Ultimate Stock-Pickers: Top 10 Buys and Sells

The first part of 2018 saw buying conviction pick up, with buying activity among several key names.

By Eric Compton | Equity Analyst

For the past nine years, Ultimate Stock-Pickers' primary goal has been to uncover investment ideas our equity analysts and top investment managers find attractive, in a manner timely enough for investors to gain some value. As part of this process, we scour the quarterly (in some cases, the monthly) holdings of 26 different investment managers, 22 of which manage mutual funds that Morningstar's manager research group covers, and four of which manage the investment portfolios of large insurance companies. As they become available, we attempt to identify trends and outliers among their holdings as well as any meaningful purchases and sales that took place during the period under examination.

In our last article, we walked through some of the buying activity we were seeing from our Ultimate Stock-Pickers during the first quarter of 2018 (and April for those that report it). The piece itself was an early read on the purchases—focused on high-conviction and new-money buys—that were made during the period. In our current article, we take a look at the aggregate buying and selling, rather than the individual buys and sells we looked at in our last article. Breaking a long-standing trend, our Ultimate Stock-Pickers were net buyers during the most recent period. While selling conviction was within a normal range, buying conviction was the highest we have seen it in years. Currently, our market fair value estimate stands at 0.98, suggesting stocks are within the realm of reasonableness.

As for sector allocation, our top managers remained meaningfully underweight in energy, healthcare, and utilities relative to the weightings of the S&P 500 Index at the end of April. Our Ultimate Stock-Pickers also continue to hold meaningfully overweight positions in the basic materials, technology, financial service, and industrial sectors (with their exposure to communication services, real estate, consumer defensive, and consumer cyclical being less than 100 basis points off the benchmark index).

The trend of more and more capital flowing into passive products has likely made the stock-picking environment more difficult as it results in all equities appreciating, regardless of the valuation of individual constituents. That said, our Ultimate Stock-Pickers still found some names that piqued their interest, and we believe these are worth highlighting from a valuation perspective.

The conviction buying that took place during the first quarter of 2018 (and the beginning part of the second quarter of 2018) was once again focused on high-quality names with defensible economic moats, exemplified by a high number of wide- and narrow-moat companies on our list of top 10 (and top 25) high-conviction purchases, although several no-moat insurance names did make the cut.

As for the selling activity during the period, most of it seemed to revolve around paring stakes that already were and continue to remain widely held, including wide-moat

Ultimate Stock-Pickers' Top 10 Stock Holdings (by Investment Conviction)

The overall makeup of the top 10 stock holdings by investment conviction did not change compared with last period—only their order changed.

Microsoft, Comcast, Berkshire, and Wells Fargo are the only names from the top holdings list that are trading at relatively attractive valuations compared with our analysts' fair value estimates. We have chronicled Wells Fargo in the past, and the firm has had its ups and downs. Wells Fargo was trading at a relatively attractive price point, according to Morningstar analyst Jim Sinegal, through much of 2016, before trading up roughly 30% through the first quarter of 2017. Then shares slid, dropping almost 20% by September 2017, where again Sinegal argued that shares looked attractive. Shares then traded up over 30% before finally sliding once again, back down to where they are today. Shares are now at a 16% discount to Sinegal's $65 fair value estimate.

After yet another settlement with regulators (this time for 1B), and an admission to additional internal issues related to altered information on customer accounts, Wells can't seem stay out of the negative news cycle and away from self-inflicted damage. Sinegal did not find the latest developments too surprising as Wells Fargo has more than 250,000 employees, and the firm’s practices are being examined with a fine-toothed comb by regulators and managers.

He also notes that the latest revelations should not be material to the firm’s financial prospects, as the alterations do not appear to have generated any additional revenue. Instead, mundane information was being added outside of proper channels. Rather, the bigger question for Sinegal, given management’s comments and the fact that this particular behavior continued into 2018, is whether top management is truly intent on conducting a ruthless transformation of the company’s culture. While he doesn't believe the bank is out of the woods yet, and further changes may be needed to catalyze the company’s comeback in the eyes of customers and investors, he does believe the bank's wide moat is still intact.

Wells remains the top deposit gatherer in the United States, with deep customer relationships and an enviable branch network—and account closures did not spike even during the worst of the bank's sales problems. If the bank can gradually rebuild its image and get control over its internal issues, shares may yet again be attractively priced today.

Berkshire also looks attractively priced, based on Morningstar analyst Gregg Warren's $220 fair value estimate for B shares and $330,000 fair value estimate for A shares. Warren has been an analyst on the panel for the Berkshire annual meeting for years, and his experience and the questions asked this year gave him some key takeaways regarding future capital deployment.

Warren continues to believe that Berkshire has too much cash and not enough good options to deploy it. With the firm likely to generate $5 billion-$10 billion in free cash flows quarterly going forward, he expects that over the next five years Berkshire will reach the $150 billion cash threshold that Buffett has said would be difficult to defend to shareholders. Absent a large (or several large) acquisition(s), Warren expects the firm to start returning more of its excess cash to shareholders. While share repurchases are Buffett's preferred option, Warren still believes that a special one-time dividend may end up being the bitter pill Buffett has to swallow if Berkshire can't find a way to put its excess cash to work in acquisitions, investments, or share repurchases in the near term.

Either way, shares are currently trading at roughly a 13% discount to Warren's fair value estimate, and, based on a $211,184 book value per Class A equivalent share at the end of the first quarter (and depending on how fast this book value has grown since then), Buffett should be willing to buy back stock at prices below $253,421 ($168.95) per Class A (B) share, giving investors some downside protection.

Ultimate Stock-Pickers' Top 10 Stock Purchases (by Investment Conviction)

Taking a closer look at the high-conviction buying that we uncovered during the most recent period, there was a moderate amount of overlap with the same list last quarter. Our managers continued to buy up stakes in Apple (primarily Berkshire),

As for the sectors our top managers focused on, there were three firms each from the financial services and healthcare sectors, as well as three technology names. Wide-moat rated

Lastly, we purchased a small position in Facebook towards the end of the quarter. Remarkably, Facebook controls four social media platforms with more than a billion global users each: Instagram, WhatsApp, Facebook Messenger, and the original Facebook "Blue App." Though doing so will involve substantial cost, we believe the company will take necessary steps over the coming months and years to restore the damaged trust of its users and advertisers. After factoring these costs into our valuation, we believe the recent controversy enabled us to purchase a very unusual business franchise riding several powerful secular trends at a price-earnings multiple only a little higher than that of the overall stock market. Though Facebook has unquestionably committed sins for which it must now atone, we believe it remains a far more competitively advantaged, economically attractive, and faster-growing enterprise than the average American business.

This was in line with the view Morningstar analyst Ali Mogharabi took on the name (profiled in our last article) following the stock's precipitous decline, and the recovery predicted by both Mogharabi and Sequoia has essentially already played out.

AIG was also purchased with conviction by multiple managers, three to be exact, most notably by

We started our AIG investment when its shares were valued at 10 times earnings, and after it had underperformed the S&P 500 by more than 20% over three years. We viewed AIG’s new leadership, strong balance sheet, and improving combined ratio as long-term value drivers. As well, recent indications of property & casualty premium headwinds should prove transitory, and we took advantage of volatility in the quarter to add to our position.

This is essentially in line with Morningstar analyst Brett Horn's view on the name as well (which was profiled in our last article). Horn argues it is only a matter of time before the strong new management team with a history of success and improving combined ratios help AIG trade closer to his fair value estimate of $76.

MetLife also caught our eye, as it was the second, no-moat insurer to make the list this quarter, something we don't see too often. Diamond Hill, the major conviction buyer, did not have much to say regarding the name during the most recent quarterly commentary, and Morningstar analyst Brett Horn views the name as close to fairly valued, although there may be some room for appreciation as it is trading at roughly a 10% discount to his $52 fair value estimate.

As with most life insurers, Horn does not believe MetLife has a moat, nor does he see a credible path toward creating one in what is a commoditized business. He does see rising interest rates and several recent strategic moves as positives, however. The company recently spun off Brighthouse, which represented a substantial portion of its retail operations and accounted for about 20% of its operating earnings. The divested operations include the bulk of MetLife's variable annuity business. Horn views this move favorably and likes the overarching strategy to shift MetLife toward greater transparency and more stable cash flow production. While Horn does not see this leading to a moat, he believes a move away from more complex business is a positive change for shareholders in the long run.

Horn does not believe recent, negative reserve developments will significantly impact the value of the firm. Management recently discovered that the processes by which the company attempts to locate missing or unresponsive annuity and pension recipients was insufficient, and historical reserve releases related to this issue were inappropriate.

As a result, it has had to restate historical results. The amount of the reserve charge is not material to Horn's overall valuation, but he believes this situation highlights the opaque nature of life insurance accounting and supports his high uncertainty rating for MetLife. As a result, even at a 10% discount, the firm is still trading in 3-star territory, and investors may do better to wait for a more attractive entry point.

Wide-moat rated

Parnassus was buying CVS with the most conviction, and CVS is the fund's third largest holding. The fund had this say about the name from its most recent quarterly commentary:

Drugstore chain CVS Health reduced the Fund’s return by 68 basis points (a basis point is 1/100th of one percent) as its stock dropped 14.2% from $72.50 to $62.21. Shares fell after the company announced it would invest a significant portion of its tax savings to increase wages and pilot enhanced service offerings, rather than drop the savings to the bottom line. Additionally, investors remain concerned that CVS’s proposed acquisition of Aetna may not gain regulatory approval due to other pending large-scale transactions involving health insurers. Nonetheless, shares are currently trading at a very attractive valuation. CVS has a unique collection of assets, and we believe the company is well positioned to improve care and reduce healthcare costs with or without Aetna.

With CVS trading at a 35% discount to Lekraj's fair value estimate, there does seem to be some margin of safety if CVS can make the Aetna merger work without too much shareholder value destruction or if it can prosper on its own even without the merger, as Parnassus suggests.

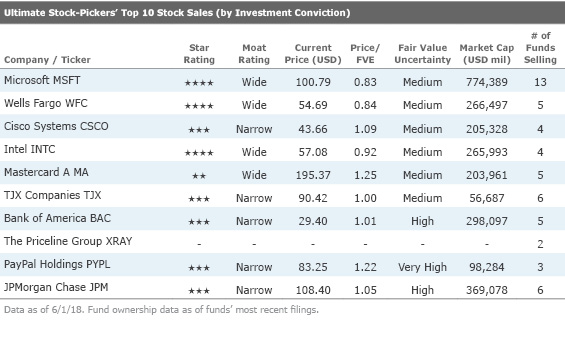

Ultimate Stock-Pickers' Top 10 Stock Sales (by Investment Conviction)

As has been the case for several periods, wide-moat Microsoft continues to be the most widely sold security. Shares of the technology firm were sold by 13 of the 17 managers that held it coming into the first quarter, with seven of our Ultimate Stock-Pickers selling with conviction. That said, three of our top managers did add shares of Microsoft to each of their respective portfolios during the period, albeit in small quantities.

As tends to be the case, many of the most widely sold securities tended to remain top holdings despite seeing a fair amount of selling during the period, with many of our top managers who were selling already having large exposures to each stock. We should also note that a majority of the names on our list of top 10 stock sales this period are currently trading nearly at or above our fair value estimates. The only exceptions, at over a 10% discount, were wide-moat rated Microsoft and Wells Fargo.

The most notable conviction sales to us during the period were narrow-moat rated

The award for highest conviction sale this quarter goes to Dentsply, with the outright sale by Sequoia. The firm did not have much comment on this sale; however, shares have been down over 30% since the start of the year. Morningstar analyst Michael Waterhouse believes shares have looked overvalued for some time, with shares trading well above his fair value estimates for all of 2016 and 2017, and the recent pullback has finally made shares fall back down to fairly valued territory.

Dentsply merged with Sirona back in 2016, and it appears the firm may have overpayed based on subsequent results. Multiple members of the management team of the combined firm resigned in late 2017 as a result of these disappointing results. Waterhouse still sees more threats on the horizon for the firm, including the growth of lower priced competitors, even in specialty dental markets, where the firm was hoping to build up more higher-margin business.

While shares are more attractively priced than they have been in years, there is still not a large margin of safety to Waterhouse's $49 fair value estimate based on his medium uncertainty rating, and investors may do better to wait for a more attractive entry point.

Disclosure: Eric Compton has no ownership interests in any of the securities mentioned here. It should also be noted that Morningstar's Institutional Equity Research Service offers research and analyst access to institutional asset managers. Through this service, Morningstar may have a business relationship with fund companies discussed in this report. Our business relationships in no way influence the funds or stocks discussed here.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)