We Forecast Global Electric Vehicle Sales to Quadruple by 2030

Top investing picks across the EV supply chain.

/s3.amazonaws.com/arc-authors/morningstar/ca8d2ce1-cd0f-433b-a52b-d163be882398.jpg)

Over the past couple years, battery electric vehicles have seen far faster adoption than consensus expected—and this growth can and will continue.

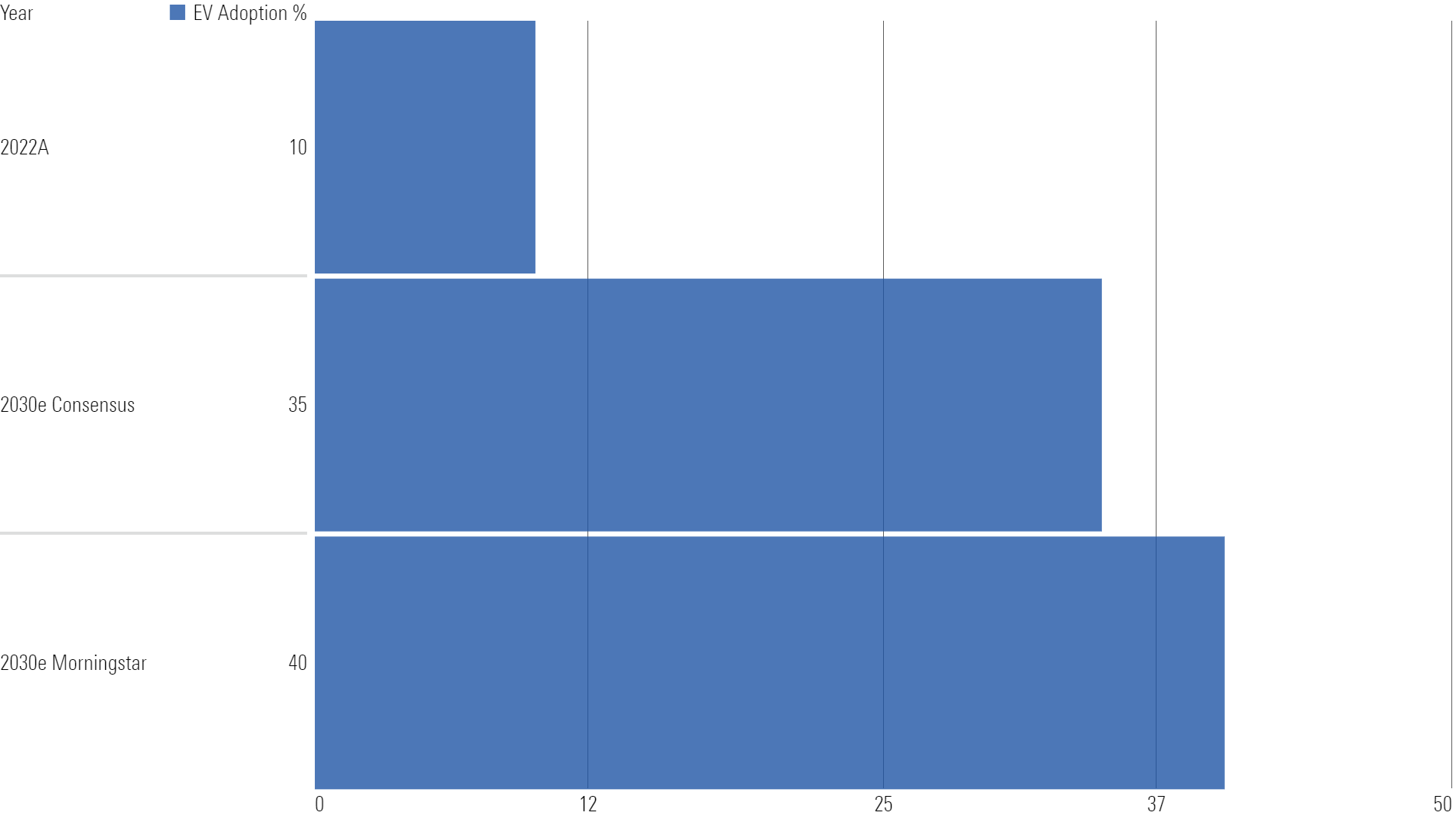

By 2030, we forecast EVs will account for 40% of global auto sales—more than 5 times the number of EVs sold in 2022. This translates to roughly 40 million vehicles, with an additional 20 million hybrids.

Our 2030 40% EV Adoption Forecast Is Above the Consensus Average of 35%

While we see growing EV volume globally, adoption rates will differ by country: We forecast that China will continue to be the global leader in EV sales and adoption, and Europe will remain second. We expect that the United States, which is currently a laggard, will catch up to the global rate by 2030.

While EVs still cost more than most auto categories, we expect falling battery costs will drive cost parity over the next couple of years in the majority of autos. Consumer function concerns are rapidly disappearing. As EVs have reached range parity with internal combustion engines, or ICEs, and charge times have fallen, the buildout of chargers across highways and in cities throughout the world will drive higher EV sales even without subsidies.

With growth accelerating over the second half of the decade, we see strong opportunities for investors throughout the EV supply chain.

We’re More Bullish on EV Adoption Than Consensus

| Topic | What the Market Is Saying | How We’re Differentiated |

|---|---|---|

| EV adoption | EV growth is dependent on subsidies remaining in place over the long term. | EV/ICE cost parity removes dependence on subsidies, as subsidies only provide temporary impact. |

| Cost parity | Cost parity between EVs and ICEs occurs when battery pack costs reach $100/kWh regardless of vehicle type. | Vehicle type is an important factor in cost. EVs are currently cheaper for luxury sedans and CUVs with battery prices at $151/kWh. Entry-level cars will reach parity at $110/kWh. |

| Functional parity | Functional parity is less important to adoption than cost. | Functional parity is as important as cost. Road trip anxiety currently limits EV adoption. |

| 2030 global EV adoption rate | 35% | 40% |

| Regional adoption | China and Europe will be the only regions to see large EV adoption. | Large EV adoption will occur in China, Europe, U.S., Canada, Japan, and South Korea. EV adoption in a country is highly dependent on the charging infrastructure. Countries that build plentiful public EV chargers will see higher EV adoption rates. |

EV Supply Chain Industry Analysis and Our Top Picks

Rising battery electric vehicle sales will transform multiple industries throughout the supply chain, and the transition to electric vehicles has also created opportunities throughout the EV charging value chain, which includes the buildout of EV chargers and the required supporting infrastructure.

Below, see our top picks for investing in each associated industry. Although all industries will benefit from the transition to EVs, we think investors should particularly explore opportunities in auto suppliers, electronic components, and lithium.

Our Top Pick Among Auto Suppliers: BorgWarner BWA

- Morningstar Rating: 5 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): $72

BorgWarner makes motors, gearboxes, inverters, converters, battery management systems, onboard chargers, and software for EVs. The company also combines components and software into a complete integrated drive module.

BorgWarner’s narrow-moat rating comes from the intangible asset moat source derived from a continuous flow of intellectual property. The firm also benefits from the switching cost moat source.

In 2030, BorgWarner targets around 48% of its revenue from EVs, up from about 6% in 2022. We expect revenue to average 2 to 4 percentage points of growth in excess of global light vehicle production as EV penetration outpaces declines in ICE.

Our Top Pick Among Electronic Components: Sensata Technologies ST

- Morningstar Rating: 5 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): $71

Sensata Technologies sells sensors and electrical protection into EVs. The firm’s narrow economic moat stems from switching costs for its OEM customers, as well as intangible assets in sensor design.

Sensata is targeting $2 billion in electrification revenues in 2026, up from less than $500 million in 2022. Half of this (more than $1 billion) is to come from autos.

Our Top Pick Among Lithium Producers: Albemarle ALB

- Morningstar Rating: 5 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): $350

Albemarle’s largest business is lithium production, which generates nearly 90% of profits. Lithium will benefit from increased EV adoption as higher lithium demand will result in higher prices and profits.

Our narrow moat rating stems from Albemarle’s cost-advantaged lithium production. Albemarle operates three of the lowest-cost resources globally.

Albemarle is investing in expanding its lithium capacity roughly 4 times over the next decade, largely through lower-cost brownfield capacity expansions. We view these investments as value-accretive given our favorable EV outlook.

Our Top Pick Among Auto OEMs: General Motors GM

- Morningstar Rating: 5 Stars

- Morningstar Economic Moat Rating: None

- Fair Value Estimate (as of Sept. 12, 2023): $78

GM’s ambition is to only sell zero emission light duty vehicles globally by 2035. The Buick and Cadillac brands will transition to BEV only by 2030, and it is offering one of the few affordable mass market BEVs starting this year with the $30,000 Chevrolet Equinox CUV.

GM plans to invest $35 billion on EV and AV development from 2020 to 2025. By the end of 2025, it intends to launch 30 EVs and have about 1 million annual BEV unit production in North America and another about 1 million in China. It also has its proprietary Ultium battery technology that it is selling to other firms such as Honda.

Our Top Pick Among Batteries: Samsung SDI 006400

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: None

- Fair Value Estimate (as of Sept. 12, 2023): KRW 802,000

Samsung SDI is one of the largest EV battery suppliers globally, with battery manufacturing sites around the world to supply automakers.

We forecast Samsung SDI’s revenue will grow at a 20% compound annual rate through 2025 largely driven by battery growth. However, we are not confident that the company will be able to earn an excess return in the longer term, as EV battery suppliers lack sufficient pricing power and stick relationships with automakers.

We forecast battery revenue will grow at a 27% compound annual growth rate as Samsung SDI is investing heavily in the buildout of its battery manufacturing capacity.

Our Top Pick Among EV Chargers: ChargePoint CHPT

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: None

- Fair Value Estimate (as of Sept. 12, 2023): $8

ChargePoint is a provider of EV charging software and equipment across all end markets: home, commercial, and fleet.

We assign ChargePoint a no-moat rating. We think the company has moaty aspects in the Level II charging market (slow charging), but less so in Level III (fast charging), where competition is fierce.

ChargePoint is focused on growth across its end markets of home, commercial, and fleet as EV penetration rises. The company has also expanded into Europe, which currently accounts for around 20% of revenue.

Our Top Pick Among Raw Materials: Glencore GLEN

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: None

- Fair Value Estimate (as of Sept. 12, 2023): GBX 510

Glencore is exposed to EVs through material copper, cobalt, and nickel production and earnings.

We think the company’s commodities trading and marketing operations would likely be worthy of a narrow moat on their own, based on cost advantage. However, Glencore’s mining assets on average are not moatworthy.

Glencore has been relatively disciplined with capital allocation, and the growth outlook for the major EV exposed metals is generally flat. Cobalt is the exception and is set to grow about 40% by 2025 from 2022 levels as production cuts initiated in 2019 are versed and its Katanga mine increases production.

Our Top Pick Among Specialty Chemicals: Celanese CE

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): $160

Celanese is the largest producer of engineered materials, which are the plastics that are often used to replace metals in autos. Nearly 50% of the company’s end market sales are to the auto industry, with EVs creating the opportunity for Celanese to sell more content per vehicle.

Celanese recently acquired the majority of DuPont’s mobility and materials portfolio, which was highly exposed to the auto end market. After integrating the acquisition into the engineered materials segment, Celanese should be well positioned to grow from a recovery in global auto production and the shift to EVs.

Our Top Pick Among Automotive Semiconductors: Infineon Technologies IFX

- Morningstar Rating: 4 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): EUR 47

Infineon is the market leader in power semiconductors, and such semis are prominent in EVs to deliver power throughout the car system. It has several large contracts to supply SiC semis into EV inverters. 40%-plus of its revenue comes from automotive in total.

Our narrow moat rating is based on intangible assets stemming from decades of chip design expertise, as well as high customer switching costs because of costly redesigns. Infineon is well exposed to rising chip content per car. We estimate that semi content in cars should rise roughly 5% faster than global light vehicle sales, thanks to content gains per vehicle, including EVs.

Our Top Pick Among Utilities: Edison International EIX

- Morningstar Rating: 3 Stars

- Morningstar Economic Moat Rating: Narrow

- Fair Value Estimate (as of Sept. 12, 2023): $74

Edison’s Southern California electric utility has the largest EV charging network investment plan among all U.S. utilities. Edison projects nearly 3 million EVs will be in its service territory by 2030.

As a fully regulated distribution utility, Edison’s service territory monopoly in Southern California and its efficient-scale advantage are its primary sources of a narrow economic moat. California utilities regulation is mostly constructive, as the state realizes it needs financially healthy utilities that can attract capital to support its environmental goals.

Edison plans to spend $6 billion annually during the next three years on electric distribution and transmission grid upgrades in California, representing 7% annual growth in its asset base. As EV penetration grows, we expect investment in EV-related infrastructure and energy storage to make up a larger share of its growth investment.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ca8d2ce1-cd0f-433b-a52b-d163be882398.jpg)