What to Consider When Buying a Dividend Stock Fund

They are attractive, but investors should pay heed to more than yield.

/s3.amazonaws.com/arc-authors/morningstar/08b315db-4874-427f-b3b1-f2b84a16e609.jpg)

With the Morningstar U.S. Corporate Bond Index’s yield to maturity at 2.18% as of September 2021, and long-term inflation expectations ranging from 2.4% to 2.5%, bonds are not very appealing. In the short run, they can also hurt if interest rates surge. When the 10-Year Treasury yield more than tripled to its recent high of 1.74% between August 2020 and March 2021, the Morningstar U.S. Corporate Bond Index lost 4.1%, while the Morningstar U.S. Large-Mid Index gained 20.5%. Although bond investors can make some of that money back when they invest at higher rates, their long-term prospects are still meager.

Dividend stocks, on the other hand, are an appealing bet for income investors who can stomach their risks. Their payouts are more stable than their share prices, the payouts tend to increase over time, and investors who have hung on through downturns have done well. A $100,000 investment in Vanguard 500 Index VFIAX on Feb. 29, 2008, would have suffered the index’s worst 12 months in more than 50 years--a loss of 43.3%--but would have broken even within about three years. At the end of five years, it would have paid nearly $10,000 in dividends and still had almost $114,000 of principal left to yield more.

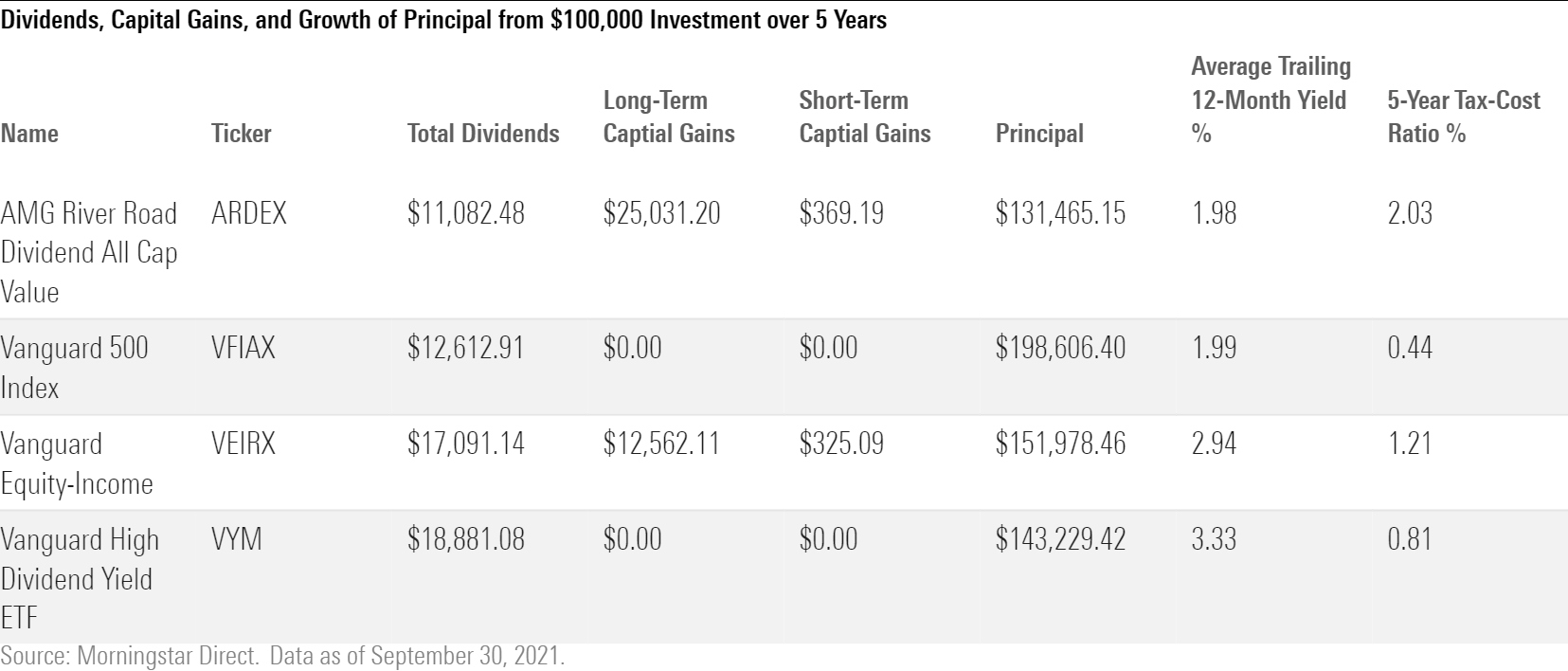

Projected yield is an important consideration in evaluating dividend stock strategies, but it can be misleading, and one shouldn’t forget about fees. AMG River Road Dividend All Cap Value ARDEX had a 3.69% anticipated yield before fees in September 2016 based on its stocks’ dividend-growth rates over the prior five years, but its more than 1% expense ratio and stock disappointments reduced the fund’s subsequent one-year yield to only 1.08% after fees and it averaged a 1.98% trailing 12-month yield over the five-year period ended September 2021. So, the fund’s 3.23% projected one-year pre-expense yield as of June 2021, then the highest among U.S. diversified equity funds in the Morningstar 500, is not a sure thing.

Dividend investors should instead focus on total return--income and capital gains--over multiple years. Whereas $100,000 in AMG River Road Dividend All Cap Value over the five-year period ended September 2021 paid $11,082 in total dividends on a principal base that grew to about $131,500 with capital gains reinvested, that sum in Vanguard 500 Index paid $12,612 in dividends and grew to more than $198,600, in part thanks to growth stocks’ tailwinds.

To generate more income than a broad equity benchmark like the S&P 500 may require sacrificing some total return. Vanguard Equity-Income VEIRX grew an initial $100,000 investment to only about $151,980 over the five years through September 2021, but it paid $17,091 in dividends, or about a third more than Vanguard 500 Index.

Investors who hold their money outside tax-advantaged accounts should pay heed to tax efficiency. Vanguard Equity-Income distributed more than $12,560 and $325 in long- and short-term capital gains, respectively, on an initial $100,000 investment over the five years ended September 2021. By contrast, Vanguard 500 Index didn’t generate any, and neither did Vanguard High Dividend Yield ETF VYM, which paid $18,881 in dividends and grew its principal to nearly $143,230.

Investors who resist the temptation to chase yield and instead consider funds’ income generation and total return potential, as well as fees and taxes, increase their odds for success.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OPA4TZMXZJDRLG5DYE2W6YTE7A.jpg)

/d10o6nnig0wrdw.cloudfront.net/05-08-2024/t_f17f0449d3314a27b966dcee5d39a6cb_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LUIUEVKYO2PKAIBSSAUSBVZXHI.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/08b315db-4874-427f-b3b1-f2b84a16e609.jpg)