Lessons From a Multibillion-Dollar Fund Scandal

Allianz Global Investors’ fraud: The crime, the punishment, and the effects have lots to teach investors.

/s3.amazonaws.com/arc-authors/morningstar/08b315db-4874-427f-b3b1-f2b84a16e609.jpg)

Warren Buffett’s famous quip, “you only find out who is swimming naked when the tide goes out,” applies to large global asset managers, whose fortunes fade after the receding waters reveal not just ill-advised behavior but outright malfeasance. (See, for example, Buffett’s chairman’s letter in the 2001 Berkshire Hathaway annual report, where he applies the quip to the reinsurance business.) That happened to several shops in the wake of the early 2000s market-timing scandals, and it happened again in mid-2022 to the U.S. subsidiary of Allianz Global Investors, while affecting investors in the strategies it ran for other firms, including more than a dozen Virtus Investment Partners mutual funds.

The crime, the punishment, and its effects reinforce the importance of knowing what you own and what managers are doing. After allowing some time for the dust to settle and to assess all the changes, we detail here what happened and which funds were affected, and draw out several lessons for investors.

Crime and Punishment

AllianzGI’s now-defunct Structured Alpha funds were the source of the problem. These 17 institutional-oriented strategies had gathered up to $14 billion in assets under management by profiting from buying and selling options on indexes like the S&P 500, using the funds’ own debt and equity holdings as collateral. Put option combinations giving the right to sell were supposed to protect the funds against a sudden market crash, at least in the short term. But in their absence the lineup’s most-aggressive strategies lost more than 90% in March 2020′s coronavirus-driven volatility while the tamer versions dropped about 35%. AllianzGI liquidated the lineup’s worst performers immediately, others at the end of that year, and the rest in 2021.

The problem wasn’t just the losses, but the lying that preceded them. The disastrous early 2020 performance revealed that there was much less hedging in place than what had been communicated, and that the managers had understated the funds’ risk. AllianzGI later admitted to defrauding investors for at least the six previous years, and three of its former employees were charged with breaching the strategies’ capacity limits, manipulating stress tests, and smoothing returns. As a result, in May the SEC fined AllianzGI’s U.S. subsidiary $1 billion, ordered it to pay more than $5 billion in restitution, and banned it from managing U.S. registered investment funds for 10 years.

Effects

AllianzGI’s forced exit left Virtus Investment Partners scrambling as an advisor. It had to find a new subadvisor for its 18 U.S. mutual funds that AllianzGI ran. Unlike the Structured Alpha strategies, they were more-traditional strategies for everyday retail investors.

A strategic partnership between AllianzGI and Voya Investment Management initially seemed like a major step forward. The plan was to transfer billions of AllianzGI U.S. assets and selected investment teams to Voya, with AllianzGI taking a stake in Voya as a part of the deal. Virtus’ board would need to review and approve all new management contracts in line with its fiduciary duty, but the expectation was that most of the funds moving to Voya would keep their teams, providing continuity for investors.

That plan only partially materialized, however. By late July, just two funds had changed hands as anticipated, in each case keeping their prior Morningstar Analyst Rating. Five other rated funds received new management teams either in whole or in part because Virtus tapped affiliates with whom it had a prior relationship. The 11 nonrated strategies suffered a mix of fates, which included three liquidations. The accompanying exhibit summarizes the changes and their impact to the 15 funds that remain, with updated Morningstar Analyst Ratings for the seven still under coverage.

Fraud Destroys

Fraud destroys, and it can take years to recover. Entering 2022, AllianzGI had $163.4 billion in U.S. discretionary AUM. As of July 25, however, Voya had acquired more than $100 billion of those assets in return for AllianzGI taking a 24% stake in Voya’s business.

That stake will help ameliorate the loss of those assets, but the reputational and financial harm to AllianzGI’s U.S. business has been significant. Even if the misdeeds prove isolated as AllianzGI has claimed, history suggests it could be hard for the U.S. subsidiary to regain its former status.

Putnam was a top-five firm in March 2000 with nearly $280 billion of assets in its mutual fund business. Then came the 2000-02 bear market and later revelation that from 1998 to 2003 some Putnam money managers repeatedly late-traded their own international funds when the U.S. market rallied in anticipation of overseas markets following suit; other Putnam employees let institutional players trade late. Both actions skimmed profits from long-term investors. The scandal and its aftermath caused Putnam’s fortunes and ranking to plummet. As of September 2022, Putnam’s $70 billion in assets ranked outside the industry’s top 40.

True, some firms embroiled in the early 2000s market-timing scandal, such as MFS and Pimco, have recovered and now serve investors well. Still, others, such as Strong Capital Management and PBHG, have disappeared.

Conflicts of Interest Should Be Minimized

Conflicts of interest, though pervasive and persistent in the fund industry, should be minimized as much as possible.

Extremely profitable strategies are unfortunately less prone to draw scrutiny. AllianzGI netted more than $400 million from the Structured Alpha funds between 2016 and 2020, at a profit margin exceeding 70%. That made it less likely that the firm would have intervened with such a cash cow. Meanwhile, a higher revenue share as returns approached or exceeded targets incentivized the managers to take more risk than advertised. In 2019, for example, the Structured Alpha funds’ lead manager Gregoire Tournant had a $300,000 base salary but received $13.4 million in bonus compensation.

The best firms pay managers based on long-term investment results, not AUM. They also ensure managers do not take undue risks to amplify their bonuses. One prominent shop, for instance, after a certain point flattens out its bond managers’ bonuses for benchmark- and peer-beating returns so that they aren’t encouraged to take imprudent risks in any given year.

Due Diligence Is Crucial

Due diligence is crucial for fund companies as well as investors. That’s true for any strategy but especially for those that are supposed to generate good investment results when markets crash, since they are often quite complex.

AllianzGI’s due-diligence efforts on the Structured Alpha funds fell short, and it is at fault for the criminal misconduct of its now former employees. Virtus had no part in the fraud, and it rightly retained some management teams of the funds affected by AllianzGI’s ban while changing others.

Still, there were prior signs in at least one instance that Virtus’ oversight efforts left something to be desired. Virtus Global Allocation (formerly Virtus AllianzGI Global Allocation) PALLX imported its process from Europe in 2016, transitioned to a sustainable focus in 2019, and lost several managers from 2020 to 2021.

Neither has Virtus distinguished itself through subsequent changes to Global Allocation. Although Virtus was able to bring Global Allocation’s lead manager Heather Bergman in-house, she has lost access to key personnel amid increased duties, and now oversees a fund with two subadvisor teams whose expertise does not match their role. The value shop NFJ runs a sustainable mandate behind 30% of the fund’s targeted equity weighting but has no record running such strategies. Similarly, it’s questionable that emerging-markets debt specialist Stone Harbor has the kind of core bond capabilities that the fund needs.

Morningstar Can Help

Morningstar’s Parent work and fund coverage can help investors stay on top of changes to strategies they hold, as we’ve done here. It can also help them make good choices and set realistic expectations while ideally pointing them to the best options from the start.

Morningstar isn’t perfect, however. Nor are we immune to fraud. Our ratings on AllianzGI’s Structured Alpha funds were wrong in large part because we received the same doctored information others did, including a discussion of risk-management practices that led us in February 2020 to upgrade the strategy’s Process to Above Average from Average. That upgrade, combined with the team’s Above Average People rating, had resulted in a Morningstar Analyst Rating of Bronze for its cheapest share classes. Our missed call notwithstanding, in the immediate aftermath of the funds’ early 2020 catastrophic losses Morningstar placed the strategy Under Review in late March of that year and downgraded it to Negative in April.

After the SEC charged AllianzGI with fraud in 2022, Morningstar downgraded its Parent rating to Below Average from Average. AllianzGI, though, did not previously have an Above Average Parent rating, much less a High one.

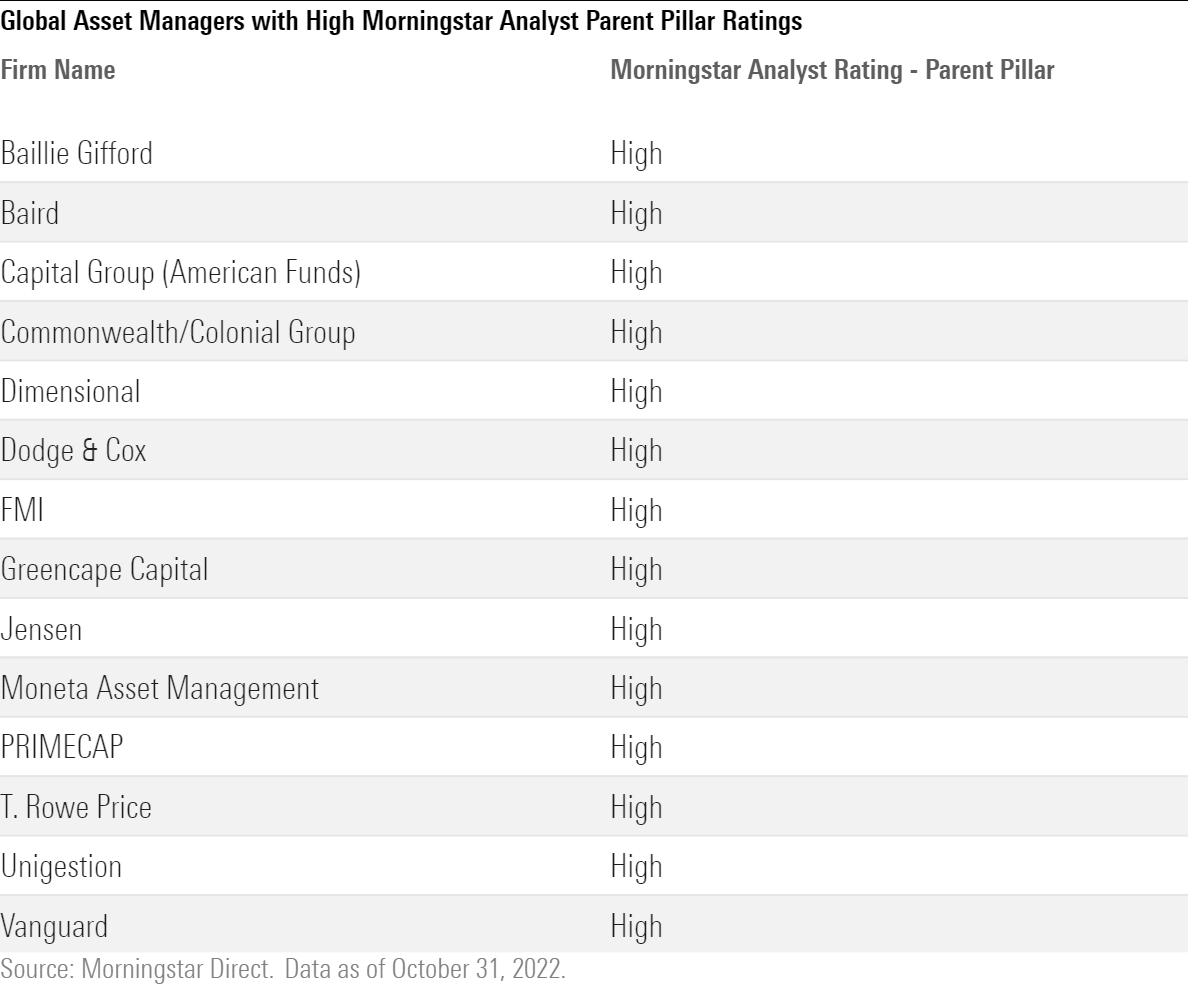

Morningstar reserves the High rating for top-tier firms that repeatedly prove themselves worthy of trust in their approach to hiring and monitoring talent, whether internal or external, so they can address problems before they multiply, not afterward. Selecting and keeping tabs on the right asset manager is a lot to ask of most investors. But Morningstar in its Parent ratings and fund coverage aims to help them do just that.

Ultimately, the goal is to point investors toward firms and strategies that will enable them to be as prepared as possible for when Buffett’s proverbial tide goes out.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/08b315db-4874-427f-b3b1-f2b84a16e609.jpg)