2.5 min read

Clean Shares: What You Need to Know

Morningstar proposes a more meaningful way of categorizing share classes.

Clean shares were created to reduce conflicts of interest by eliminating, or at least leveling, payments from asset managers to the intermediaries that sell mutual funds. Intermediaries would then ensure their advisors’ compensations did not depend on the fund they recommended, reducing conflicts of interest.

While the idea of clean shares is good for investors, we have a few concerns with how they’re being presented.

Here's what investors and financial advisors need to consider for three types of clean shares.

What Does “Clean Shares” Really Mean?

Our concerns with the umbrella term “clean shares” include:

- It implies that anything called “clean” is the best choice, which is not necessarily the case. As there are actually several different flavors of new share classes, we believe more descriptive names and categories would help mutual fund investors understand the answers to a few key questions related to this difference. For instance, who are they paying directly and indirectly for services? What conflicts of interest might any indirect payments create?

- Though there is universal agreement that clean shares will not have loads or 12b-1 fees—both fees used to pay for a mutual fund’s distribution costs—there are still different service-fee arrangements among share classes that currently fall under the “clean” umbrella.

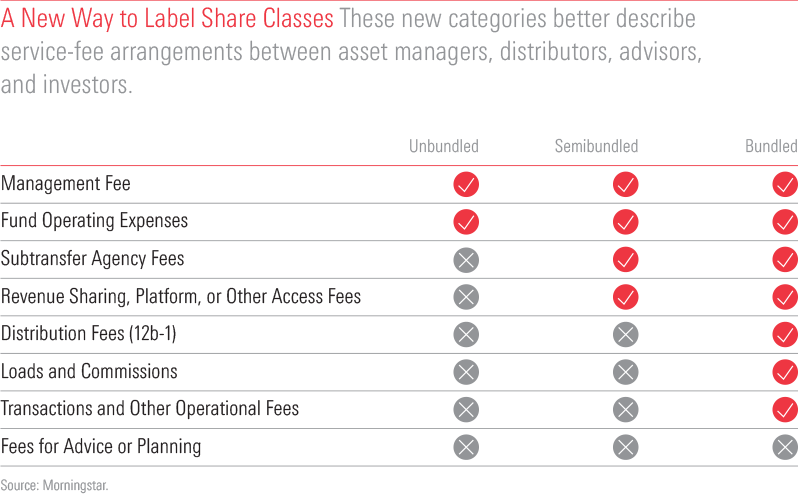

3 Ways to Categorize Share Classes

To help investors and the industry untangle what these new share classes mean, Morningstar is labeling emerging share classes a little differently.

We aim to shed light on what an investor pays for directly (say, by writing a check to an advisor) or indirectly (via a fund’s expense ratio). As the chart below shows, we categorize the classes as unbundled, semi-bundled, or bundled.

Here’s More About What That Means

- Unbundled: An investor simply pays for investment management and fund operating expenses, and the fund and its advisor do not pay third parties who sell their funds to the public. Unbundled share classes reduce conflicts, but investors still need to ask if they are paying a reasonable amount for advice and for the services that their intermediary charges them directly.

- Semibundled: No traditional distribution fees (or 12b-1 fees) or load-sharing but can have revenue sharing or sub-TA fees. Semibundled share classes could create some potential conflicts of interest that investors need to ask about.

- Bundled: Traditional share classes, where the investor pays a load and a 12b-1 to the mutual fund, which in turn pays the intermediary. Bundled share classes are purely transactional, which can work well for sophisticated investors who have done their homework and wish to pay up-front commissions. Advice associated with these share classes may ultimately cost less, particularly with rights of accumulation.

How Advisors and Asset Managers Can Use These Categories of Share Classes

One category isn't inherently better than the other; each of these service arrangements can be appropriate for different kinds of investors. Rather, investors and advisors should use them as starting points to have better-informed conversations.

Here’s how those groups may benefit from these categories:

- For advisors, it can be an opportunity to demonstrate how their particular service model benefits their clients. Bundled share classes, for example, may be in decline, but advice associated with these share classes may ultimately cost less for long-term investors.

- For asset managers, the unbundled category may give a clearer way to showcase their skill: Because unbundled share classes are stripped of all the servicing and compensation burdens that come with bundled and semi-bundled share classes, investors and advisors have a clearer view of a portfolio manager’s value-add.

Users of Morningstar Direct and Morningstar Direct Advisory Suite can see these new labels for all US funds at the share class level under “Clean Share—Service Fee Arrangement.”

This blog post is adapted from an article that originally appeared in the June/July 2018 issue of Morningstar magazine. Read the full article or subscribe for free.