stocks or otherwise devoting a large chunk of their assets to top positions. Across all categories, they typically have the highest levels of portfolio concentration--as measured by the percentage of assets in their top-10 stocks--relative to peers and therefore less stock-level diversification. This magnifies the impact of investment mistakes and the risk of missing out on the market's biggest winners.

Exhibit 7: Average Active Shares (x-axis) and Average Assets in Largest 10 Stocks (y-axis) by Select Categories and Active-Share Quintiles as of Year-End 2020

- source: Morningstar Research. Data as of Dec. 31, 2020. The dots for Small Blend and Small Value overlap. This illustration excludes large-blend and large-growth categories, given that their respective indexes' unusual top-heaviness in recent years has contributed to a substantial narrowing of the differences between their quintile concentrations.

The Bottom Line on Active Share

Active share isn’t without value. The connection between a portfolio's differentiation from its index, its concentration, and volatility can help to classify funds by their investing style and risk level. But active share is fraught with pitfalls when used as a tool to identify superior active strategies.

High-active-share funds are relatively expensive and have shown an undesirable risk profile over the long run. While it's true that the best-performing funds tend to be those with high active shares, the same is true for the worst performers.

There is little use of applying active-share screens--for instance, a minimum threshold--to funds in the small- or mid-cap categories because the high-active-share cohort posted among the weakest results within mid-caps from 2003 through 2020 and its advantage within small caps was statistically insignificant. The before-fee advantage for high-active-share funds has shown to be statistically significant only for large-cap categories.

These findings should not be taken as a signal to swear off highly differentiated funds. Across all domestic categories, there are high-active-share funds whose skilled portfolio managers and strong, risk-minded investment processes make them worthy long-term holdings.

Instead, the findings serve as a cautionary tale for asset owners or advisors tempted to pay more than they should for the funds with second-rate investment teams or poorly devised processes that can lead to volatile and inferior net returns. With higher active share comes a higher risk of disappointment.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/5dd7882e-0413-4eb1-b7f0-3d3ed94328e7.jpg)