Wage Data Shows the Bind Facing Investors and the Fed

Inflation may be peaking, but supply chain issues are creating even more unknowns than usual.

/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)

The latest inflation data highlight the tough spot that the Federal Reserve and investors are in: while the worst of the upward pressure on prices may be past, it’s proving stickier than many had expected and it’s hard to know exactly when it will start coming down.

That means continued uncertainty, the one factor almost guaranteed to cause volatility in the markets.

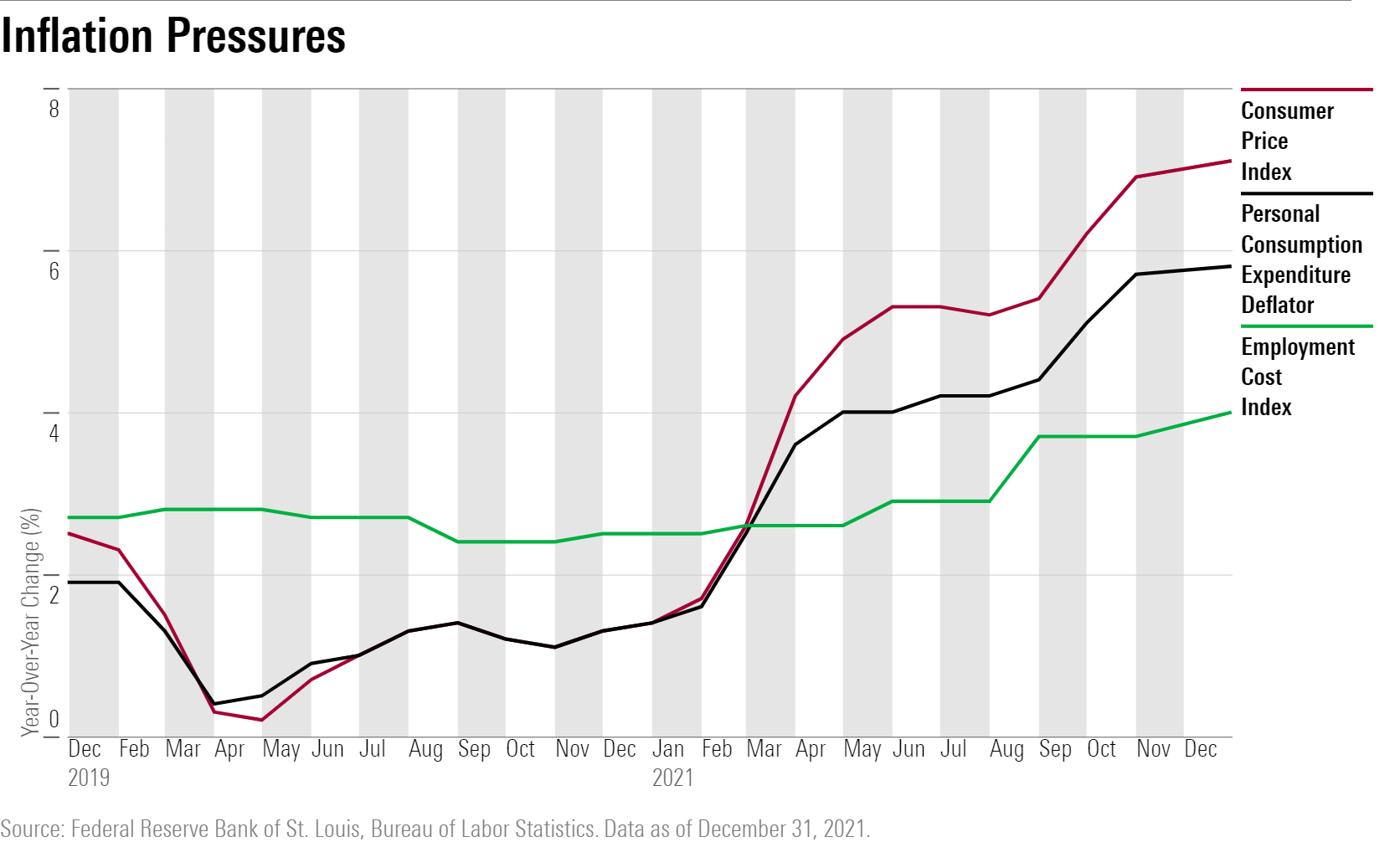

The Labor Department reported Friday that wages as measured by the employment cost index rose 4.0% during 2021, the fastest increase in two decades. While good news for workers, the abrupt rise in wages reinforces concerns about a "wage-price" spiral, where inflation for goods and services feeds upward pressure on wages, which in turn pushes inflation higher.

While bond and stock markets had a muted reaction to the latest data, the numbers fill out the picture painted by other recent reports, as well the outlook cited by the Fed in signaling that interest-rate increases are on their way very soon.

“Inflation has yet to cool off, and wage pressure also remains high,” says Preston Caldwell, Morningstar’s chief economist. “This supports the Fed’s almost certain move to hike interest rates in March.”

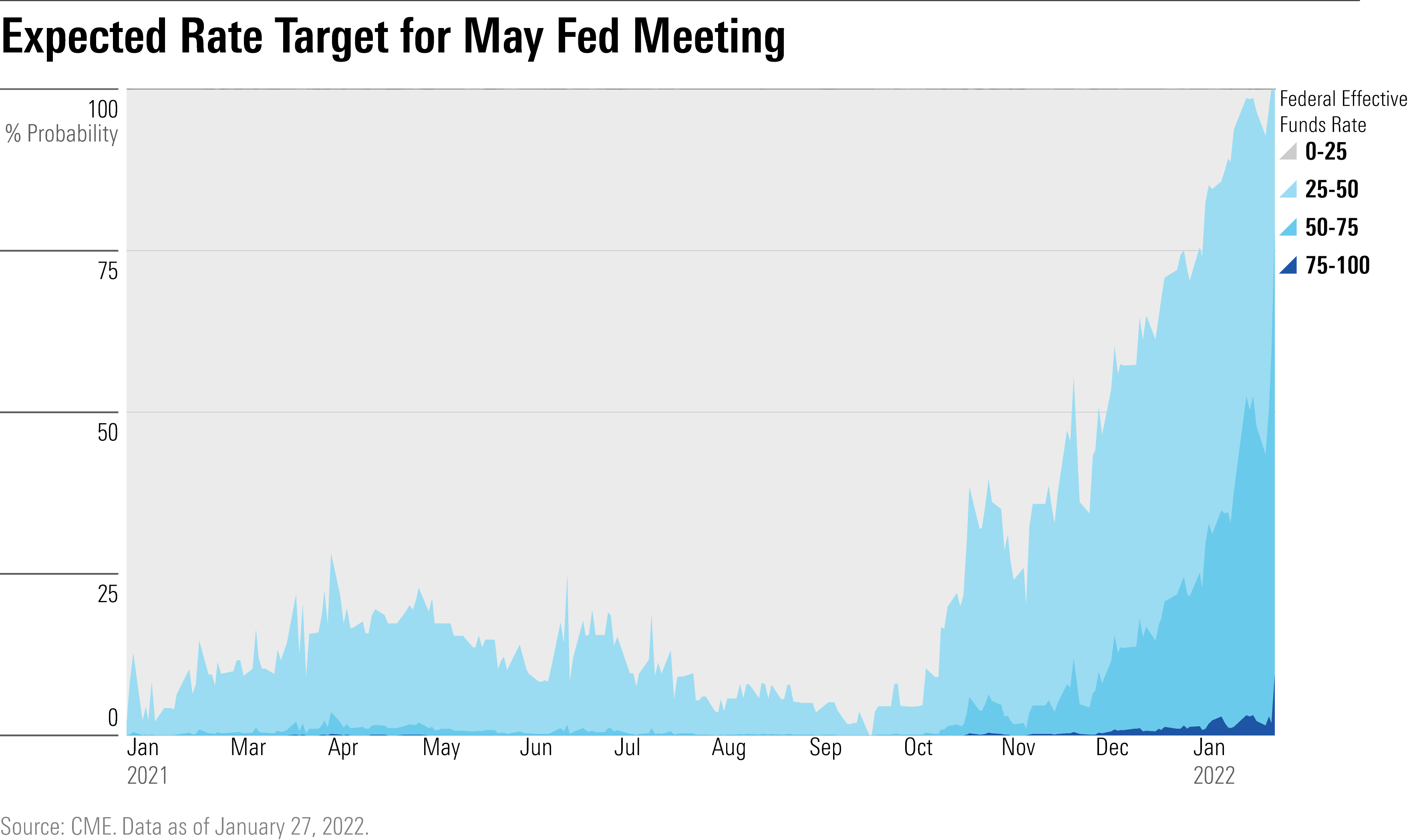

Interest-rate markets are predicting the Fed will boost the federal-funds rate by a quarter of a percent at their next policy meeting and ultimately hike four times in 2022. Not only are markets expecting an increase in March, but expectations are now at a nearly 75% chance for another rate increase in May.

Concerns about wage pressures are feeding into those Fed policy expectations.

Caldwell says it’s difficult to predict how wage inflation will play out in coming quarters, especially due to the impact of the omicron variant on the economy. However, “over the next one to two years, I don’t think we’re going to see an acceleration in wage growth from here. But I do think that wage inflation will remain above normal given the tightness of labor markets, putting modest pricing pressure in some industries,” he says. “This will be offset by deflation in durable goods and other areas as supply issues resolve.”

Caldwell noted that another economic report published Friday showed a steep 4% drop in personal spending on goods. At the same time, consumer spending on services continued to grow. "This represents a normalization of spending patterns, which if continued will provide immense relief to supply chains," he says.

Caldwell believes that in terms of the consumer price index, at 7% for the 12 months ending in December, likely reflects the peak with inflation expected to post a 3.6% increase for 2022. While down from 2021, that’s well above the Fed’s 2% target.

Alfonzo Bruno, associate portfolio manager at Morningstar Investment Management, says the problem facing investors is that the impact of supply chain issues makes it even more challenging than usual to assess the course of inflation, and what that means for Fed policy. “It’s very difficult to get a handle on the possible range of outcomes and where inflation will be at the end of 2022,” he says. “The range of outcomes is extremely wide.”

Bruno notes the Fed has already admitted it is behind the curve on fighting inflation given the rapid rise in prices, and that Chairman Jerome Powell pointed to increasing wages as a source of concern. The challenge, Bruno says, is that the Fed’s monetary policy tools focus on cooling off demand by raising interest rates, which makes it more costly to borrow money.

“But the Fed doesn’t have anything they can do about the supply side problem,” Bruno says. “They can’t just increase interest rates to 2% and expect semiconductors to be produced at a high rate. That’s why inflation expectations are being stickier."

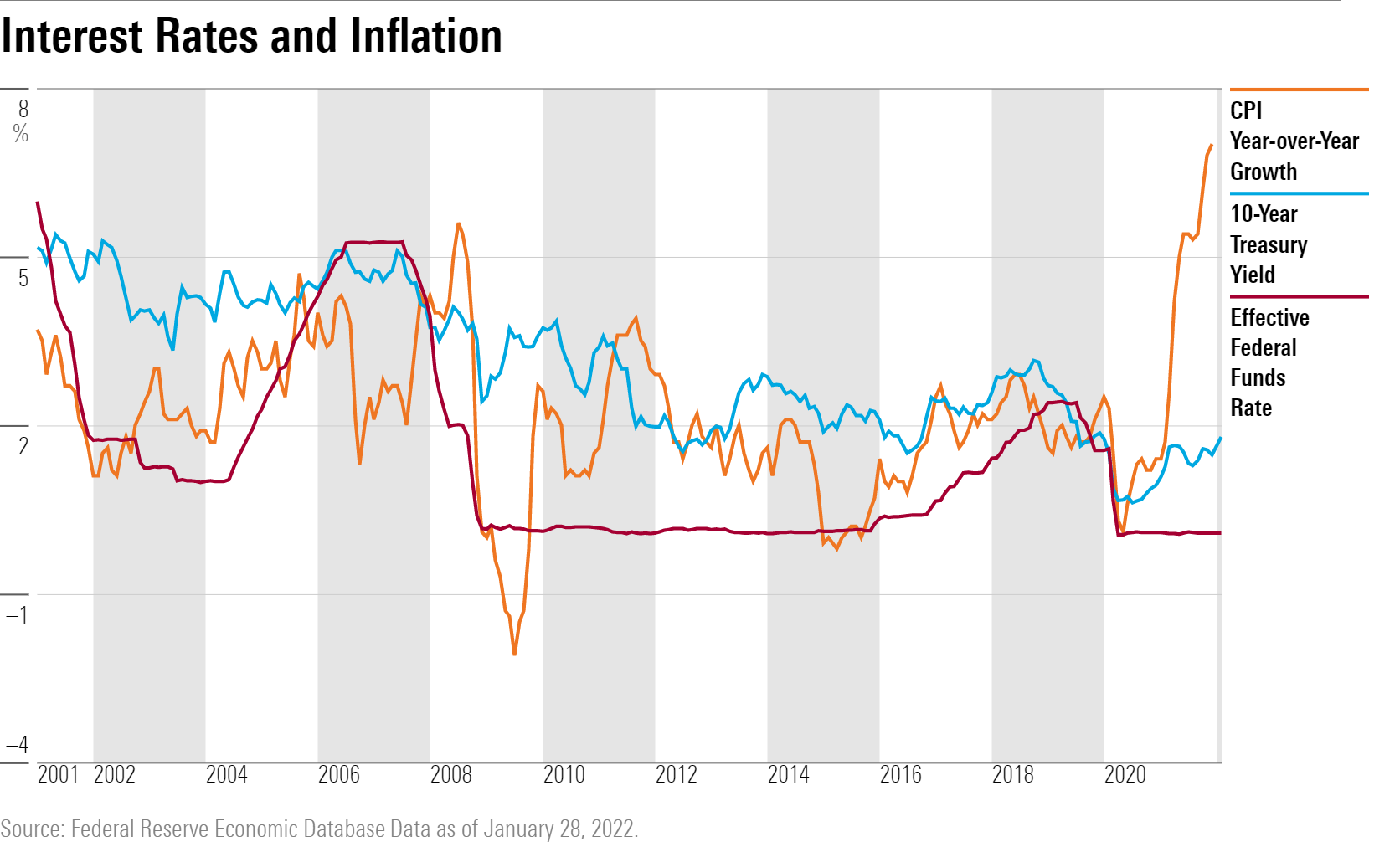

For the bond market, stickier inflation and the greater level of uncertainty around it likely means continued upward pressure on yields. That means favoring corners of the bond market that can be insulated from rising yields – such as floating-rate bonds. “That even means getting into the long-end of the Treasury market in the event that the Fed overtightens” and bond yields start to decline, Bruno says.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LDGHWJAL2NFZJBVDHSFFNEULHE.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed529c14-e87a-417f-a91c-4cee045d88b4.jpg)