The Worst-Performing Stocks of 2023

SolarEdge, Plug Power, Moderna, and Pfizer are among the year’s biggest losing stocks.

/s3.amazonaws.com/arc-authors/morningstar/11aca145-fc87-4ca5-9dbf-09f77ad3584c.png)

Overall, 2023 was a great year for stocks, as the markets rallied to near-record highs in late December. However, not all companies surged.

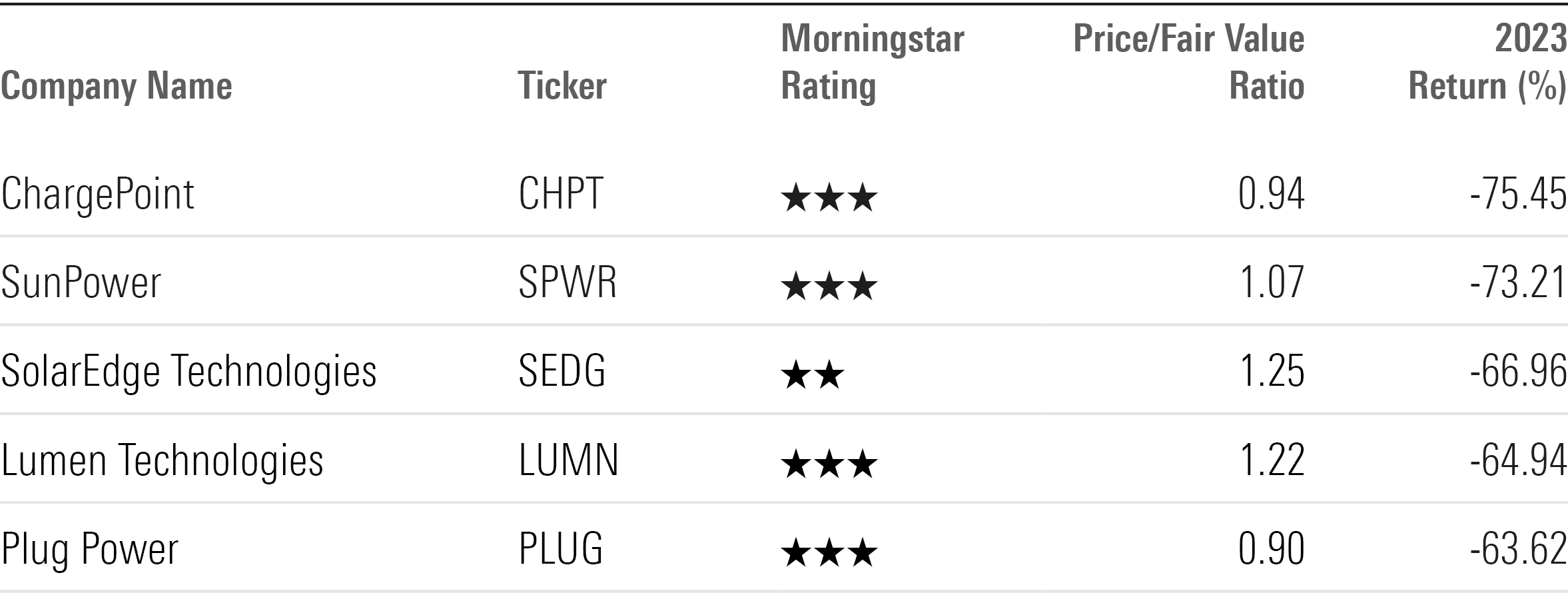

The year’s worst-performing name among the U.S.-listed firms covered by Morningstar analysts was ChargePoint CHPT, which fell 75.5%. Clean energy stocks were pummeled by high interest rates, supply chain issues, and decreased demand. Four of 2023′s five worst-performing stocks were in this industry. SunPower SPWR, SolarEdge Technologies SEDG, and Plug Power PLUG fell 73.2%, 67.0%, and 63.6%, respectively.

These were 2023′s worst-performing stocks under Morningstar’s U.S. coverage:

- ChargePoint

- SunPower

- SolarEdge Technologies

- Lumen Technologies LUMN

- Plug Power

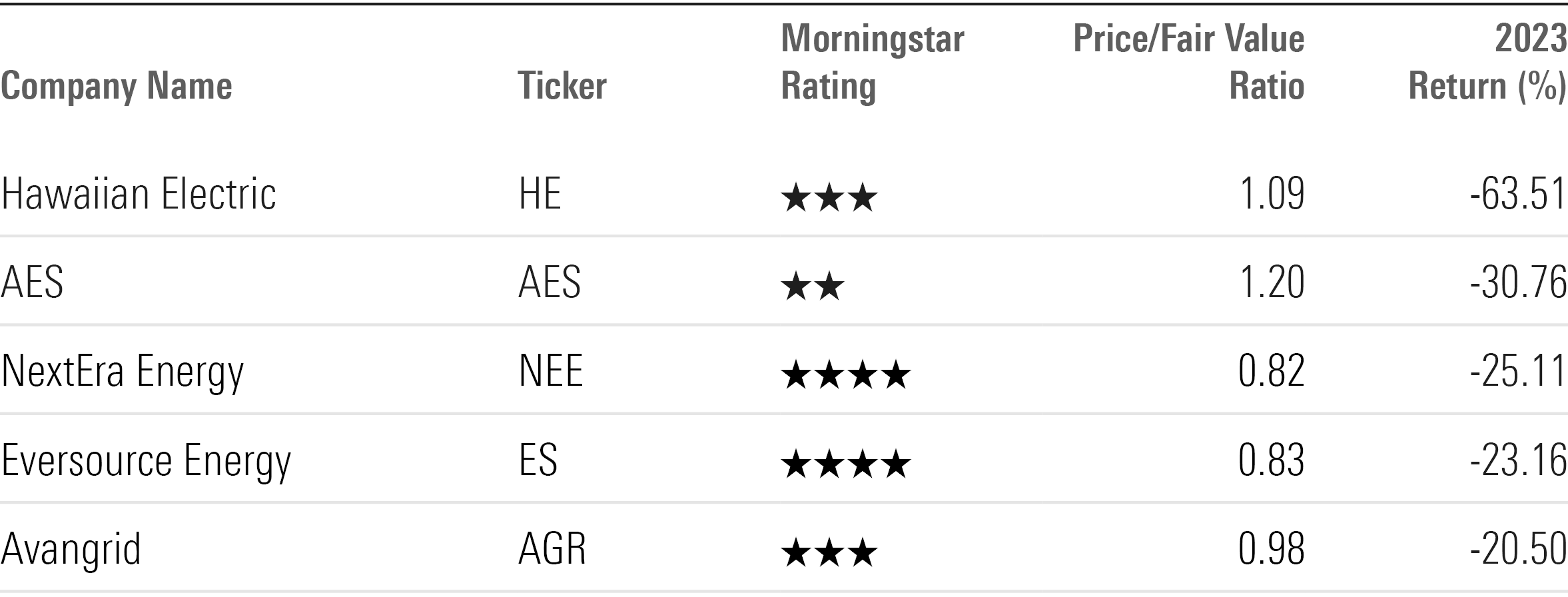

Overall, utilities posted the worst returns of any sector, with the Morningstar US Utilities Index dropping 7%. Many of these are clean energy companies, such as AES AES and NextEra Energy NEE, which fell 30.8% and 25.1%, respectively.

The worst-performing utility stock, Hawaiian Electric HE, faced additional headwinds over concerns around its potential liabilities related to the deadly Maui wildfires in August. Morningstar equity strategist Andrew Bischoff warned that “investors could experience material capital loss given the wide range of potential outcomes, which remain very uncertain and could change as the situation develops.”

Here’s a look at 2023′s worst-performing stocks, along with their key Morningstar metrics and selected commentary from our analysts. All data is as of Jan. 2, 2024.

2023′s Worst-Performing Stocks

Worst-Performing Stocks of 2023

ChargePoint

- Fair Value Estimate: $2.50

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: None

“We believe ChargePoint is well-positioned in the alternating current (level 2) charging market but enjoys fewer advantages in the direct current fast-charging segment. While rising electric vehicle penetration remains a long-term secular growth opportunity, we see more attractive opportunities for investors outside of our EV charging coverage.”

—Brett Castelli, equity analyst

SunPower

- Fair Value Estimate: $4.50

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: None

“SunPower has undergone several strategic changes in recent years to refocus on the U.S. residential solar market. In 2020, it completed the spinoff of Maxeon, its legacy solar module manufacturing business. In 2021, Peter Faricy replaced longtime CEO Tom Werner, who retired. Faricy promptly focused the company on U.S. residential by exiting the less profitable commercial segment and acquiring residential solar installer Blue Raven Solar.”

SolarEdge Technologies

- Fair Value Estimate: $75.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: None

“SolarEdge began commercial shipments in 2010 and has grown into the world’s leading inverter manufacturer based on revenue. The company’s DC optimizer is prevalent in rooftop applications, as it provides functionality not found in a string inverter, but at a lower price than microinverters. SolarEdge initially targeted the residential market but has expanded its product suite to the commercial market and more recently the utility-scale market. This strategy has expanded the company’s total addressable market, but average selling prices and gross margins typically deteriorate as project sizes increase.”

Lumen Technologies

- Fair Value Estimate: $1.50

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: None

“The attractiveness of Lumen’s enterprise business—which now makes up almost 80% of the firm’s total—is mixed. Lumen has a leading network that plays an integral role in making up the backbone of the internet and transporting data around the world. While it is not the leader in optical fiber holdings or enterprise communications services, the growing importance of our connected world gives us confidence that Lumen’s network will remain vital. On the other hand, the company faces overcapacity, multiple competitors, and technological advances that lead to deflationary pricing and cannibalization of big legacy revenue streams. We don’t anticipate the firm’s total enterprise revenue will return to growth for the foreseeable future, as customers will continue to benefit from the ability to use shared, rather than private, networks and require less bandwidth to meet growing needs.”

—Matthew Dolgin, equity analyst

Plug Power

- Fair Value Estimate: $5.00

- Morningstar Rating: 3 tars

- Morningstar Economic Moat Rating: None

“Green hydrogen is in its infancy as a fuel to decarbonize. Customers face numerous challenges with adopting hydrogen technology, including economics and a lack of production and infrastructure. Within this context, we view Plug’s efforts to provide customers with a one-stop-shop solution of technology and fuel as a way to lower the barriers to customer adoption. While this strategy brings greater capital intensity, it positions Plug as the only all-in-one provider within the industry.”

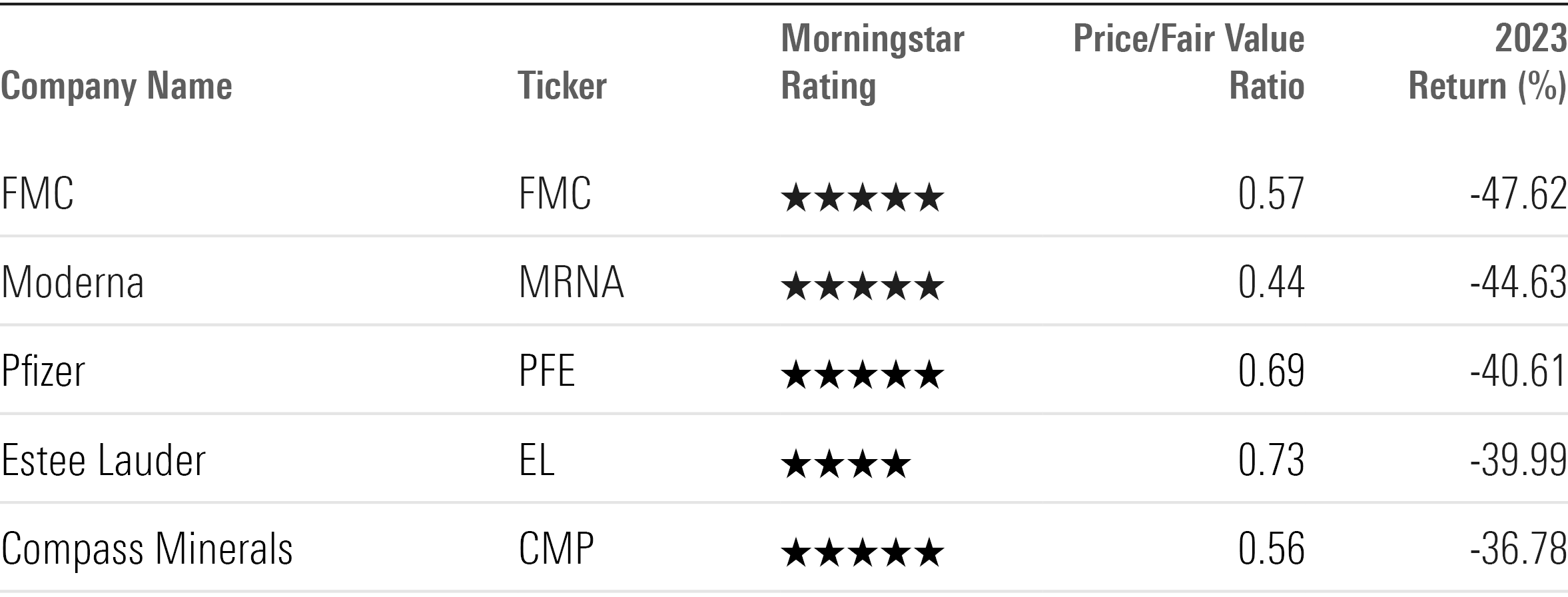

Worst-Performing Undervalued Stocks

Worst-Performing Undervalued Stocks

FMC

- Fair Value Estimate: $110.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Narrow

“We view FMC FMC shares as materially undervalued, with the stock trading at roughly 50% of our fair value estimate. We think the market is overly focused on the near-term decline in FMC’s profits due to industrywide inventory destocking. In our view, inventory destocking has affected all the company’s premium product peers, when isolating crop protection products and accounting for differing geographical exposure. Further, we think the market gives FMC virtually no credit for its pipeline, while also assuming FMC’s diamide portfolio faces a patent cliff, leading to lower long-term profits. Accordingly, we see a strong margin of safety in the current share price, with much of the bad news already priced in.”

—Seth Goldstein, strategist

Moderna

- Fair Value Estimate: $227.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: None

“In a record-breaking span of just 11 months, Moderna MRNA created, developed, manufactured, and got regulatory authorization for mRNA-1273, a two-dose COVID-19 vaccine that is one of the first two mRNA vaccines ever authorized (alongside Pfizer/BioNTech’s BNT162b2). The pandemic accelerated Moderna’s evolution into a commercial-stage biotech, and we expect that the firm’s ramp-up in manufacturing and clinical know-how will pave the way for faster timelines for additional programs. Moderna’s mRNA platform, involving rapid design and similar manufacturing across programs, allows the company to pursue multiple programs in parallel. Moderna also retains full rights to most of its programs, although partnerships with Merck and Vertex help support its efforts in oncology and cystic fibrosis.”

—Karen Andersen, strategist

Pfizer

- Fair Value Estimate: $42.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Wide

“Pfizer’s PFE size establishes one of the largest economies of scale in the pharmaceutical industry. In a business where drug development needs a lot of shots on goal to be successful, Pfizer has the financial resources and established research power to support the development of more new drugs. Also, after many years of struggling to bring out important new drugs, Pfizer is now launching several potential blockbusters in cancer and immunology.”

—Damien Conover, director

Estee Lauder

- Fair Value Estimate: $200.00

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Wide

“We see Estee EL as poised to benefit from premiumization trends, as beauty consumers in developed and emerging markets alike upgrade for perceived better-quality ingredients, efficacy, and service. Outside North America, we view Estee as particularly well-positioned in Asia (where skincare makes up 50% of premium beauty spending), thanks to highly regarded skincare brands (La Mer and Estee Lauder), as well as a newly opened innovation center and factory in the region that should enable it to deliver locally relevant products in a timely fashion. Further, we think its strategy to extend its brand reach is strong, given only half of Estee’s 20-plus brands are currently available in China, India, and Brazil. In addition, we expect Estee to dial up investments in digital channels and travel retail to complement its strong ties with brick-and-mortar retailers, keeping Estee’s brands top of mind for consumers and ensuring its products are easily accessible as beauty users shop across channels.”

—Dan Su, equity analyst

Compass Minerals

- Fair Value Estimate: $45.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Wide

“Compass Minerals CMP has an enviable portfolio of cost-advantaged assets. Its Goderich rock salt mine in Ontario benefits from unique geology, and with access to a deepwater port, it can deliver deicing salt to customers at a lower cost than competitors. Additionally, the company controls one of only three naturally occurring brine sources that produce the specialty fertilizer sulfate of potash. These operations at the Great Salt Lake in Utah can produce SOP at a lower cost than marginal-cost producers that convert standard potash.”

Worst-Performing Moat Stocks

Worst-Performing Moat Stocks

Hawaiian Electric

- Fair Value Estimate: $13.00

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: Narrow

“Shareholders will need to be comfortable with a wide range of outcomes due to potentially significant liabilities from recent wildfires in Maui. The largest fire in Lahaina killed more than 100 people and destroyed 2,200 structures with an estimated cost of $5.5 billion, according to a damage report released in mid-August by the Pacific Disaster Center and the Federal Emergency Management Agency. Plaintiffs will need to show that the utility was negligent or could have reasonably prevented a loss.”

—Andrew Bischof, strategist

Dollar General

- Fair Value Estimate: $141.00

- Morningstar Rating: 3 Stars

- Morningstar Economic Moat Rating: Narrow

“Dollar General’s DG over 19,000 small-box locations make the retailer an omnipresent force in rural communities that lack national retail chains. The firm provides low-income households (a typical Dollar General customer earns around $40,000 per year) with a convenient fill-in shopping destination and reasonable price points on merchandise, which we view as the crux of its value proposition. Since thinly populated and less affluent towns cannot economically support an abundance of retailers, Dollar General thrives by leaning into areas with minimal competition. Furthermore, its impressive scale and proximity to consumers, product mix that is 80% consumables, and small basket size (usually around $15) help insulate the retailer from e-commerce competition.”

—Noah Rohr, equity analyst

Worst-Performing Utilities Stocks

Worst-Performing Utilities Stocks

AES

- Fair Value Estimate: $16.00

- Morningstar Rating: 2 Stars

- Morningstar Economic Moat Rating: None

“CEO Andres Gluski has narrowed AES’ geographic and business focus by selling businesses in markets where the company did not have a strong platform or competitive advantage. We think his strategy has been in the best interest of shareholders. The company now has operations in fewer countries, a stronger balance sheet, and a rapidly growing renewable energy business. Management expects earnings to grow 7%-9% annually through 2025. We expect AES to achieve this. Growth should be supported by continued development of the company’s renewable energy backlog and growth at the company’s regulated utilities.”

NextEra Energy

- Fair Value Estimate: $74.00

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: Narrow

“We believe the market has lost confidence in management’s ability to hit its growth targets since the recent announcement that its partially owned NextEra Energy Partners subsidiary is cutting growth expectations. Additionally, we think the continued concerns about the regulatory environment in Florida will persist until the company works through its upcoming rate case, which will determine rates effective January 2026.”

Eversource Energy

- Fair Value Estimate: $74.00

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: None

“Eversource ES has grown into one of the largest utilities in the U.S. Northeast after its 2012 merger with NStar, 2017 acquisition of Aquarion, and 2020 acquisition of Columbia Gas. This can make it a prime target for politicians and customers who pay high energy prices in the region. The region’s clean energy goals create ample opportunities for the company over the next decade to integrate renewable energy, energy efficiency, and electric vehicles. However, some regulators in the region have been stingy due to high customer rates, limiting the upside for shareholders.”

—Travis Miller, strategist

Avangrid

- Fair Value Estimate: $33.00

- Morningstar Rating: 3 Stars

- Morningstar Economic Moat Rating: Narrow

“Avangrid AGR is majority-owned by European utility Iberdrola. Investors must be comfortable with regulated operations across the Northeast and the outlook for the U.S. onshore and offshore renewable energy growth. Avangrid’s regulated utility segment, Networks, operates eight regulated electric and natural gas utilities across New York, Maine, Connecticut, and Massachusetts. We consider the utilities’ regulatory jurisdictions as mostly constructive. Most of its subsidiaries’ rates are tied to multiyear agreements or formula rates and decoupled from usage. However, Avangrid has struggled to earn its allowed returns.”

Correction: (Jan. 12, 2024): A previous version of this article misspelled the last name of Morningstar healthcare strategist Karen Andersen.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/11aca145-fc87-4ca5-9dbf-09f77ad3584c.png)