What Are the FAANG Stocks Really Worth?

We’ve recently updated our fair value estimates on four of the five names.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

Campaigning and voting are over. Ballots have been mailed in, dropped off, or cast in person. No more rallies (drive-in or otherwise), celebrity endorsements, or prerecorded phone calls from candidates.

For some, following the U.S. election has been a near full-time habit--but it isn’t the only thing we’ve been thinking about here at Morningstar. Earnings season has kept us plenty busy, too.

That might surprise some. After all, longtime readers know Morningstar doesn’t give quarterly earnings reports and short-term guidance too much weight. Rather, we focus on a company's long-term sustainable competitive advantages, encapsulated in our Morningstar Economic Moat Ratings. We expect companies with moats to deliver superior returns over time. Short-term earnings surprises or disappointments are no more than blips in the long-term picture.

That being said, a company might release information when reporting that influences our fair value estimate of its stock.

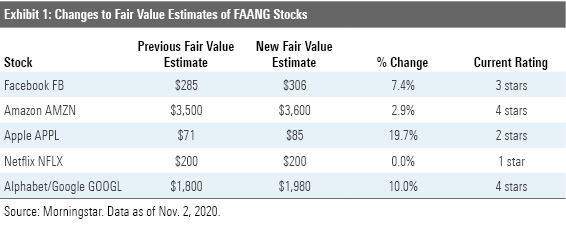

In fact, we’ve boosted our fair value estimates on four of the five FAANG stocks during the past couple of weeks as a result of new information that surfaced in their earnings reports and/or calls.

However, a fair value boost isn't a buy signal. A stock is only a "buy" from our perspective if it's trading well below our fair value estimate, after being adjusted for uncertainty. (For more about how we determine our fair value estimates, watch this explainer video.)

Here’s a sampling of our thoughts about the latest earnings reports from Facebook FB, Amazon AMZN, Apple AAPL, Netflix NFLX, and Alphabet GOOGL, along with the fair value change where appropriate. (Read more about what our analysts think about other high-profile earning reports this quarter.) Interestingly, two of the five stocks are undervalued according to our metrics as of this writing.

Facebook "Facebook reported better-than-expected third-quarter results but provided a cautionary outlook for 2021. The firm is concerned that demand for direct response ads may weaken a bit during a recovery after an unexpected spike during the coronavirus pandemic. Additionally, Facebook management reiterated that changes to Apple's identifier for advertisers could create headwinds. However, we believe management is being overly cautious, as an economic expansion will likely be accompanied by the startup of small businesses, which will mainly use direct response advertising. In our view, the pandemic and resulting e-commerce growth has increased the stickiness of Facebook, as smaller businesses have become more dependent on the platform for advertising and various tools (such as Facebook Shop and Business Suite) that the firm provides to help with digital transformation.

An economic recovery should also prompt a rebound in demand among brand advertisers. Finally, while Apple’s move may lower ad ROIs, we believe advertisers will have little choice but to use the platform given its large audience. We increased our 2020 and 2021 revenue projections, increasing our fair value estimate to $306 (from $285). We view this wide-moat stock as fairly valued.

Facebook posted total revenue of $21.5 billion, up 22% year over year driven by growth in users and user monetization. The firm's monthly active user count increased in all markets, reaching more than 2.7 billion users globally, up 12% from 2019. With similar growth in daily active users, overall engagement on the platform remained at about 66%. More users and more time spent on the platform continue to attract advertisers, mainly small and medium-size businesses, or SMBs, which further improved Facebook's user monetization as average monthly revenue per user increased 9% from 2019 to $7.89. With more users and higher engagement, ad supply increased 35% from last year, with only a limited impact on prices, which declined 9%." Ali Mogharabi, senior analyst

Amazon "Posting another quarter of exceptional growth (revenue of $96.2 billion, up 37.4%, versus guidance of $87-$93 billion) and profitability (operating profit of $6.2 billion, representing operating margins of 6.4%--10.0% excluding $3.5 billion in COVID-19-related expenses--versus guidance of $2 billion-$5 billion), the natural question investors might be asking is how much of wide-moat Amazon's recent momentum is tied to pandemic demand and how much reflects structural changes? While certain trends are unlikely to repeat--pantry stuffing and fulfillment centers running at elevated capacity, for instance--many changes in consumer behavior are likely to sustain, giving us confidence in our five-year targets calling for 22% top-line CAGR and 10% operating margins.

Our conviction comes from several service-related sources. One, Prime member engagement remains high, with Prime member renewal rates improving year over year and subscription revenue per Prime member increasing roughly 10% according to our estimates. Two, third-party seller services revenue also accelerated (55% from 52% last quarter), which not only indicates Amazon's importance as a distribution channel, but that sellers are increasingly using services like Fulfillment by Amazon (FBA). Three, as advertising budgets rebound from COVID-19 lows, we expect Amazon will become an increasingly important partner both on and off Amazon marketplaces. Four, while demand remains mixed among some customers in discretionary categories, AWS margins (up 530 basis points to 30.5%) reinforces our views existing AWS users are graduating to more value-add services. Lastly, while the firm noted international profitability is "running ahead of schedule" because of fulfillment capacity usage, we still see a path to mid-single-digit operating margins for many markets outside the U.S.

We're planning to raise our $3,500 fair value estimate by a few percentage points to account for this quarter's upside and see shares as modestly undervalued." R.J. Hottovy, sector strategist

Apple "Apple reported fiscal fourth-quarter results ahead of our expectations led by Mac and iPad segments. The firm did not provide guidance the last two quarters and again refrained from offering specific guidance due to uncertainty regarding COVID-19. CEO Tim Cook expects iPhone revenue to grow in the December quarter despite the new iPhone 12 being launched a couple of weeks later in the quarter, though he did not specify the magnitude of growth. Meanwhile, all other products and services are expected to grow in the double digits.

We are raising our fair value estimate for narrow-moat Apple to $85 per share from $71 as we incorporate a stronger near-term outlook for the Mac and iPad segments due to ongoing work- and learning-from-home dynamics. Nonetheless, we think shares are currently overvalued, as we think recent growth trends could be unsustainable as we enter 2021.

Fourth-quarter revenue was up 1% year over year thanks to growth in iPad (46%), Mac (29%), services (16%), and wearables, home, and accessories (21%). Management noted the iPad and Mac segments remained supply constrained, which bodes well for these business lines in the December quarter. Apple’s iPhone sales were understandably down 21% year over year due to the iPhone 12 delay. Apple now has over 585 million paid subscribers to its various services, up 135 million from a year ago, and the firm expects 600 million subs by December 2020. Although Greater China was the region most impacted by the absence of the new iPhones for the quarter (total revenue down 29% year over year), non-iPhone sales grew double digits. Gross margin of 38.2% was up 20 basis points sequentially due to a higher mix of services.

Management was optimistic revenue from Greater China would grow in the first quarter, particularly as 5G is more mature in the region. We anticipate iPhone revenue for fiscal 2021 will be up in the low teens, though the late launch may shift some sales from the December quarter to the March quarter." Abhinav Davuluri, sector strategist

Netflix "Netflix raised prices on its two most popular plans in the U.S. on Oct. 30 as the firm looks for ways to grow revenue in the face of slowing subscription growth in its single biggest market. The price of the firm's standard plan will increase by $1, to $14 per month, and the premium plan will rise by $2, to $18 per month. The firm decided to not increase the price on its cheapest plan at $8 per month. The increase is the fifth for the standard plan, which debuted in November 2010 at $8 per month. While Netflix waited for three and a half years to enact its first price hike on the standard plan, this increase is the third in just three years. The increases in the United States and other developed markets will help offset the impact of lower-price plans in newer, emerging economies like India and Indonesia. We have slightly increased our estimate for 2021 monthly average revenue per user in the U.S. region as we previously expected a price hike later in 2021 and expected a uniform $1 increase. However, we are maintaining our $200 fair value estimate for Netflix, as our long-term pricing assumptions remain intact, based on the multitude of streaming options that have emerged in the U.S. market.

While Netflix did post strong U.S. subscriber growth in the first half of 2020 as the pandemic set in, growth slowed significantly in the third quarter, and we expect slower-than-usual growth in the fourth quarter as well. As we've noted before, Netflix has only one real source of revenue (streaming subscriptions) with only two levers to increase revenue: subscribers and price. Given the high penetration in the U.S. and high customer awareness, gaining the marginal subscriber is getting tougher, particularly as the streaming competition increases in number and quality. As a result, price increases may be the only real lever left to grow revenue in the U.S., and we expect that further increases may cause churn to spike up sharply." Neil Macker, senior analyst

Alphabet (Google) "While Alphabet is battling the Department of Justice and U.S. and international lawmakers on antitrust, Section 230, and other regulations, it continues to impress financially. The firm reported another strong quarter, with growth in all areas driving top- and bottom-line results above our projections and the FactSet consensus estimates. With the better-than-expected third-quarter results and increasing confidence in digital ad demand, we have increased our projections, resulting in a $1,980 fair value estimate, up from $1,800.

Alphabet’s Google benefited from increases in brand and direct-response digital ad spending as search and YouTube ad revenue grew during the quarter. In addition, the firm’s cloud segment continued its strong double-digit growth. As the economy recovers, we expect digital ad spending to accelerate, from which Google will be one of the main beneficiaries. Google also remains well positioned to continue to grab its fair share of the fast-growing cloud market.

Alphabet’s total revenue increased 14% year over year to $46.2 billion, driven by growth in ad and other revenue (which includes the cloud business). Search ad revenue of $26.3 billion returned to year-over-year growth (6.5%) after the pandemic-driven decline in the second quarter. YouTube ad revenue increased 32% from last year (compared with only a 6% increase in the previous quarter) to $5 billion as the platform continued to attract direct-response advertisers. Increased demand from brand advertisers also contributed to growth.

Google's cloud revenue jumped 45% year over year to $3.4 billion, driven by the increasing demand for digital transformation. Adoption of Google Workspace continued to improve as the number of seats as well as average revenue per seat increased during the quarter." Ali Mogharabi, senior analyst

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)