The Model Portfolio Landscape in 6 Charts

Illuminating the rising popularity of model portfolios.

/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)

Model portfolios continue to gain traction. Over the nine months through March 2022, assets following model portfolios grew by an estimated 22% despite a volatile market. Model providers have taken notice, delivering a variety of offerings to help meet the needs of advisors and their clients. As of May 2022, more than 2,400 models were reported to Morningstar’s database, 30% of which were launched since 2019.

In our recently published 2022 Model Portfolio Landscape, we review the assets following models, the increasing breadth of offerings available, the advantages models provide, and highlight Morningstar’s ratings. We also provide an overview of the avenues for accessing and implementing models.

Below, we’ve highlighted six exhibits from this year’s report that emphasize some of our key findings.

The Total Assets Following Model Portfolios Are Growing

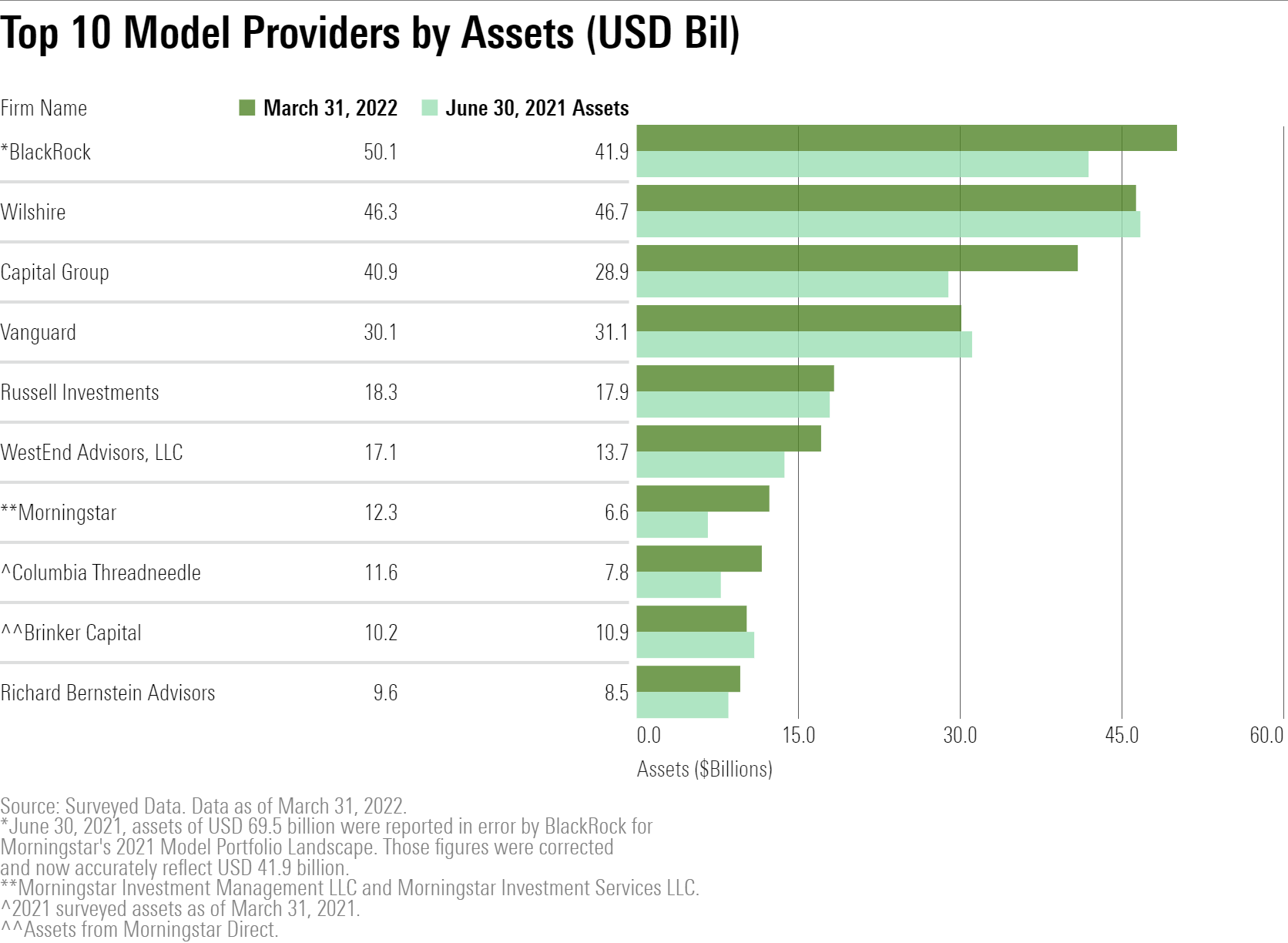

Over the nine months through March 2022, assets following models quickly rose to USD 349 billion, a 22% increase. The table below highlights the top 10 model providers by assets.

BlackRock leads the pack with USD 50.1 billion in assets across its U.S. model portfolios, with the majority of the assets following its target allocation exchange-traded fund series, which has a Morningstar Analyst Rating of Gold. Within USD 10 billion of that mark stand Wilshire Associates and Capital Group. Capital Group’s USD 12 billion increase in assets helped it jump past Vanguard to third on the list. Notably, three of the top 10 providers are strategists—firms that usually lack proprietary products and instead tap third-party strategies to build their model portfolios. WestEnd Advisors leads this group with USD 17.1 billion in assets, a 25% increase over the trailing nine months. Brinker Capital and Richard Bernstein Advisors round out the trio.

Tracking the total assets following model portfolios can be a difficult task. The reported figures are a conservative estimate. For this report, we have both surveyed model providers under Morningstar analyst coverage and leverage the reported assets in Morningstar Direct.

The Breadth of Model Portfolio Offerings Continues to Expand

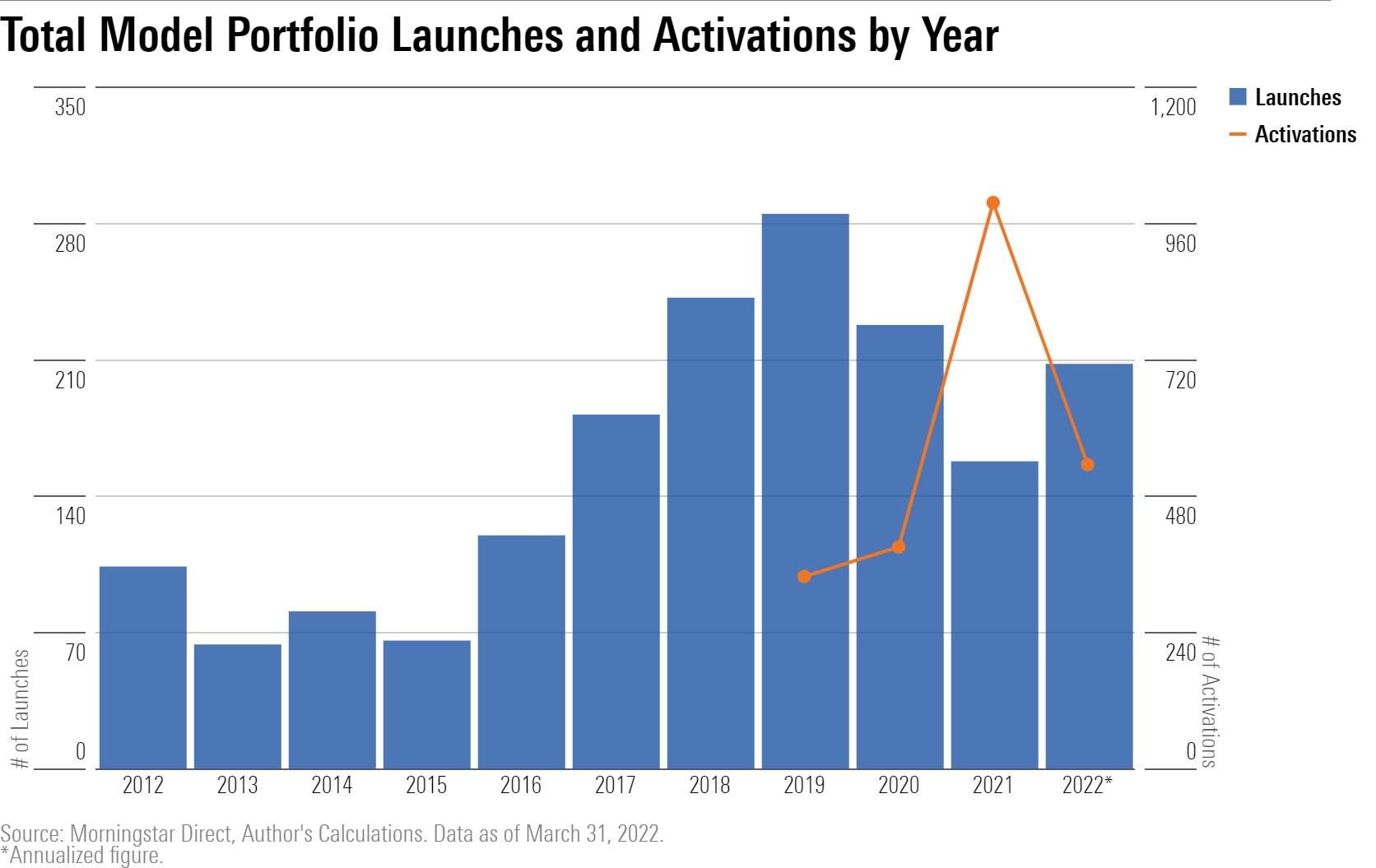

Newly launched model portfolios are coming to market at a quick pace, inundating investors with a plethora of options to choose from. The chart below shows the number of model portfolios launched over the past decade, as well as the number activated since Morningstar’s models database was established. Launches are based on a model’s inception date, while activations are based on the date a reported model is added to Morningstar’s database.

Model portfolio launches were on a tear in the mid-to-late 2010s, posting four consecutive years when growth in absolute models outpaced the year prior. Though the rate may have slowed recently, there were still over 150 individual launches in both 2020 and 2021. Plus, over 50 models have already launched through the first quarter of 2022.

Asset-Allocation Models Remain Dominant, but We Are Seeing Pickup Elsewhere

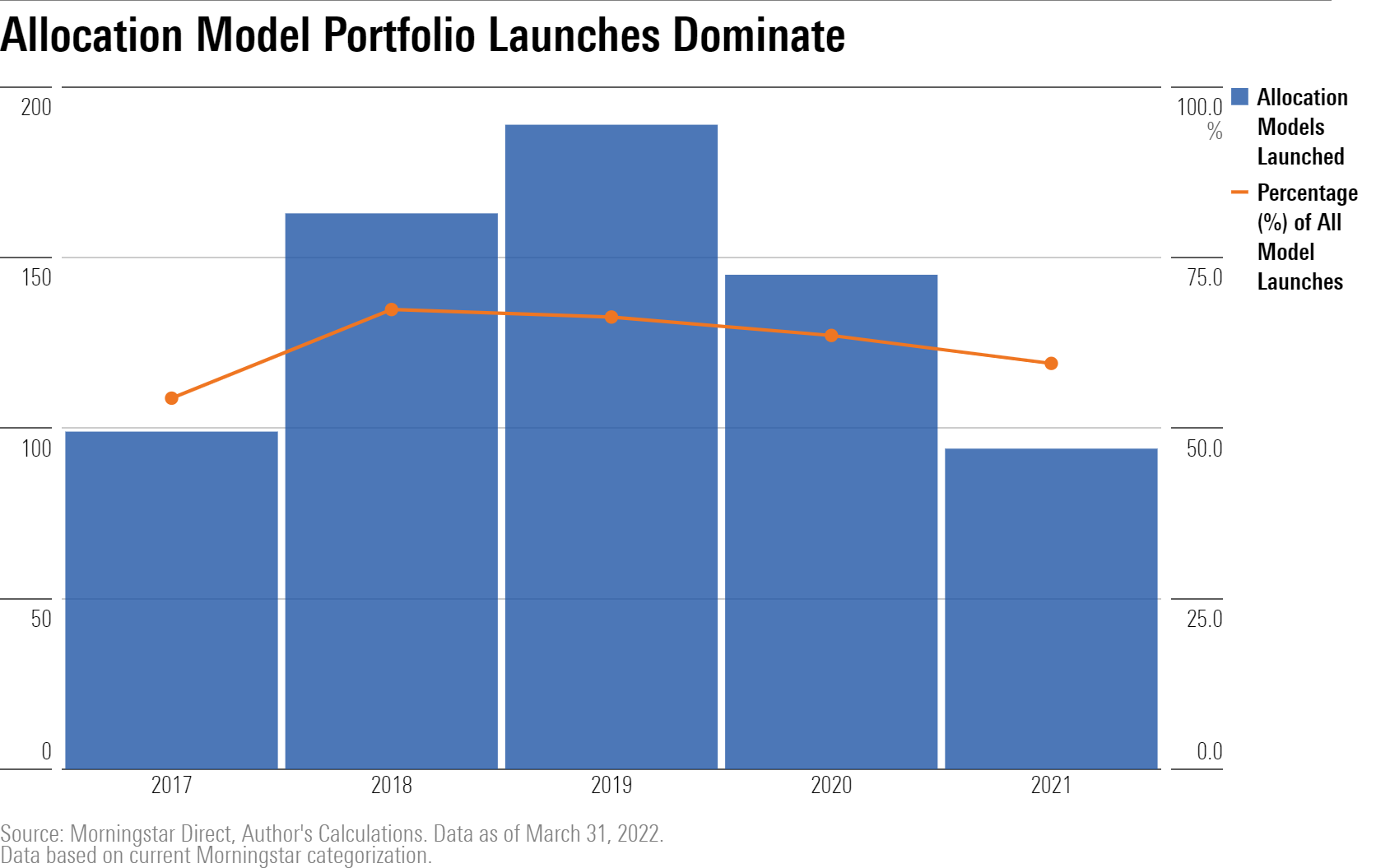

Asset-allocation models continue to dominate the space. As of March 2022, asset-allocation model portfolios falling in Morningstar’s five equity allocation categories accounted for over 70% of the total models in Morningstar’s database. The chart below shows the yearly launches of allocation model portfolios and their percentage of total launches.

These models continue to account for the lion’s share of all models available for a few reasons. One of the biggest drivers of their popularity lies in their series format, which delivers a variety of portfolios across different stock/bond mixes. Some series may include upward of 10 individual portfolios.

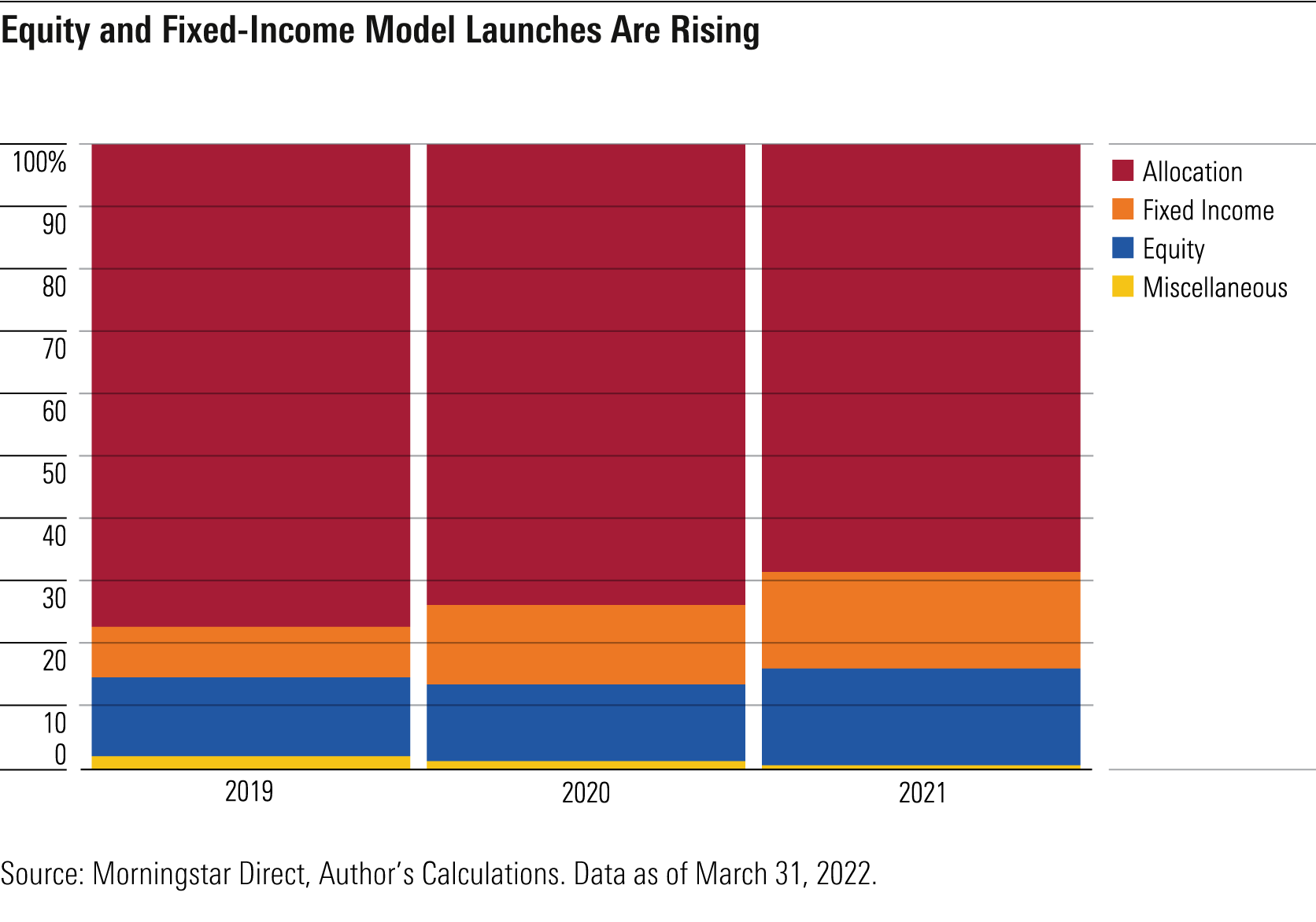

That said, providers are leaning into offerings that fall outside the typical multi-asset construction. For instance, asset-class-specific models are becoming more common as providers look to expand their lineups for advisors and their clients.

The chart below shows the percentage of total new model portfolio launches, broken down by broad asset class: equity, fixed income, allocation, and miscellaneous, which includes more-esoteric model offerings. Over the past three years, equity and fixed-income models have gone from accounting for 21% of new launches to 31%.

These offerings may still be part of target-risk series. For instance, all Dimensional Fund Advisors’ series offer a 100% bonds/0% stocks portfolio, which falls into a fixed-income Morningstar Category. They can also act as stand-alone offerings. Fidelity offers fixed-income models like Fidelity Core Bond and Fidelity Core Plus Bond to function as core or complementary fixed-income holdings for advisors to utilize in client portfolios.

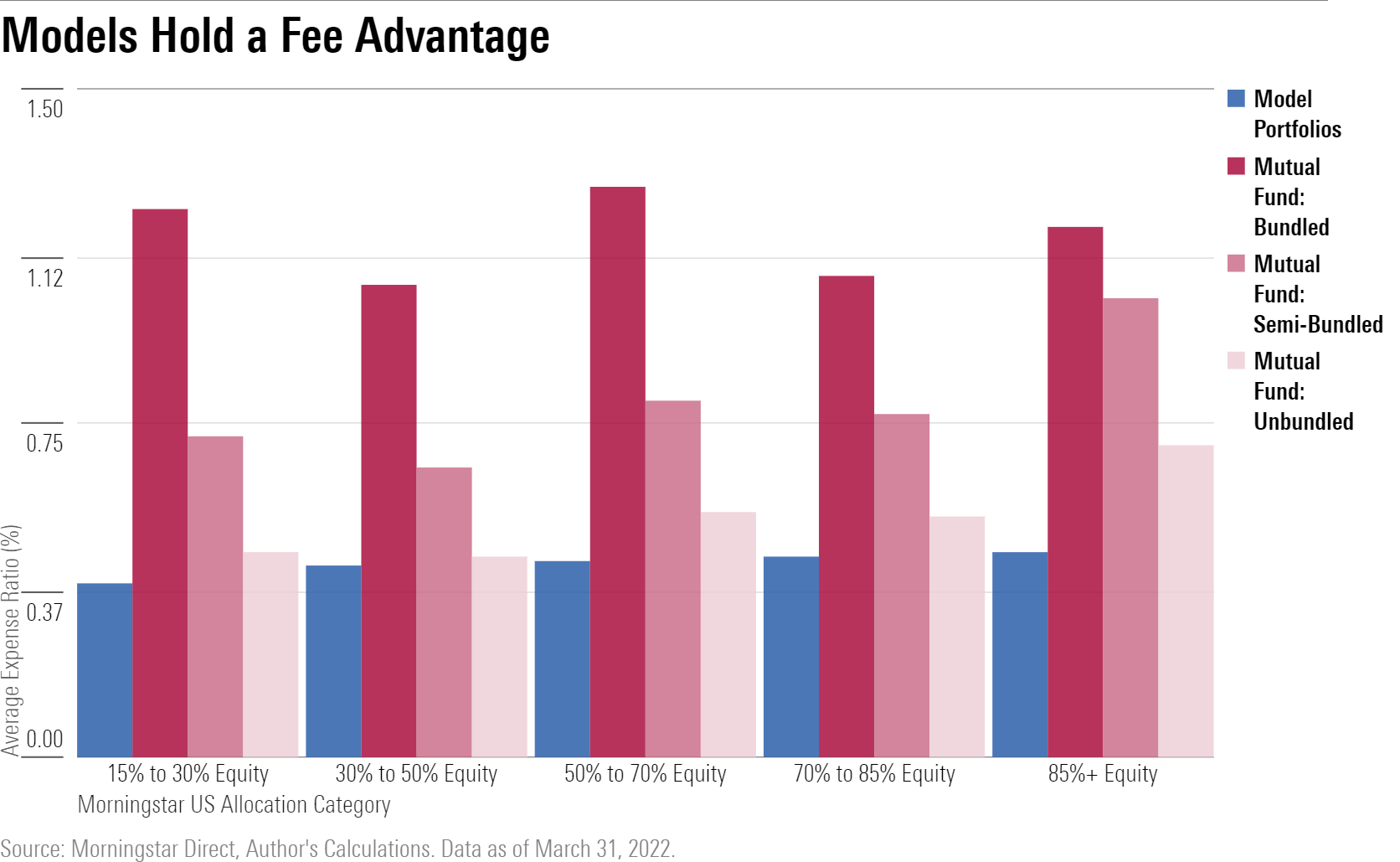

Low Costs Remain an Appealing Characteristic

Model portfolios continue to hold a fee advantage against their mutual fund peers. The chart below compares the average asset-weighted fee for each asset-allocation model versus the average fee of similarly allocated mutual funds, broken down by Morningstar’s Clean Share—Service Fee Arrangement designation. Even when compared against “unbundled” mutual fund shares that have the lowest built-in expenses, a model portfolio charges 11 basis points less on average across all five categories.

The analysis only includes model portfolios with a reported portfolio as of December 2021 or newer. In addition, we do not account for the strategist fee, which some models may layer on as an additional cost.

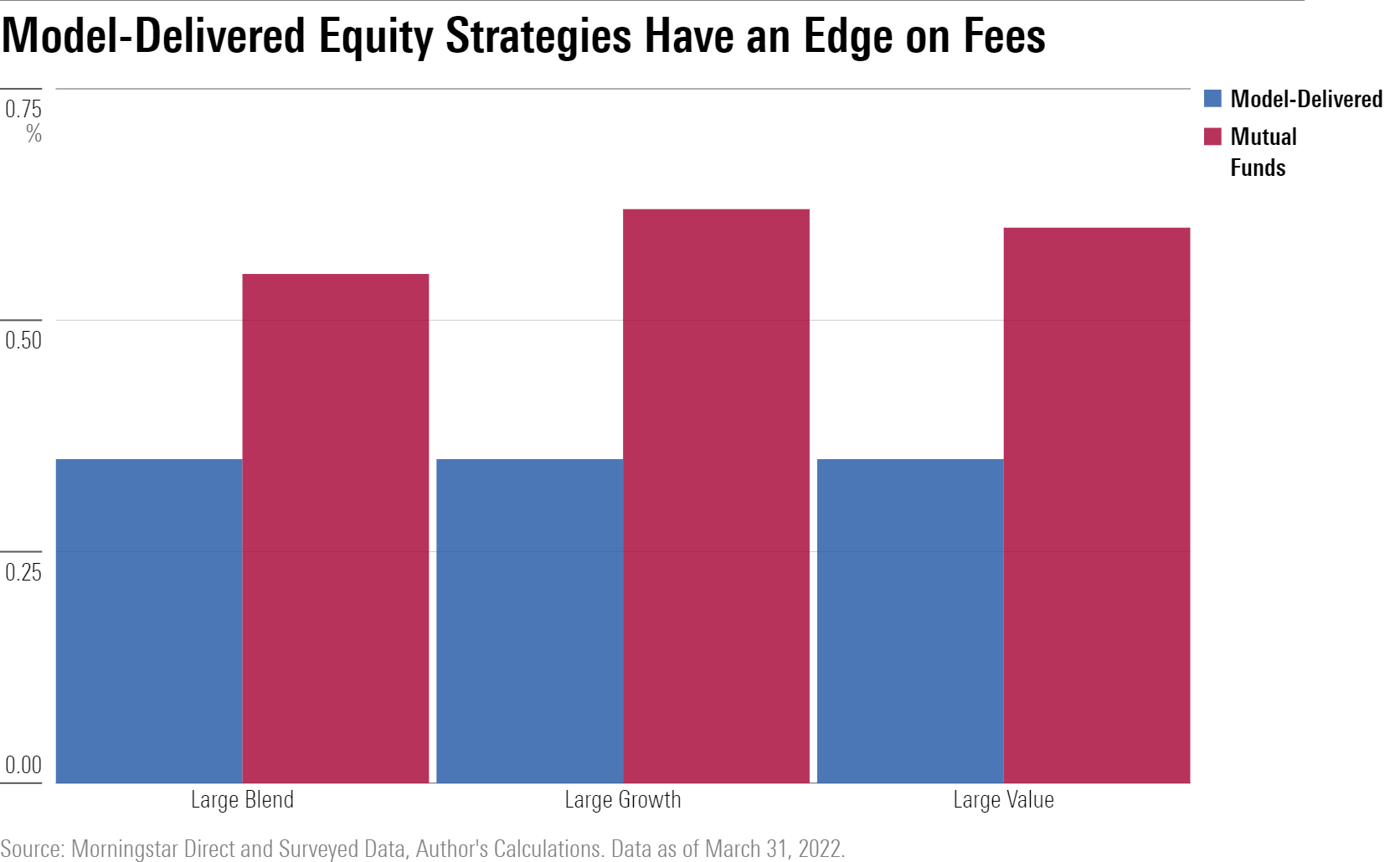

Looking outside of just allocation models, more specific offerings like model-delivered equity strategies also hold a notable advantage when it comes to costs. The chart below compares the average fee for model-delivered equity strategies (based on surveyed data from firms with model-delivery separately managed accounts) with “unbundled” actively managed mutual funds. Across Morningstar’s three U.S. large-cap equity categories, the model-delivered offerings are 20 to 27 basis points cheaper.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KWYKRGOPCBCE3PJQ5D4VRUVZNM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TZEZ6FJNTZEZRC3FBWCWXTXVOQ.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)