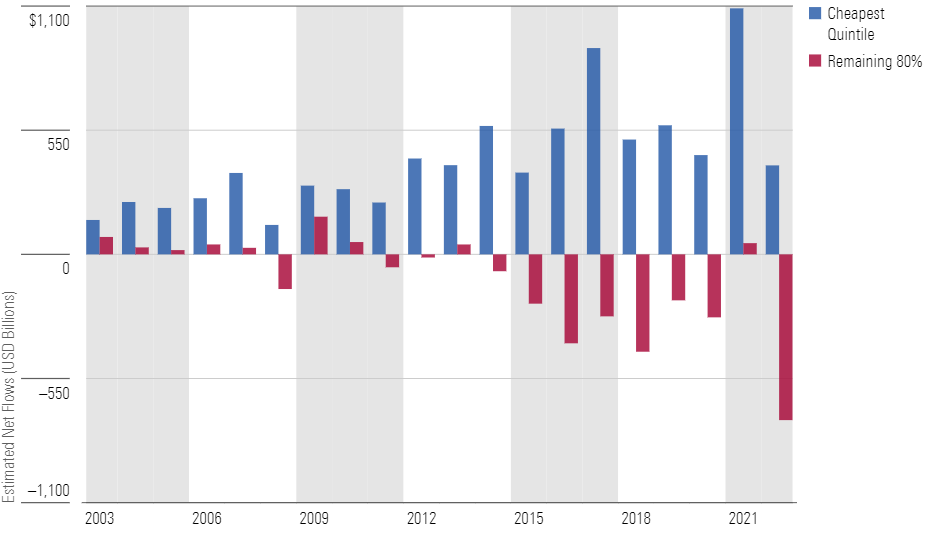

Investors Piled Into the Cheapest Funds in 2022

The cheapest quintile of funds had a $1.1 trillion advantage in net flows over the remaining 80% of funds.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

The average expense ratio paid by fund investors has been falling for two decades.

In 2022, the asset-weighted average expense ratio across all mutual funds and exchange-traded funds (not including money market funds and funds of funds) was 0.37%. This is less than half of what investors paid in fund fees, on average, in 2002.

Fund investors themselves deserve much of the credit for this movement, as the shift toward low-cost funds has been the primary driver of this decline. While there’s plenty to celebrate, investors shouldn’t stop here. Although fund costs have come down, the total costs borne by investors haven’t necessarily followed in lockstep.

Some costs have diminished, while others have taken new shape. For example, the cost of advice has increasingly been stripped out of funds’ fees and resurfaced in the form of advice fees. Investors should be ever vigilant of what Vanguard founder John Bogle referred to as “the tyranny of compounding costs,” and keep account of what they’re paying for their investments and advice.

Here’s a closer look at some of the key takeaways from Morningstar’s latest annual fund fee study.

A Modest Decline in Fund Fees Saves Investors Billions

Asset-weighted fund fees fell to 0.37% in 2022 from 0.40% in 2021. This might not sound like much, but it amounted to $9.8 billion in savings for fund investors. A few billion dollars saved means more than a few billion earned in years to come. This is the second-largest year-over-year decline we have recorded, dating back to 1994. This fee decline is a big positive for investors because fees compound over time and diminish returns.

These savings have disproportionately accrued to investors in passive funds. The asset-weighted fund fee across all passive funds has declined 60% since 1994, landing at 0.12% in 2022. Meanwhile, the asset-weighted fee paid by investors in active funds stood at 0.59% in 2022—a 40% decline over the same period. The trend continued in 2022, as passive funds saw their asset-weighted average fees drop 10% from 2021 compared with 3% for active funds.

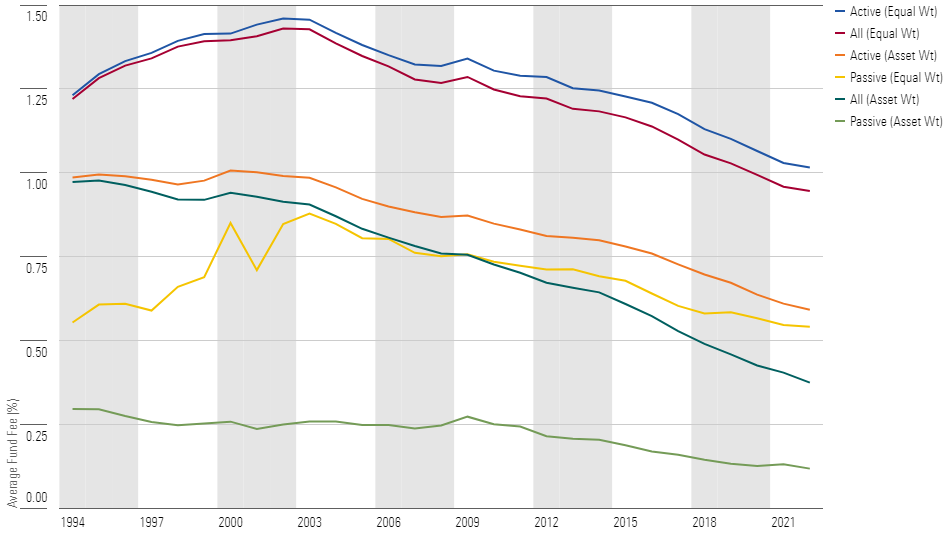

Fund Fees Continued Their March Lower

Investors Deserve Most of the Credit for Declining Fund Fees

Asset-weighted fees have dropped more sharply than equal-weighted fees—meaning the average amount investors are paying for the funds they invest in has fallen more than the toll taken by the average fund. The fact that asset-weighted fees are persistently lower than equal-weighted fees indicates that investors, on average, choose funds with below-average fees.

The chart below shows aggregate flows into all funds based on how their fees stack up versus their Morningstar Category peers. In eight of the last nine years, the cheapest 20% of funds across all Morningstar Categories have, as a group, accounted for 100% of the net inflows into all funds. Money has poured out of the remaining 80% during that time. The sums are staggering: More than $5.4 trillion has flowed into the low-cost cohort during this eight-year span, while $2.6 trillion has been pulled from the remaining funds.

In 2022, the gap in flows for cheap and expensive funds grew into a chasm. For the first time since 2017, the cheapest quintile of funds had a net flow advantage of over $1.1 trillion more than the remaining 80% of funds.

The Gap in Flows Between Cheap and Costly Fund Is Massive

The lion’s share of flows into low-cost funds has gone to index mutual funds and ETFs. These funds’ growth has been driven by a variety of factors: notably, shifting investor preferences, the evolving economics of the financial advice industry, and the ascendance of target-date funds as the default investment option in retirement plans.

- Investors’ tastes can be fickle, but the trend toward indexing in general and ETFs in particular appears to be durable. Disillusioned with active managers—and fed up with high fees and regular capital gains distributions—investors of all stripes have flocked to low-cost, tax-efficient index funds.

- In the advice space, the shift away from transaction-driven business models and toward fee-based ones has led advisors to recommend lower-cost funds to their clients to, in part, make more room for their own fees, which are often charged as a percentage of client assets under management.

- In the retirement space, target-date funds have experienced significant growth as they are now the default investment option in many retirement plans. The majority of target-date fund assets are now in target-date series composed exclusively of index mutual funds.

Taken together, these three factors help explain the sea change we have witnessed from active funds to passive ones, costly ones to inexpensive ones.

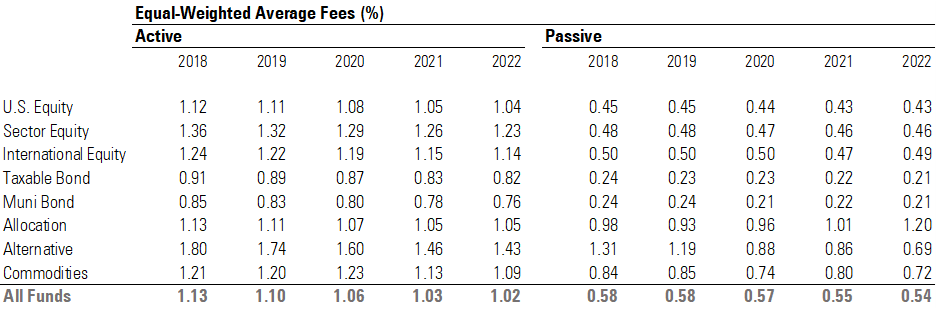

Fund Fee Trends in Active Versus Passive Funds

The table below shows the trend in equal-weighted fees for active and passive funds across Morningstar Broad Category Groups. From 2018 through 2022, the average expense ratio for passive funds dropped 7% and the average fee for active funds dropped 10%.

Fund Fees Charged by Asset Managers Represented by Equal-Weighted Fees

Fund companies are charging investors less than they were five years ago, partly because they are dropping certain line items from investors’ bills. As advice (such as loads) and marketing and distribution costs (such as 12b-1 fees) get scrapped to reflect the evolution of advisory practices, fund fees are getting stripped down to manufacturing costs (that is, management fees). This effect has been most pronounced among active funds, where these expenses are—or at least were historically—most prevalent.

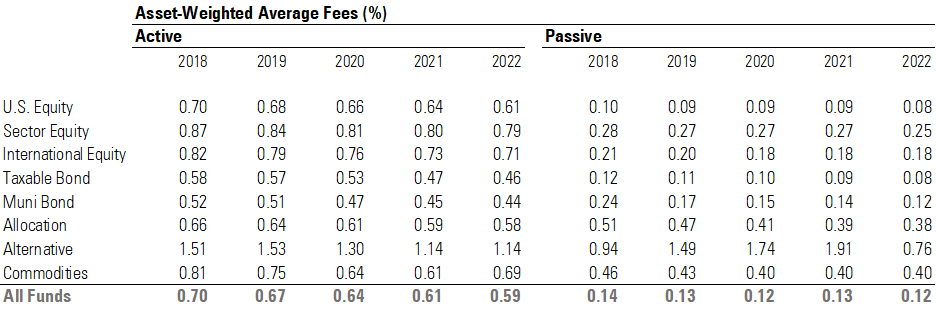

The table below shows the trend in asset-weighted fees for active and passive funds across Morningstar Broad Category Groups. From 2018 through 2022, the asset-weighted average expense ratio for passive funds dropped 19%, while the asset-weighted average fee for active funds dropped 15%.

Investors' Average Fund Costs by Asset-Weighted Average Fees

The rate of change in what investors pay, on average, for passive funds has been much greater than the rate at which these funds’ fees have fallen. This reflects how acutely price-sensitive investors have become in this segment of the market. Broad-based market-cap-weighted index funds have become a commodity product. Differences in fees have become razor-thin; high-fidelity index-tracking performance is table stakes. Market beta has become, for all intents and purposes, a public good.

Pressure on Fund Fees Is Here To Stay

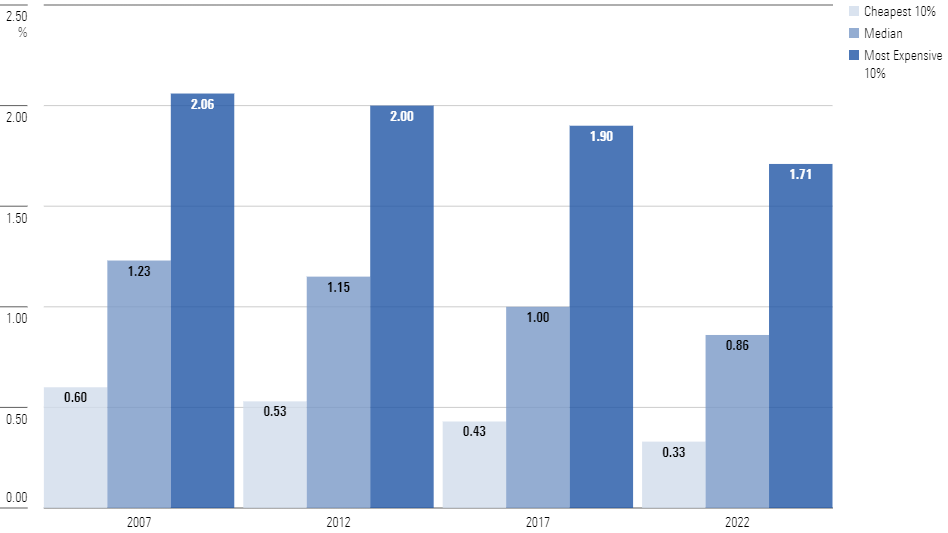

Below, you can see the summary fee breakpoint data for funds over the past 15 years. This provides further evidence that the trend in fees has been friendly to investors. Not only has the median fund gotten cheaper over the past 15 years, the most expensive ones have, too. The most encouraging figure is the one representing the level that divides the cheapest 10% of funds from the rest. At 0.33%, this breakpoint was 45% lower in 2022 than it was in 2007.

Cheap Funds Are Getting Cheaper, Expensive Ones Are Trying To Gain Ground

The downward pressure on fund fees is unlikely to abate. Competition has driven fees close to zero in the case of many index mutual funds and ETFs. The same forces that spawned these low-cost funds tracking major indexes have begun to spread to other corners of the fund market, areas where there is still ample room for fees to fall further.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)