Take It From Warren Buffett: Misses Are Inevitable

Embrace these timeless investing principles and you can still attain remarkable outcomes.

Woodstock for capitalists takes place the first Saturday in May.

That’s a reference to the Berkshire Hathaway BRK.A BRK.B annual shareholders meeting. More than 30,000 people fill an arena in downtown Omaha—standing-room only—seeking business updates and general investment wisdom from Warren Buffett.

The weekend of the event, hotel rooms at the Hilton Omaha across the street from the meeting venue were fetching $2,500 per night. And it’s a two-night minimum, meaning $6,000 after taxes for the weekend stay.

Put simply, demand is high.

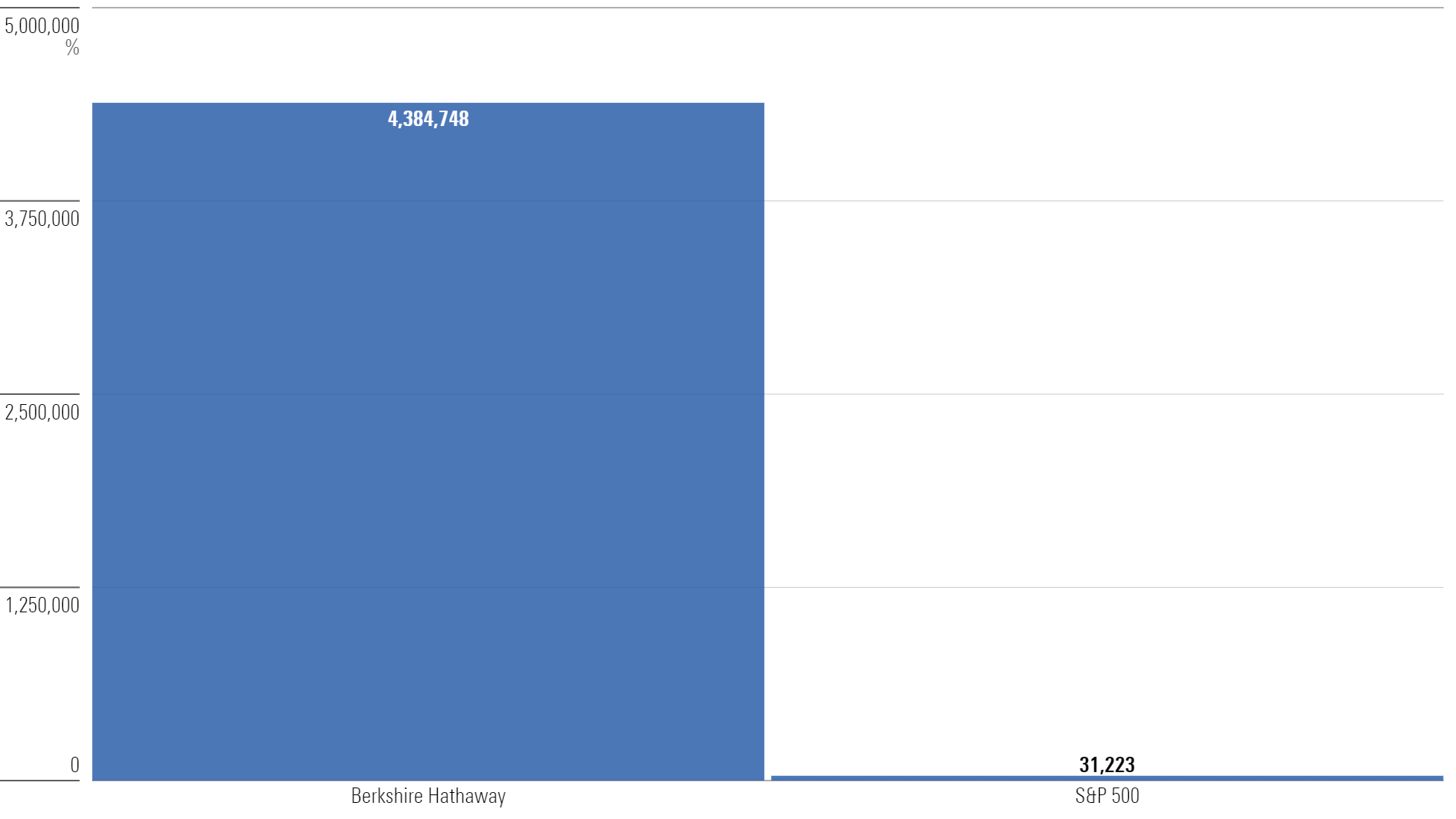

The reason is obvious: Buffett—and Berkshire—have a nearly 60-year track record of delivering consistent results. According to Barron’s, Berkshire shares could fall 99% and remain ahead of the S&P 500′s total return since 1965, when Buffett took over.

Berkshire’s total returns work out to a cumulative gain of more than 4,000,000%. The S&P 500 returned more than 31,000% in the same span, but when you compare the returns side by side, it appears the S&P returned nothing. That’s how outstanding Berkshire’s long-term track record has been.

Cumulative Return (1965-2023)

But a funny truth about Buffett: He’s often more inclined to discuss mistakes rather than celebrate success.

As one example, the 2018 Berkshire annual meeting had a question from a shareholder, who asked:

“You have gotten into the tech world (purchasing) Apple AAPL. You have Bill Gates sitting (in the front row today). I’m just wondering why you’ve never bought Microsoft?”

Laughter broke out as Gates, then a Berkshire board member, smiled while sitting in a folding chair near the stage where Buffett was answering questions.

With usual candor, Buffett remarked, “It’s very clear. The answer is stupidity.”

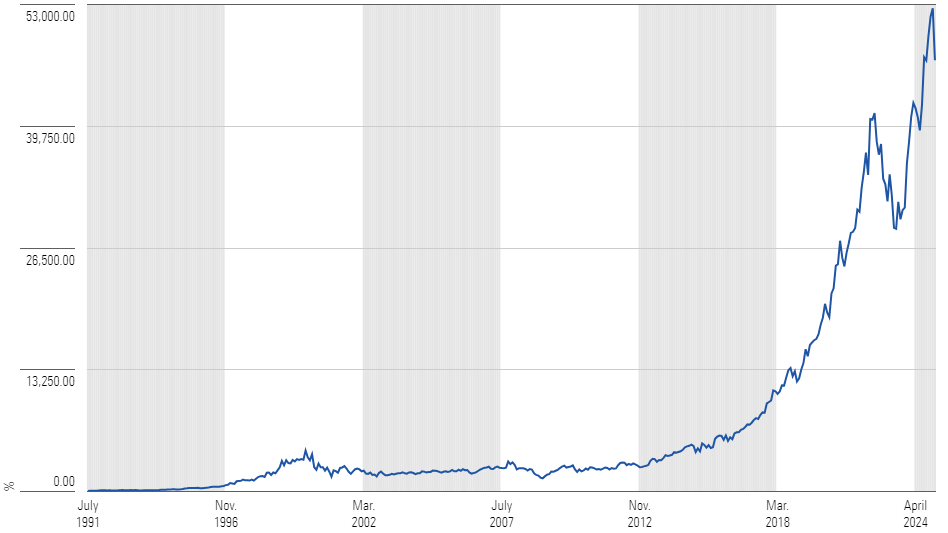

Buffett and Gates have known each other since at least 1991. When they initially met, Microsoft MSFT was a publicly traded company valued at around $10 billion. Today, Microsoft is worth nearly $3 trillion.

More than a 44,000% return left on the table—a giant miss.

Microsoft Total Return Since Buffett and Gates First Met

How did missing Microsoft impact Buffett or Berkshire shareholders?

Probably not at all.

Buffett’s aversion to technology stocks has been well-documented. Even if he bought Microsoft in 1991, it’s not obvious he would have held it for 30 years. That was a period when the business went through multiple transformations: starting in computer software, moving into video game manufacturing, and then an aggressive expansion into cloud computing.

Buffett was a fan of betting on horses at an early age—detailed in Alice Schroeder’s book, The Snowball—and enjoyed the process of handicapping, only placing wagers when he believed the odds favored him.

In the case of Microsoft, he didn’t believe the business moat—one that would protect Microsoft from competition—was strong enough.

But he did identify moats across Geico, American Express AXP, Coca-Cola KO, Gillette, and countless others where he believed the odds were advantageous. And he felt more comfortable about the future for each.

It’s easy to think Microsoft was “a miss,” but the opportunity cost is unknowable. Buying Microsoft could have taken his attention away from the many other businesses that delivered great investment outcomes in the decades that followed.

Buffett finished answering the question, stating, “We missed a lot in the past, and I suspect we’ll miss a lot more in the future.”

If one of the world’s great investors can brush off a perceived miss, maybe the rest of us should, too, whether it be Nvidia NVDA, bitcoin, or any other shiny object.

Getting a few simple things right over an investment lifetime—and less emphasis on home-run hitting—will carry most of the freight.

For many, the simple things—while not all encompassing—can be distilled down to a few key ideas:

- Save more than you spend

- Diversify across asset classes

- Invest regularly (even during bear markets and corrections)

- Be mindful of costs

- Don’t panic during selloffs

Recognizing the impossibility of participating in every winning investment is crucial, a principle even Buffett acknowledges. By prioritizing timeless investing principles and embracing simplicity whenever feasible, investors can still attain remarkable outcomes.

The author or authors own shares in one or more securities mentioned in this article. Find out about Morningstar’s editorial policies.

Morningstar Investment Management LLC is a Registered Investment Advisor and subsidiary of Morningstar, Inc. The Morningstar name and logo are registered marks of Morningstar, Inc. Opinions expressed are as of the date indicated; such opinions are subject to change without notice. Morningstar Investment Management and its affiliates shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Before making any investment decision, please consider consulting a financial or tax professional regarding your unique situation.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KWYKRGOPCBCE3PJQ5D4VRUVZNM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TZEZ6FJNTZEZRC3FBWCWXTXVOQ.jpg)