Where to Invest in Bonds in 2024

Interest rates are projected to fall further, bolstering returns for longer-duration bonds.

/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)

Key Takeaways

- Investors will be best served in longer-duration bonds.

- Long-term interest rates are projected to decline further.

- The Federal Reserve will begin cutting rates, possibly as soon as March.

- Corporate credit spreads provide an adequate margin of safety for downgrade and default risk.

The Bond Market Rebounds in 2023

Following the worst bond market ever in 2022, fixed-income markets have largely normalized and rebounded in 2023. For the year to date, fixed-income returns are positive, with those bonds that trade with a credit spread having performed better than U.S. Treasuries.

Through Dec. 5, the Morningstar US Core Bond Index, our proxy for the broad bond market, increased 2.77%. The return was supported by a combination of underlying yield carry and tightening credit spreads, slightly offset by an increase in long-term interest rates.

Returns for Morningstar's U.S. Fixed-Income Indexes

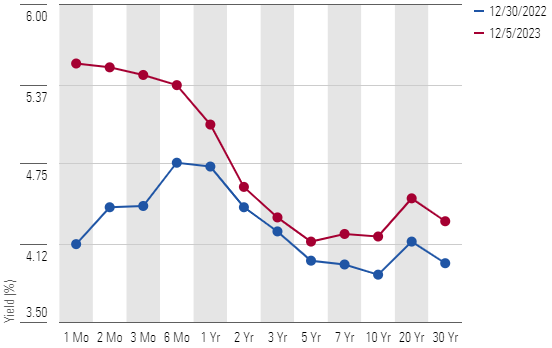

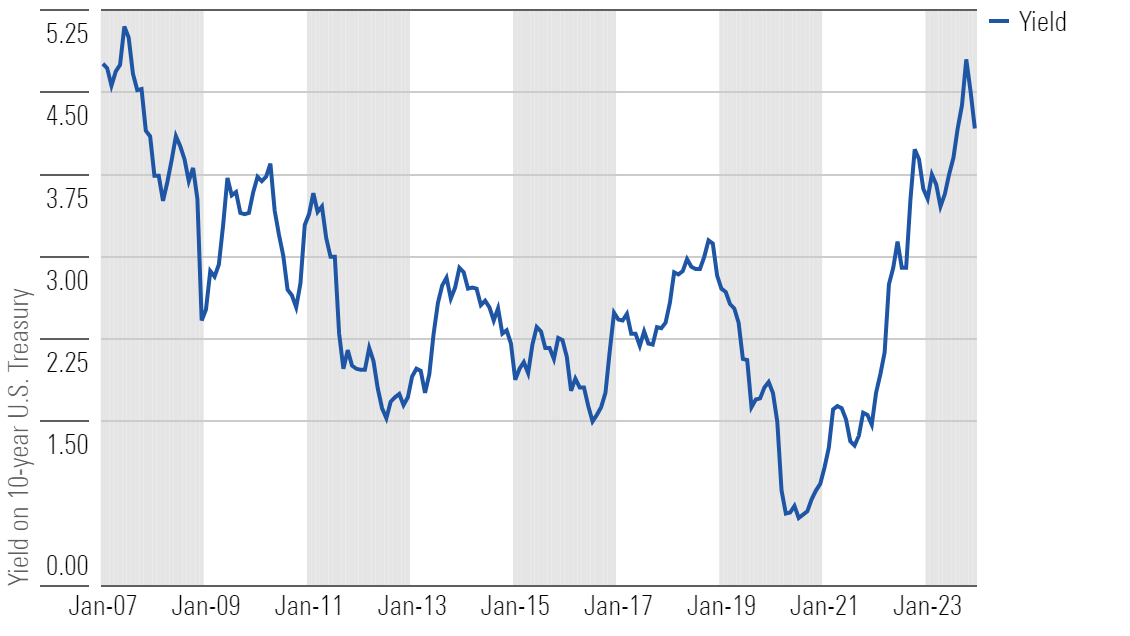

Throughout 2023, the yield curve became further inverted. Short-term interest rates rose as the Federal Reserve hiked the federal-funds rate, reaching a range of 5.25% to 5.50% after starting the year at a range of 4.25% to 4.50%. High inflation, quantitative tightening, and other technical factors drove the yield on the 10-year U.S. Treasury up to 4.18%, a 30-basis-point increase from where it began the year.

U.S. Treasury Yield Curve

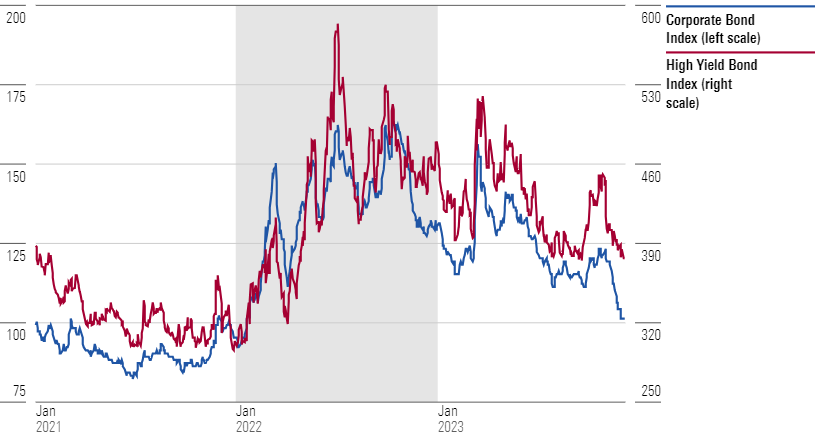

Bonds that trade with an additional credit spread over equivalent maturity U.S. Treasury bonds performed the best thus far this year. For example, the Morningstar US Corporate Bond Index (our proxy for investment-grade corporate bonds) rose 5.49% and the Morningstar US High-Yield Bond Index rose 10.14%. The reason for the outperformance was twofold. First, those bonds provide a higher yield to compensate investors for the risk of credit rating downgrades or defaults. Second, credit spreads tightened over the year.

Through Dec. 5, the average corporate credit spread of the Morningstar US Corporate Bond Index tightened 29 basis points to plus-101. The average corporate credit spread of the Morningstar US High-Yield Bond Index tightened 103 basis points to plus-376.

Average Credit Spread of the Morningstar Corporate Bond Indexes

Outlook for Investing in Bonds in 2024

After starting the year recommending that investors focus on the middle of the yield curve, we began to advise investors to lengthen their duration in our midyear bond market update. According to our forecasts, we continue to think investors will be best served in longer-duration bonds and locking in the currently high interest rates.

At the short end of the curve, we expect that the Fed will shift course and begin to ease monetary policy in 2024 by lowering the federal-funds rate. This forecast is based on the combination of our projections that inflation will continue to moderate and that the rate of economic growth will slow.

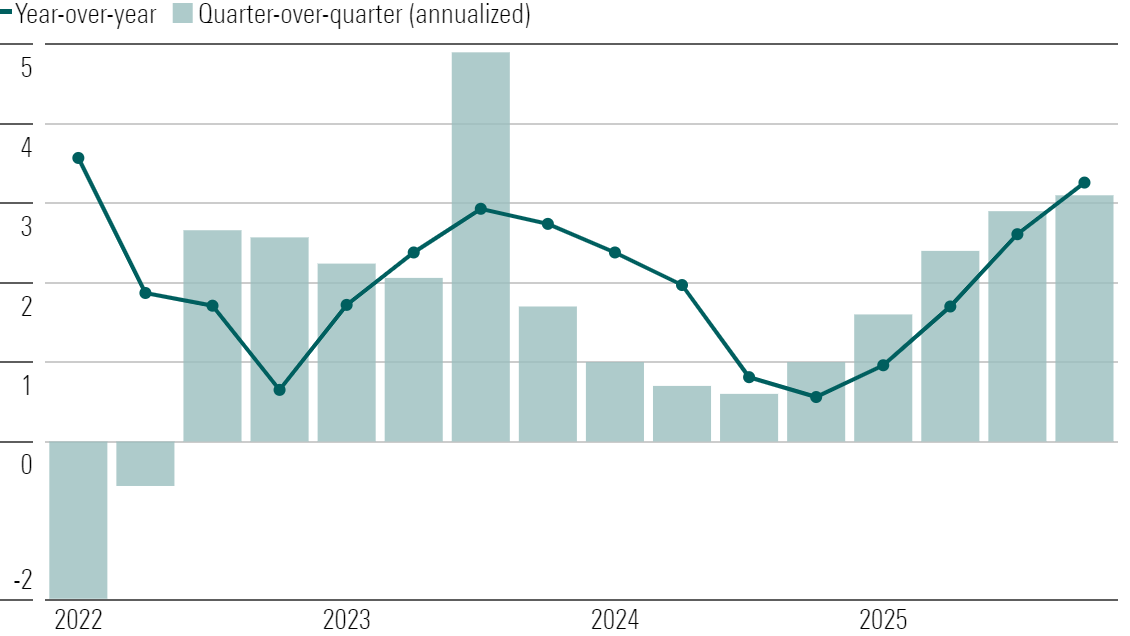

From the pandemic-induced shift in consumption patterns to supply chain disruptions to geopolitical events, inflation rose higher than anyone expected in 2022. Inflation has been steadily subsiding in 2023, and we expect that trend to continue. Looking forward, the conditions that spurred inflation higher have largely been normalizing. We project the deflationary forces in those specific categories will slow the overall inflation rate substantially.

Inflation Forecast as Measured by the Personal Consumption Expenditures Price Index

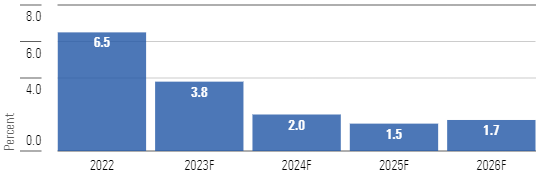

Tight monetary policy and currently high interest rates will take their toll on the economy. While our base case remains that there will be no recession, we do expect that the rate of economic growth will slow. We are forecasting that real gross domestic product will decelerate to a 1.7% annualized rate in the fourth quarter of 2023 and continue to slow sequentially each quarter until bottoming out in the third quarter of 2024. We then forecast the rate of economic growth will climb throughout 2025.

Morningstar’s Quarterly Forecast of Annualized Real GDP Growth

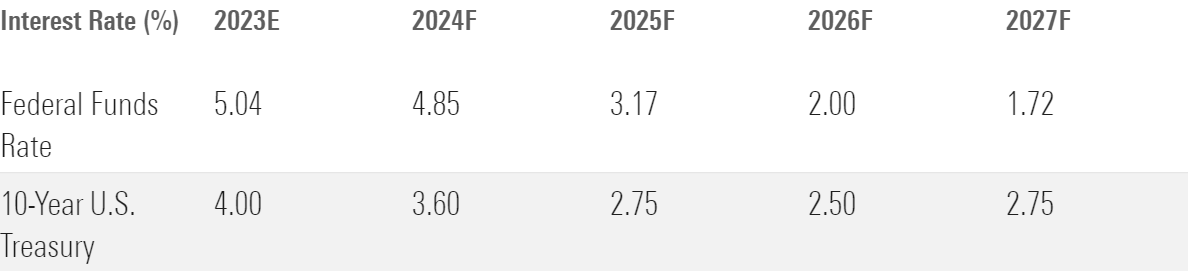

We forecast that the Fed will lower the federal-funds rate at its March 2024 meeting and continue to cut rates further to approximately 3.75% by the end of the year. We further project that the Fed to continue cutting rates, dropping to 2.25% by the end of 2025. While short-term rates are currently high, those rates will decline in relation to the federal-funds rate, and as short-term debt matures, investors will be left with the option to reinvest in lower rates.

Morningstar’s Interest Rate Projections, Annual Average

At the longer end of the curve, we project that the yield on the 10-year U.S. Treasury will decline and average 3.60% in 2024. We project the yield will decline even further in 2025 and average 2.75%. As interest rates decline, investors will not only earn the currently high interest rates but will also benefit from additional price appreciation on bonds with longer maturities.

Yield on the 10-year U.S. Treasury Bond

The Corporate Bond Market Outlook for 2024

In our 2023 bond market outlook, we noted that we saw value in the wide credit spreads that were offered by corporate bonds. Since then, corporate credit spreads have tightened and are now in a range that we consider to be fairly valued.

Over the first half of 2024, credit spreads could face pressure as the economy weakens, and the market may price in an expectation for additional downgrades and defaults. While our base case is that the rate of economic growth will slow over the first three quarters of the year, we do not expect the U.S. economy will slip into a recession. As such, we expect that downgrades and defaults will remain close to historically normalized levels. According to PitchBook, the default rate in the leveraged loan market was 1.48% in November 2023, compared with a 10-year average of 1.58%.

While the amount of extra spread provided on corporate bonds appears adequate based on our economic outlook, by no means are credit spreads cheap. Over the past 23 years, only 18% of the time has the spread on the Morningstar US Corporate Bond Index been below the current spread of plus-101 basis points. Over the same period, only 25% of the time has the spread on the Morningstar US High-Yield Bond Index been below its current spread of plus-376 basis points.

Bond Investing Ahead of the New Year

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)