You Probably Own Too Much Domestic Equity

Home bias is a global phenomenon that reduces diversification.

/s3.amazonaws.com/arc-authors/morningstar/984ff87e-463c-4fca-8c15-ebbf7f9593b2.jpg)

The article was published in the October 2021 issue of Morningstar FundInvestor. Download a complimentary copy of FundInvestor by visiting the website.

Your portfolio probably needs a higher international-stock weighting. Maybe you've boosted the non-U.S. weighting lately, because many investors have. You may know that, for a long time, foreign stocks were considered riskier than U.S. stocks, so a 20% to 25% weighting in foreign fare was an aggressive stance for an American investor. But studies suggest that foreign stocks add diversification and are not as risky as people think.

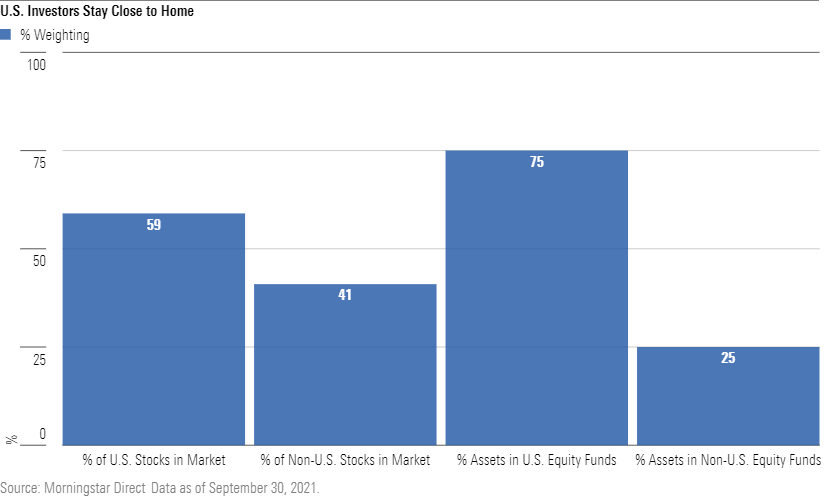

Even though many U.S. investors have raised their foreign weightings, they still have not caught up to recommended levels. Home bias occurs when an investor prefers domestic to foreign securities (for whatever reason) and consequently owns more than a market weighting in those securities. That's what most Americans do. As of Oct. 29, 2021, the FTSE All-World Index had a 59% weighting in U.S. stocks and 41% in non-U.S. stocks. In 2019, FTSE Russell released a research paper on home bias, showing that U.S. pensions were overweight domestic stocks by 10 percentage points. According to Morningstar data as of Sept. 30, 2021, including mutual funds and exchange-traded funds, there was $12.5 trillion in U.S. equity funds and $4.2 trillion in international-stock funds--meaning a nearly uncanny 75% and 25% home to abroad split.

It's worth noting that Americans' underweighting in foreign stocks is less problematic than those in other countries because U.S. stocks make up more than half the market. FTSE Russell shows that investors elsewhere have a much worse home bias. Japanese and British stocks have just 8% and 6% weightings, respectively, in the global index, but their pensions' equity stakes are roughly 35% domestic. But the world champion of home bias is Australia. Australian stocks have only a 2% weighting globally, but its pensions devote 52% of equity assets to Australian equities. There's another significant problem Down Under: Two sectors, financial services and basic materials, take up half the Australian equity market, meaning that geographic risk creates significant sector risk there.

In fact, there are a few valid reasons why a U.S. investor might want an above-market weighting in domestic companies. Investing abroad can cost more, political risks exist, and--most importantly--there are currency issues. Currencies fluctuate considerably, and people tend to spend their home currency more than foreign currency. So, it's reasonable for Americans to tilt slightly toward U.S.-dollar-denominated securities--especially as they approach retirement.

If those are your reasons, a home tilt might make sense. But home bias doesn't typically start with rational, economic explanations. More often it comes from national pride and investors' desire to "invest in what they know." Patriotism and familiarity are fine, but they're not a strong foundation for investing success. Diversification, on the other hand, is a proven way to improve investment returns and reduce risk. Investing abroad increases diversification; home bias, by default, limits it.

Recently, we upgraded Fidelity Multi-Asset Index FFNOX, which used to be called Fidelity Four-in-One Index, to a Morningstar Analyst Rating of Gold from Silver after the firm renovated the fund's process and portfolio. A huge number of factors are considered when rating a fund, but here one of the most crucial was the firm's decision to move from the long-standing 70% weighting in U.S. stocks to a marketlike 60%. It's no coincidence that the only other Gold-rated fund in the allocation–70% to 85% equity Morningstar Category, Vanguard LifeStrategy Growth VASGX, holds 61% in U.S. stocks and 39% in non-U.S. stocks.

The two funds do stand out in the category. The average split between U.S. equities and non-U.S. equities was 76% to 24% as of October 2021. True, a few funds are domestic-only, and some have specialized goals. Still, it seems that home bias remains entrenched--if less so than it once was. We encourage the oddly contrarian take: Allocate like the market.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MNPB4CP64NCNLA3MTELE3ISLRY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SIEYCNPDTNDRTJFNF6DJZ32HOI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZHTKX3QAYCHPXKWRA6SEOUGCK4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/984ff87e-463c-4fca-8c15-ebbf7f9593b2.jpg)