4 min read

What’s Behind the Rise of Direct-Sold 529 Plans?

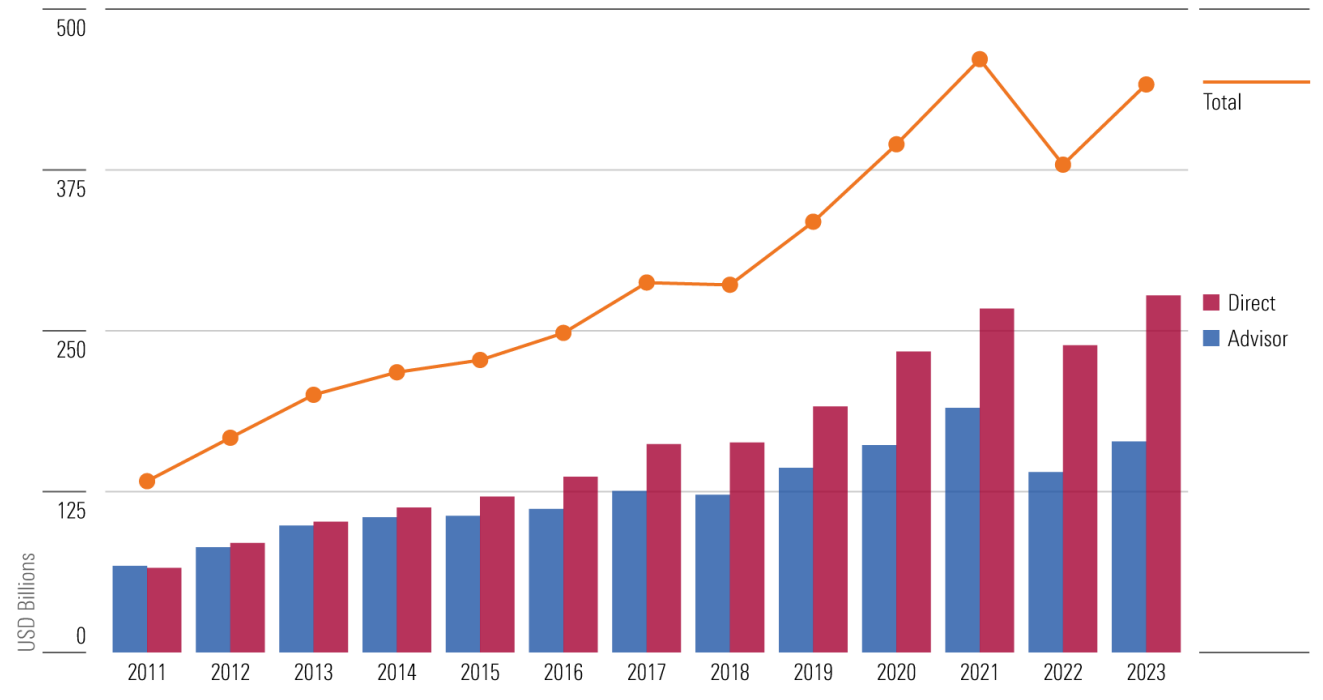

Morningstar research shows that fee-based advisors are increasingly favoring cheaper direct-sold 529 plans.

As families grapple with the rising costs of college, they’re increasingly turning to 529 college savings plans to help fund their children’s education.

That movement pushed the 529 market to an all-time high in December 2019, when assets approached $328 billion before the coronavirus sell-off caused it to fall to around $293 billion as of March 31, 2020.

Assets in 529 plans by distribution channel. Source: Morningstar Direct, surveyed data. Data as of Dec. 31, 2023.

Concurrently, there has been a long-term shift away from solely commission-based advisory businesses and toward fee-based compensation.

One key reason for the trend toward direct-sold plans is that advisors who have a fee-based business model have greater flexibility to choose the best plan available for their clients, regardless of the distribution channel. As a result, cheaper, direct-sold 529 plans have become increasingly popular with these cost-conscious fee-only financial advisors.

Direct-sold plans continue to hold the lion’s share of 529 assets, but advisor-sold plans edged ahead in recent growth. On average, Morningstar's 529 College Savings Plan Landscape report showed that direct-sold plans grew by 16% in 2023, while advisor-sold plans (mostly offered by commission-based advisors) grew by 17% over the same period.

Here, we take a closer look at how advisor-sold and direct-sold 529 plans have evolved in that time.

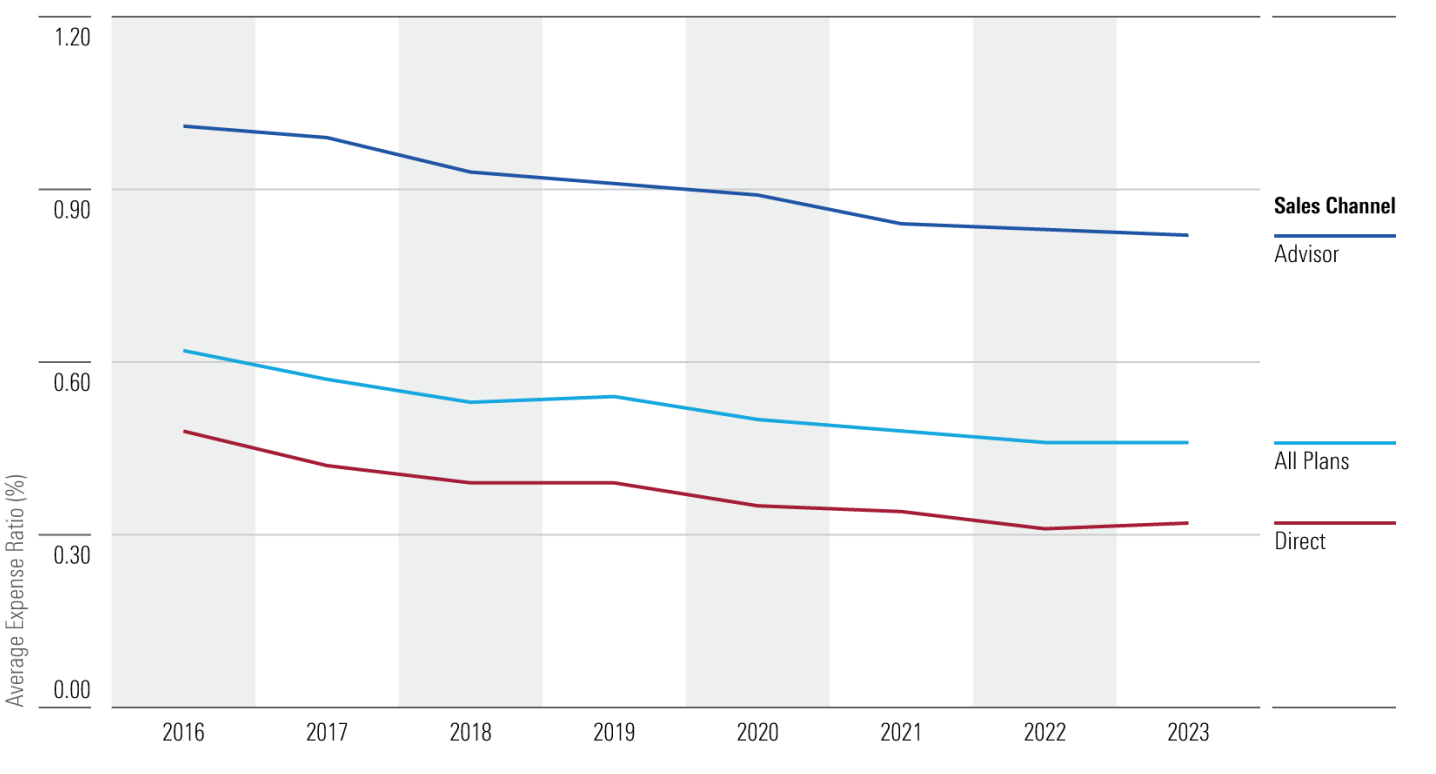

Why Are Fees for Direct-Sold 529 Plans so Much Lower?

Even as overall assets in 529 plans have grown, there’s still a wide gap between fees charged for direct-sold and advisor-sold plans.

For an age-based portfolio—the most popular investment option for college savers—the average fee in direct-sold 529 plans was 0.32% at the end of 2019, compared with 0.82% in advisor-sold plans.

There are a couple of reasons for this fee gap:

- Plans sold through an advisor cater specifically to financial advisors who receive commissions based on the funds in which their clients invest. These commissions tend to drive fees higher in advisor-sold plans’ age-based portfolios, regardless of the type of underlying funds the portfolios use.

- There are differences in the types of funds typically found in advisor-sold versus direct-sold age-based portfolios. The teams behind advisor-sold plans tend to favor actively managed funds—which charge higher prices—while direct-sold, age-based options heavily favor low-cost index funds.

The industry saw many plans switch to cheaper (often passive) underlying funds in recent years, which left fewer plans to make the same move in 2023. Still, plans with a growing and relatively larger asset base can achieve economies of scale through reduction in asset-based fees or administrative fees.

Chart showing average expense ratio over time. Source: Morningstar Direct. Data as of Dec. 31, 2023.

How We’re Rating 529 Direct-Sold vs. Advisor-Sold Plans Amid Evolving Lineups

There are valid reasons why investors choose advisor-sold 529 plans, such as when the state’s advisorsold plan is better managed than its direct-sold plan, or if the investor seeks more actively managed funds, which advisor-sold plans tend to hold more of. However, investors should note that exposure to expensive funds and the additional distribution fees lead to higher overall costs. In our ratings methodology, plans with low fees relative to peers are more attractive, as the hurdle to generating strong performance is reliably lower than more expensive peers.

Morningstar currently rates 54 education savings plans, representing 94% of the assets in the industry. Of those 54, two plans, Utah’s my529 plan and Pennsylvania’s 529 Investment Plan, receive our top Morningstar Medalist Rating of Gold, reflecting our highest confidence in their ability to provide participants with compelling investment results.

Morningstar’s Medalist Rating for 529 plans considers four pillars:- People

- Process

- Parent

- Price

For each pillar, we look for what we believe are best-in-class industry practices, including:

- Skilled teams with experience managing multi-asset strategies and curating investment menus

- A well-researched approach for target enrollment and age-based options

- A robust process for selecting investments

- The state agency’s ability to provide thoughtful oversight and stewardship

- Low fees for age-based or target-enrollment options

Read more in Morningstar’s latest 529 College Savings Plan Landscape research report.

Important Disclosures

The information, data, analyses, and opinions presented herein do not constitute investment advice; are provided solely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete, or accurate.

The opinions expressed are as of the date written and are subject to change without notice. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses, or opinions or their use. The information contained herein is the proprietary property of Morningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar.

Investment research is produced and issued by subsidiaries of Morningstar, Inc.