After Earnings, Is Albemarle Stock a Buy, a Sell, or Fairly Valued?

With falling lithium prices and a focus on free cash flow, here’s what we think of Albemarle’s stock.

/s3.amazonaws.com/arc-authors/morningstar/ca8d2ce1-cd0f-433b-a52b-d163be882398.jpg)

Albemarle ALB released its fourth-quarter earnings report on Feb. 14. Here’s Morningstar’s take on Albemarle’s earnings and the outlook for its stock.

Key Morningstar Metrics for Albemarle

- Fair Value Estimate: $300.00

- Morningstar Rating: 5 stars

- Morningstar Economic Moat Rating: Narrow

- Morningstar Uncertainty Rating: High

What We Thought of Albemarle’s Earnings

- Albemarle’s fourth-quarter results confirmed our view that the company is focusing on generating free cash flow over growing lithium volume amid the decline in lithium prices. As the company cuts operating expenses, this should support profits, and as it plans to cut capital expenditures and optimize working capital, this should support higher cash flow in 2024. Management’s market commentary also confirms our view that growing demand and slowing supply will lead to prices rising in 2024. Having updated our model to incorporate fourth-quarter results, we maintain our fair value estimate of $300 per share. Our narrow moat rating is also unchanged.

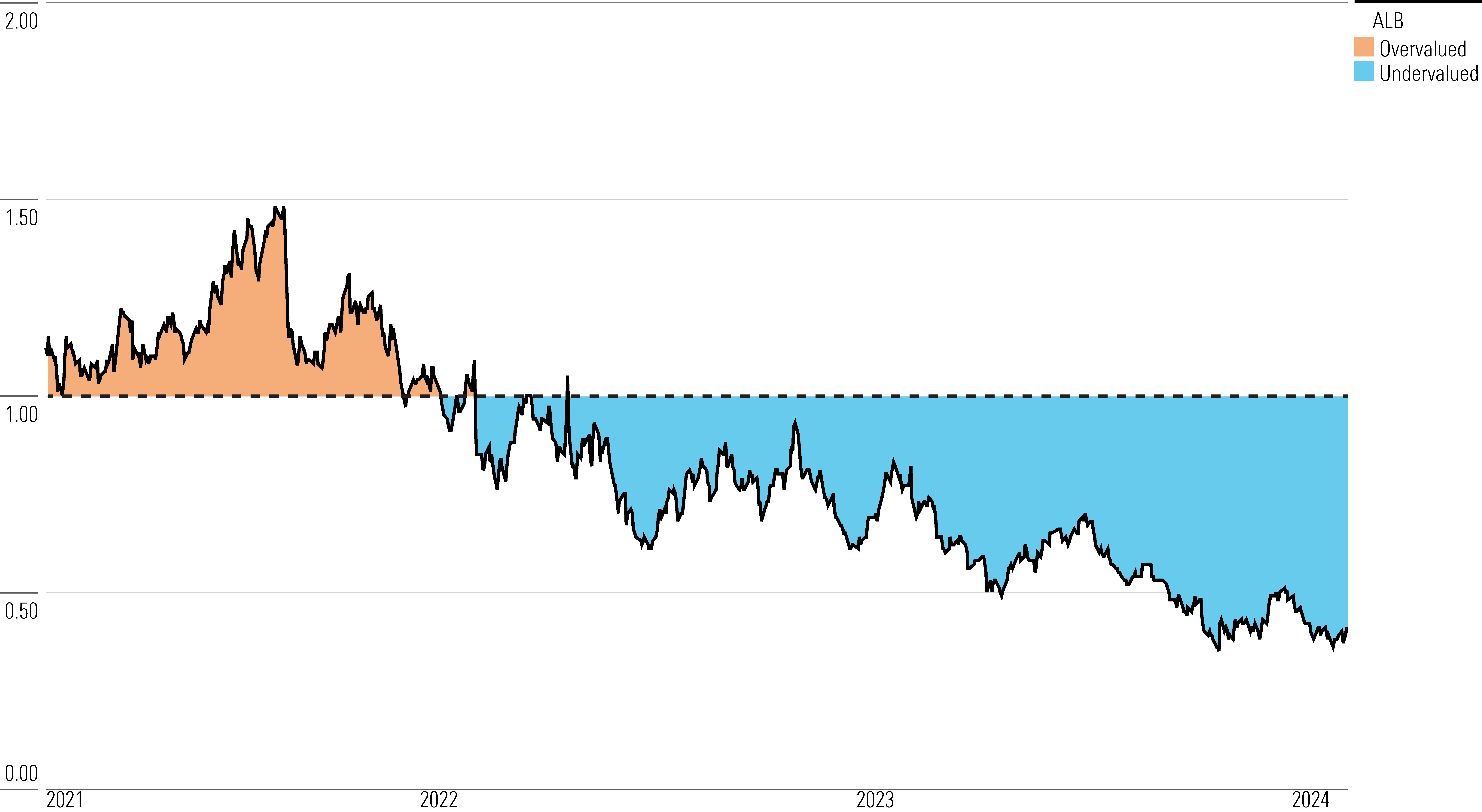

- Albemarle shares rose immediately after earnings, as the market reacted positively to the outlook. However, at current prices, we view the stock as materially undervalued, trading at a little less than 40% of our fair value estimate.

- We view current lithium prices as being at cyclically low levels, below the marginal cost of production. In response, higher-cost existing production has shut down, while new projects have been delayed at all major producers, including Albemarle.

- As electric vehicle sales grow and more utility-scale batteries are built, we forecast lithium demand will grow 10% to 1.1 million metric tons by the end of 2024. As total supply growth slows, we expect the market will move into a supply deficit, leading to prices rising, particularly in the second half of the year.

Albemarle Stock Price

Fair Value Estimate for Albemarle

With its 5-star rating, we believe Albemarle’s stock is significantly undervalued compared with our long-term fair value estimate.

The bulk of the company’s growth will come from lithium. We expect contract lithium prices will rise in 2024. Lithium carbonate spot prices, which tend to be a leading indicator of contract prices, are currently around $13,500 per metric ton (based on published indexes), down from $75,000 at the end of 2022, due to slowing lithium purchases as a result of inventory destocking. However, as demand growth remains strong and outpaces supply, we expect prices will stabilize in the first half of 2024 and rise in the second half of the year.

In the longer term, we expect lithium prices will remain well above our long-term forecast for lithium carbonate at $12,000 per metric ton through the rest of the decade. Based on our price elasticity analysis, we forecast index prices will average a little over $25,000 per metric ton for the remainder of the decade. We expect high-quality lithium hydroxide used in long-range batteries will continue to sell at a premium to carbonate, reflecting higher conversion costs.

Our price forecast is based on our forecast for the marginal cost of lithium production on an all-in sustaining cost basis. We expect lithium demand to grow nearly 20% annually from around 800,000 metric tons in 2022 to over 2.5 million metric tons by 2030. By then, roughly 95% of lithium demand will come from batteries that require high-quality lithium with few impurities. To meet demand, higher-cost supply will need to come online from lower-quality resources that will require higher processing costs.

Read more about Albemarle’s fair value estimate.

ALB PF

Economic Moat Rating

We award Albemarle a narrow moat based on its strong and durable cost advantage in lithium and bromine production. Globally, lithium carbonate is produced from either lower-cost evaporation of brine or higher-cost mining of spodumene minerals. Albemarle has a cost advantage in lithium carbonate production due to its lucrative brine assets in the Salar de Atacama in Chile, which produces lithium at the lowest cost globally, excluding royalties. Albemarle has a long-term contract through 2043 with the Chilean government to extract around 80,000 metric tons of lithium per year.

Read more about Albemarle’s moat rating.

Risk and Uncertainty

We assign Albemarle a High Uncertainty Rating. The firm’s biggest risk comes from volatile lithium prices. Prices could decline if EV demand grows slower than expected, or if new low-cost supply ramps up quicker than demand. New batteries, such as sodium-ion, could overtake lithium as the preferred energy storage resource.

Lithium production could ramp up more quickly than demand warrants if producers bring too much supply to the market. Further, new lithium production technologies could alter the cost curve in carbonate and hydroxide. Albemarle faces execution risk in ramping up its lithium production, which includes production delays and cost overruns.

Albemarle is also subject to political risk, especially in Chile. Under President Gabriel Boric’s announced plan to nationalize lithium, the Chilean government would own a majority stake in all projects. If this occurs, Albemarle could be forced to sell a 51% stake to the Chilean government at a price as low as asset book value to extend its lease when it expires in 2043.

Read more about Albemarle’s risk and uncertainty.

ALB Bulls Say

- Albemarle has top-tier lithium assets through its brine operations in Chile and spodumene hard-rock operations in Western Australia, which are among the lowest-cost sources of lithium production globally.

- Lithium prices should remain well above the marginal cost of production through at least the remainder of the decade, leading to excess profits and return on invested capital for Albemarle.

- Albemarle has low-cost bromine production through its highly concentrated brines in the Dead Sea and Arkansas.

ALB Bears Say

- Lithium prices will fall if new supply comes online faster than demand, which will weigh on profitability. Albemarle’s plans to increase its lithium production capacity will prove value-destructive in the wake of lower prices.

- Albemarle’s bromine business will decline from weak demand for flame retardants as consumers shift from computers to less bromine-intensive tablets and smartphones.

- Chile’s plan to nationalize lithium could result in Albemarle being forced to sell a majority stake to the government at a price around asset book value, destroying shareholder value.

This article was compiled by Frank Lee.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ca8d2ce1-cd0f-433b-a52b-d163be882398.jpg)