How to Size Up a Job's Benefits

When evaluating a job offer and negotiating a salary, take missing benefits into account.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

If you're considering a job offer, listing the pros and cons can help put things into better focus. Sometimes it’s as easy as choosing the job that pays the highest salary, but often it's more nuanced than that.

Increasingly, people value lifestyle considerations when making job choices. While researching this article, I read a lot of “top employee benefits” lists. Highly ranked benefits include things like flexible work schedules and remote work options--two practices that were fast-tracked into acceptance during the coronavirus pandemic and are likely here to stay at many companies. Employees also value things like generous paid time-off policies and parental leave policies.

Only you know which benefits are most important to you. But when you're considering a job offer, don't forget about the “old school” type of benefits that you can put a dollar value on. Ask yourself if the job you’re considering is light on some of the more traditional benefits, discussed below. If it is, consider how much it would cost to replace the benefit on your own, then consider using that figure to negotiate for a higher salary.

Does it offer healthcare benefits?

Value: ~$5,000/year (~$14,000 family coverage)

Traditionally, healthcare benefits have been one of the biggest enticements corporations have had to offer American workers. It’s mutually beneficial, really: Corporations want their workers to be happy and healthy--of course!--but they also get nice tax breaks. Employer-paid premiums for health insurance are exempt from federal income and payroll taxes. Additionally, the portion of premiums that employees pay is typically excluded from taxable income. For these reasons, employer-sponsored insurance plans have traditionally been the most affordable health insurance coverage option for most U.S. families.

Companies usually don't pay for 100% of their employees' health insurance, but they do pay a significant portion of it: an average of 67%, according to the Bureau of Labor Statistics.

Healthcare has become more widely available and affordable since the dawn of the Affordable Care Act, but it is still pricey and should be figured into a budget. In 2020, the average annual premiums were $7,470 for single coverage and $21,342 for family coverage, according to the Kaiser Family Foundation.

Note: Many companies offer a choice of healthcare plans with different price points. A high-deductible healthcare plan might be worth a look if you’re reasonably healthy and on a budget. HDHPs have cheaper premiums, but you have to pay a certain amount out of pocket before your insurance starts covering expenses. How much? In 2021, a high deductible is at least $1,400 for a self-only insurance plan and $2,800 for a family plan. Besides being economical, another benefit of HDHPs is that they enable you to save with a health savings account, which is a pretty neat type of account with truly excellent tax benefits. HSAs allow you to spend tax-advantaged dollars on current healthcare costs and invest the balance for future healthcare costs. And it’s portable, meaning you can take it with you if you decide leave your job.

Is there a good retirement savings plan with employer match?

Value: extra ~3% of your salary, invested in your choice of retirement funds, every year. FREE MONEY WITH EXPONENTIAL GROWTH POTENTIAL!

One benefit some companies offer is a 401(k) match. It’s even better when paired with a high-quality 401(k) with low administrative fees that offers high-quality investment options--see this article by Christine Benz that discusses how to evaluate a 401(k) plan’s quality and lobby for a better one, if necessary.

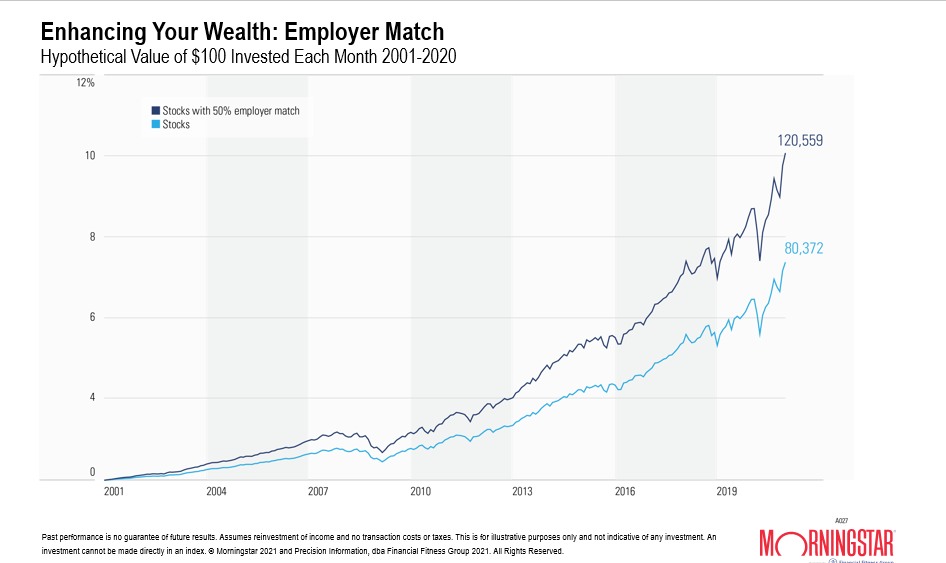

The exhibit below shows what a big difference the match makes. The light blue line shows the growth of $100 invested in stocks at the end of each month. The dark blue line represents the same investment with a 50% employer match. (In other words, $150 invested each month as opposed to $100.) Because investment returns grow exponentially and not in a linear pattern, funding your retirement account with as much money as early as possible gives you the best growth potential.

Source: Morningstar Presentations, available in Morningstar Office.

Does it offer a dependent care flexible spending account?

Value: Tax savings on up to $10,500 in childcare expenses

Check to see if the employer offers any potential savings on childcare, such as a dependent care flexible spending account. This is a handy tool that can save you some money.

A dependent care FSA allows you to set aside a maximum of $10,500 of pretax money that you can use to pay for preschool, summer day camp, or after-school care for children younger than 13. (Tuition and fees associated with kindergarten or elementary school do not qualify.) Some employers may also contribute to a dependent care FSA, but the combination of employee and employer contributions cannot exceed the maximum. (The maximum was previously $5,000, but it was temporarily lifted to $10,500 for 2021 as a result of the American Rescue Plan.)

Because you are setting the money aside before it is subject to payroll tax, you wind up paying less in taxes and ultimately increasing your take-home pay. The higher your salary (and hence, the higher your tax bracket), the bigger your FSA benefit.

Be aware, however, of a potential drawback of dependent care FSAs: Unlike HSAs, dependent care FSAs are not portable and you have to spend the whole balance by the end of the year or you lose it; you are not allowed to carry it forward. (Some employers allow a short grace period after year-end.) As such, this option really only makes sense if you are confident you will spend at least the amount you put in the account every year.

Does it offer group disability insurance coverage?

Value: Average cost of disability insurance policy is 1-3% of annual gross income

According to a study done by the Social Security Administration, about one in four 20-year-olds will become disabled and unable to work for at least a year before retirement age.

Have a plan in place in case this happens to you. One cost-effective way to hedge against this risk is group disability insurance coverage--if your employer offers it, make sure you're signed up for it, and make sure you understand the coverage it provides--what percentage of your salary will it pay and for how long (up to one year).

Also make sure you understand the tax implications, because they can be tricky: If your employer pays the premiums (or if you are paying the premiums with pretax dollars), the disability income you receive will be taxable. That's important because if your short-term disability policy will cover only 60% of your pretax salary, be aware that the taxes due will further reduce the benefit, so you might not have as much income replacement as you thought.

If you pay the premium with after-tax money, the income you receive will be tax-free.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)