Target-Date Retirement Funds in 4 Charts

Navigating retirement involves a host of problems. These funds present a range of solutions.

/s3.amazonaws.com/arc-authors/morningstar/984ff87e-463c-4fca-8c15-ebbf7f9593b2.jpg)

Investors often receive tons of information about saving and investing for retirement, but the guidance on properly funding their spending during retirement is less clear. In some ways, that's understandable. After all, amassing the wealth necessary to fund a retirement comes first, takes multiple decades, and demands discipline.

Investing toward retirement is fairly straightforward. There's broad agreement that investors should start as soon as they can, invest as much as possible, and allocate heavily to equities early before gradually shifting to fixed income. Plus, for most investors, the amount of time they have to invest is fairly well defined: That's why target-date funds have dates in their names.

Navigating retirement, on the other hand, is a conundrum. First and foremost, there's no way to know how long your money must last. Most prudent advice suggests at least 25 years, but it can be 10 or 35. Spending levels may need to shift because of inflation, medical expenses, or other unknowable issues. Finally, the amount of income you'll receive generally fluctuates with interest rates. And all that is before assessing how and when to tap all the possible sources of income: Social Security, pensions, distributions from various IRA and 401(k) accounts, and so forth.

Funds intended to help retirees through retirement, which we group in the target-date retirement Morningstar Category, can't address all those issues. But they do strive to help investors focus on two key investment challenges: having enough income year to year and not running out of money. As we shall see, there's no broad consensus over how to navigate these connected challenges, and frankly there's no one right answer. Understanding the differing approaches of the 35 funds in this category can help investors figure out a strategy that suits their needs and preferences.

As it happens, the capital markets have provided potent illustrations of these matters the past few years. Interest rates were generally quite low for a decade, making income generation difficult, and in 2022, both bonds and stocks plummeted, demonstrating these funds' risks of losing money.

Target-Date Retirement Strategies

The established way to make sure that investors can maintain their standard of living without running out of money during retirement is capital growth—which comes from stocks. Over long periods of time, the higher the equity weighting in retirees' portfolios, the more growth they can expect to help combat inflation and overcome the risk of outliving one's savings. There are two problems, one fairly small and one large. First, equities don't tend to provide a tremendous amount of income through dividends. So, you cannot simply hold stocks. Second, equities are very susceptible to nasty downturns (that's why it's important not to allocate your retirement funds 100% to stock).

Traditional fixed income, such as cash and high-quality bonds (U.S. Treasuries), essentially flips the benefits and drawbacks of equity. That is, fixed income tends to provide more income than equities but generally doesn't provide significant growth. Correspondingly, high-quality fixed income tends to have less risk of quickly degrading capital in a downturn. Cash invested in ultrashort holdings (such as a money market fund) provides the most stability and the least income, generally keeping up with inflation at best. Bonds provide a bit more income with less stability, plus there's a spectrum of risk/reward. In that asset class, generally speaking, to lift reward (income), investors must take on additional interest-rate risk, credit risk, or both.

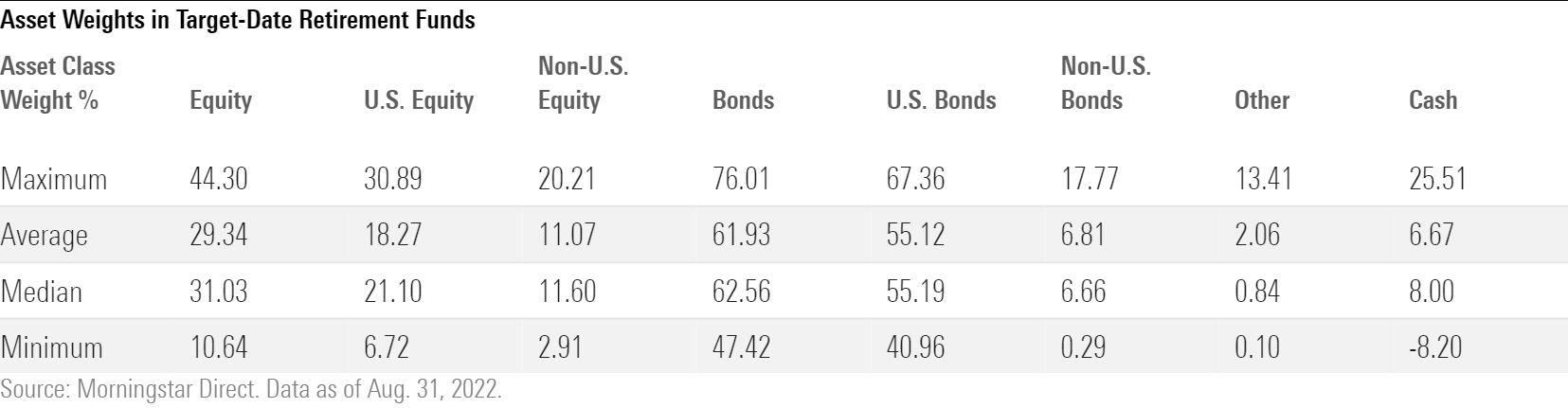

With those concepts in mind, we can look at the range of asset-allocation approaches in the target-date retirement category.

Morningstar

As you can see, asset managers construct vastly different retirement portfolios. While the typical target-date retirement fund devotes about 30% of assets to equity, the highest is about one-and-a-half times that level at 44%, while the lowest is about one third that level, at roughly 10%. Correspondingly, a common bond weighting is a bit higher than 60%, but the high is more than three fourths bonds at 76%, and the low is less than half bonds at 47%. Finally, the typical fund in the target-date retirement category has about 7% or 8% in cash, but some hold more than 25% in cash, and a couple have negative cash exposures—which we can think of as no standard cash holdings. Note that most of these funds have negligible holdings in "other" assets, although one exception to that proves notable.

The Impact of Equities Overall and Different Bond Exposures

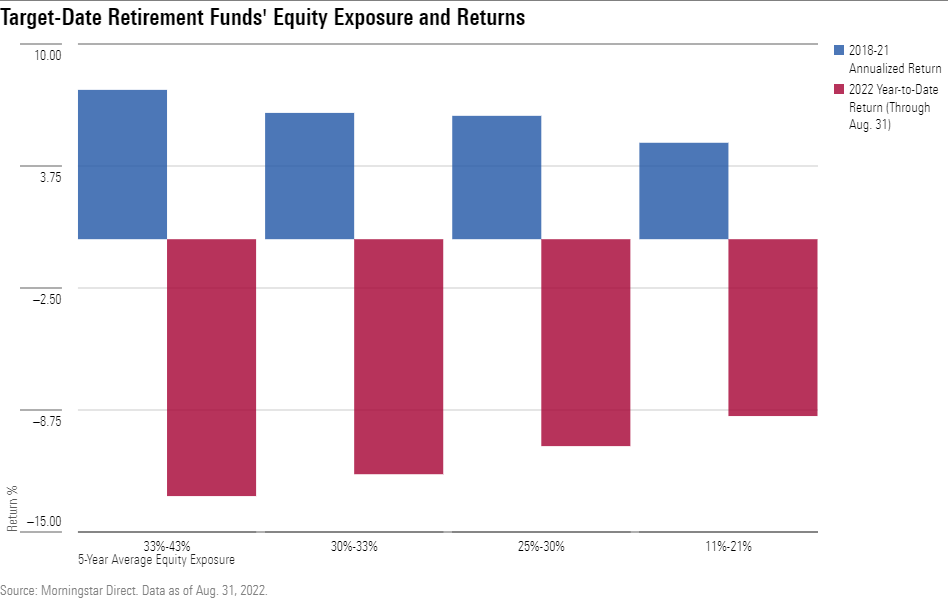

The returns of equities tend to be powerful enough that their weightings will drive overall returns for a mixed-asset portfolio—especially in strong rallies such as 2018 through 2021 and bear markets like the one in 2022. The disparities in equity weightings in target-date retirement funds show this clearly—and why equity weight is a key consideration for retirees.

We averaged the overall equity weight for each of the 31 target-date retirement funds with five-year histories and plotted those funds' returns from the beginning of 2018 through the end of 2021 as well as for the first eight months of 2022. Exhibit 2 then groups the category into four segments according to average five-year equity weight.

Morningstar

From 2018 to 2021, funds with higher equity weightings posted higher total returns on average. Those with 33% to 43% equity averaged 7.7% annualized; funds with 30% to 33% equity averaged 6.5%; funds with 25% to 30% equity averaged 6.3%; and funds with 11% to 21% averaged 4.9%. The inverse has also been true, arguably more dramatically. In the first eight months of 2022, those four groups of funds, in the same order, fell 13.2%, 12.0%, 10.6%, and 9.1%. Investors who have little need or desire to risk their capital would be wise to steer toward lower equity in retirement; those pushing for higher overall returns must accept the risk of capital losses.

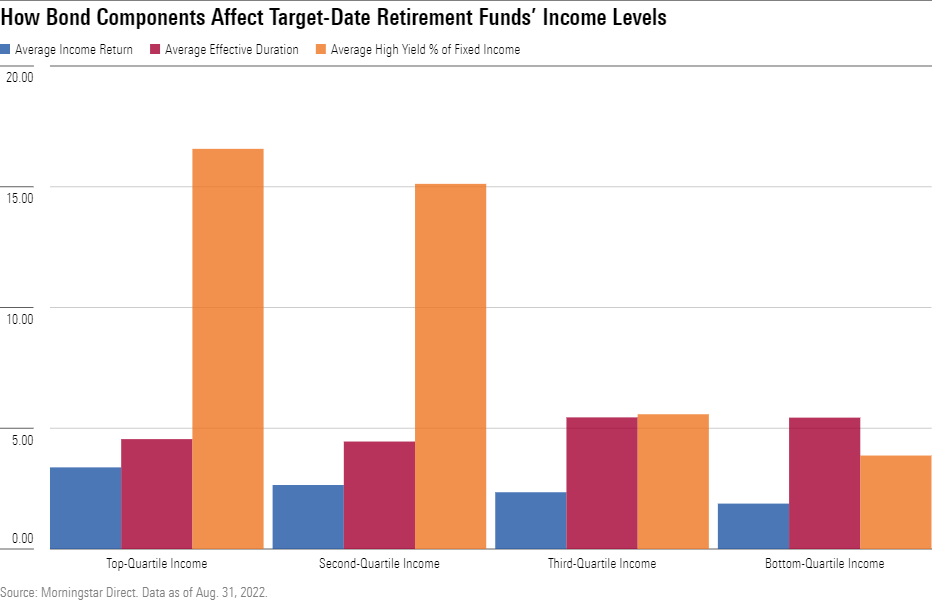

In order to examine how target-date retirement funds handled the challenge of providing income for spending, we reversed the field. We looked at overall income levels over the past five years and then examined how the funds' bond statistics explained those yields. We divided the target-date retirement funds into quartiles using their average income returns over a five-year period (2017-21). Then we looked at duration and credit quality from a number of angles, with the percentage of high yield proving to be most meaningful.

Morningstar

In some fixed-income environments, the maturity of a bond and its interest payments matter a great deal. That is, sometimes longer-dated bonds provide meaningfully higher returns than short-term bonds of similar credit quality. In those regimes, an income-generating portfolio could hold longer bonds in order to generate more income. As you can see above, however, that hasn't been the case recently. In fact, funds with the highest income levels have shorter overall durations than those with lower income levels. (Of course, now that interest rates have moved up considerably, that might change going forward.)

The most meaningful difference in income among target-date retirement funds in recent years was the amount dedicated to high-yield bonds in their fixed-income sleeves. The quartiles of funds that generated an average yield of 3.4% and 2.7% devoted an average of 16.6% and 15.1% of their fixed-income portfolios to high-yield bonds. The quartiles of funds that yielded an average of 2.4% and 1.9% held just 5.6% and 3.9% of their bond sleeves in high-yield bonds. Clearly, the disparity is high and significant.

Overall Risk and Reward for Retirement Funds

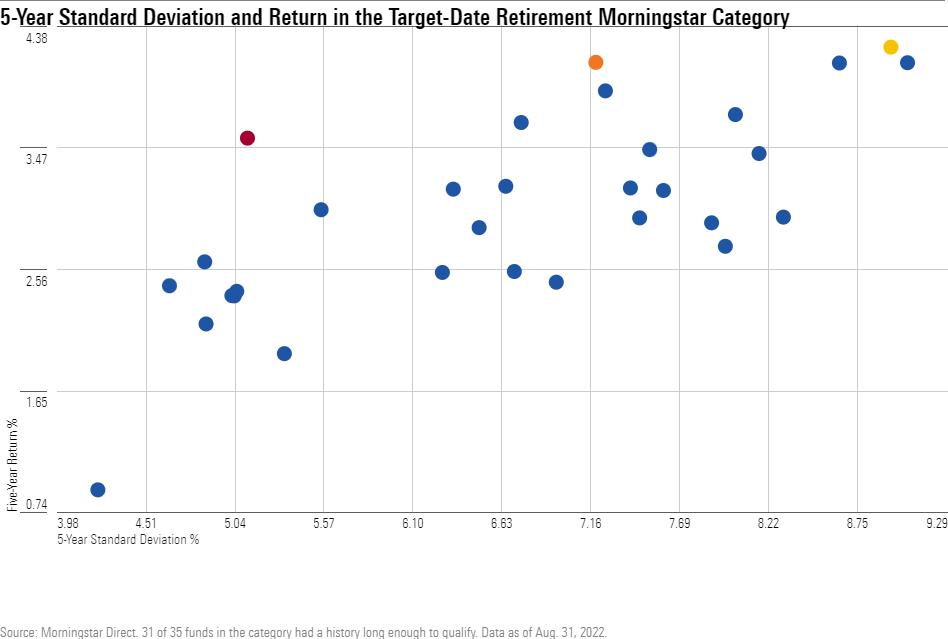

Now that we have examined the fundamental sources of risk and reward, we can look at results. Below we show five-year standard deviation and five-year returns to provide a broad overview of the risk/reward trade-offs in the space. Here are the 31 funds in the category that have enough history (as of Aug. 31, 2022):

Morningstar

Higher risk generally means higher returns, with three fairly clear groupings by volatility: funds with standard deviations from 4% to 6%, 6% to 8%, and more than 8%. Within each group there's a standout with higher returns; we'll take a closer look at those three funds below.

Among conservative funds, with a five-year return of 3.5% and a standard deviation of 5.1%, the standout (in red) is Dimensional Retirement Income TDIFX. This member of DFA's target-date series, which earns a Morningstar Analyst Rating of Neutral, devotes just 20% of assets to equities and completely avoids high-yield bonds. That stance certainly limits its growth potential and drives an average income rate of just 2%, which would be too low for the plans of some retirees. On the other hand, its 7.2% drawdown in 2022 through Aug. 31 was the second-lowest in the 35 funds in the category—and a key part of the reason its longer-term returns stand out. It's the type of fund built for investors with a significant nest egg, relatively modest income requirements, and a distaste for negative returns.

In the group of funds with midlevel volatility, Prudential Day One Income PDAJX has posted the highest five-year return (in orange). This unrated fund's 4.1% annualized gain and 7.1% standard deviation make sense given its asset allocation. It has historically devoted just less than 30% of assets to equities—the middle of the road within this category. It also stands out in a couple of ways. First, of the 54% it dedicates to bonds, only about 3% of its fixed-income assets go into high-yield fare; it's not stretching for yield. Second, its 10% "other assets" weighting is the highest in the category. That comes largely from a 5% holding in a commodities portfolio, which gained more than 25% in 2021 and has so again thus far in 2022. That's partly why the fund has only retreated 9.2% in the first eight months of 2022. Funds like this aim to entice a broad group of retirees by striking the right balance between growth and protection.

Finally, among the more volatile group of funds, Pimco RealPath Blend Income PBRNX has a five-year return of 4.2% (in yellow). Keep in mind that this member of Pimco's Gold-rated RealPath Blend Target Date suite also has the second-highest standard deviation at 9.0%. Its 44% equity stake is the highest in the category, and its high-yield weight of 16.6% sits in the heaviest quartile. This composition has produced more income than most peers; only two rivals have five-year average income returns above its 3.6% figure. That said, the strategy had the steepest losses in the category through the first eight months of 2022 at 14.6%. Pimco RealPath Blend Income is the type of fund designed for aggressive investors who seek to maximize income and can handle losses in the inevitable equity downturns. For that group, if used properly, it does what it's built to do.

Investors trying to cobble together a game plan should reflect on the following:

- What are your needs and preferences regarding capital preservation? Many bear markets see equities drop 30% or more. Are you able to handle that type of drawdown on 25% of your portfolio?

- What kinds of growth levels will make you comfortable? The longer you believe you'll live, and the more resistant you are to cutting spending in retirement, the higher the equity weight you'll need.

- What income requirements do you have? Some with large nest eggs can handle the lower, more secure yields that come from a 100% high-quality bond portfolio; others will need or want higher income levels.

If these sound like difficult decisions, it's because they absolutely are. Being thoughtful and understanding your priorities can help you to come to the most helpful conclusions. The good news here is that target-date retirement funds are not one-size-fits-all solutions. The range of different allocations and suballocations means that if you focus a bit on fundamentals—portfolio composition—you have a solid chance of finding the mix that suits your preferences and needs.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/984ff87e-463c-4fca-8c15-ebbf7f9593b2.jpg)