Better Investing Opportunities Coming Your Way in 2023

5 new themes for portfolios, including bonds, China, and active management.

/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)

Better times for investors are coming in 2023.

That’s not to say there won’t be continued volatility or another leg down of the bear market in stocks or even an economic recession. But after the annus horribilis that was 2022, money managers and strategists say there are now more compelling opportunities to pick and choose from among different asset classes.

“The 2022 downturn has set the stage for a much improved long-term investing environment,” says Philip Straehl, global head of research at Morningstar Investment Management.

Among the themes worth watching in 2023:

1. At long last, a “stock-pickers” market?

2. Bonds are back.

3. A bull in China’s stock market.

4. Building back at home with infrastructure plays.

5. Emerging markets re-emerge as a winner.

5 Intriguing Opportunities

It is hard to imagine a more brutal year than 2022, which saw U.S. stocks enter a bear market, bonds down by double digits, and overseas investments walloped by the strong dollar.

Investors found few places to hide as inflation and rising interest rates wreaked havoc with even the most risk-averse portfolios. The popular 60/40 portfolio of stocks and bonds failed to provide protection. Even the passive indexing strategies that investors have come to favor were heavily skewed toward some of the worst-performing sectors of the year, technology and communication services among them, and extremely underweight the best-performing energy sector, leaving holders more exposed to risk than they might have realized.

On a positive note, the collapse of the FTX cryptocurrency exchange and the disruption in the cryptocurrency market did not lead to financial contagion and instability, nor did the meltdown in the U.K.’s gilt—or bond—market in late September. The latter involved leveraged bets on liability-driven investment derivatives by pension funds, which required rescuing by the Bank of England.

Heading into 2023, bearish sentiment among investors is at the highest it’s been since tracking such data started 35 years ago, says Paul Hickey, a co-founder of the independent investment research firm Bespoke Investment Group. The American Association of Individual Investors Sentiment Survey has been below its historical average every week this year, he says. “That’s never happened since the survey started in 1987.” From a contrarian’s point of view, that points to positive surprises.

“If you thought 2022 was eventful, 2023 promises to be an intriguing sequel,” says Hickey.

Now, investment strategists are more sanguine about a range of opportunities presenting themselves in the wake of the carnage, even though they remain clear-eyed about the continuing risks posed by inflation, interest rates, and a possible recession and about the need to be highly selective.

TARA, or “There Are Reasonable Alternatives,” is the new mantra, taking the place of TINA, the “There Is No Alternative” approach to investing. TINA had benefited stocks in the low-interest-rate environment that had dominated investing trends since the global financial crisis.

Return of the Stock-Pickers

With every passing market cycle of underperformance against index funds, the refrain of active managers of stock funds has been, “Wait ‘til next year.”

Unfortunately for investors in many actively run portfolios, it’s been a long wait.

Will 2023 finally be the year where stock-picking matters more than broad market performance?

Some strategists say that, with the markets expected to remain volatile and overall returns likely to be low, the time could finally be right for active management to have a positive impact on a portfolio.

Uncertainty surrounding the persistence of inflation and interest rates and the likelihood of recession will require investors be more selective about the regions, sectors, and individual stocks and bonds they pick than they have been in recent times, says Maria Vassalou, co-chief investment officer for multi-asset solutions at Goldman Sachs Asset Management.

That, she says, favors good old-fashioned stock-picking and active management styles rather than passive approaches.

“These opportunities may transcend the usual categorizations of value and growth or particular industries and instead be rooted in companies with effective operations and healthy balance sheets, regardless of sector or style,” says Vassalou.

“We are likely facing a market in the coming year that is less thematic,” says Jeremiah Buckley, portfolio manager for U.S. growth and income and balanced strategies at Janus Henderson Investors.

“Rather than broad groups of stocks leading based on general trends or factors, we believe relative performance will be more dependent on dynamics at the individual company level. In this market, innovation in products and services, effective capital allocation, and management’s ability to contain costs and gain productivity and utilize capacity at efficient levels will all be integral in determining companies’ growth,” he continues.

Under the hood, Wall Street consensus sees little earnings growth being generated by the stocks that represent the U.S. broad market, and many expect the market in 2023 to be flat at this time next year.

As David Kostin, chief U.S. equity strategist at Goldman Sachs Research, wrote in his 2023 investment outlook, there will be “less pain, but no gain” in 2023. Under that scenario, he advises investors to own defensive sectors—healthcare, consumer staples, and energy—that have low-interest rate risk. He also recommends stocks that benefit from decelerating inflation such as banks and pharmaceutical biotechs. Also, investors would do well to seek out stocks with resilient margins such as drugmaker Eli Lilly LLY and Lamb Weston Holdings LW, which makes frozen potato products for restaurant chains, as examples.

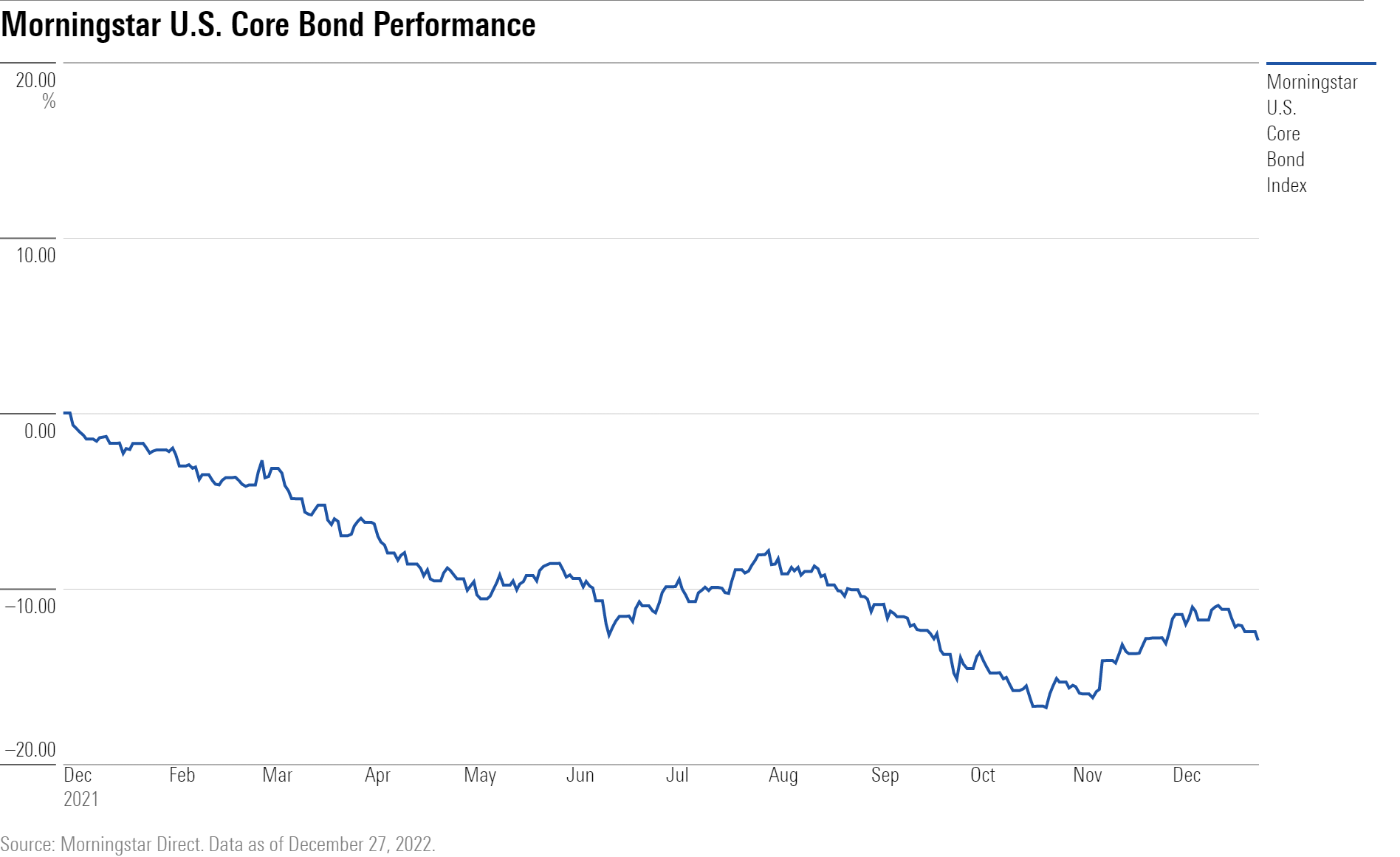

Time to Invest in Bonds

For bond investors, 2022 was the worst year in history. But now they’re back.

Bonds haven’t been this attractive since the 2008-09 period, says Morningstar’s Straehl, with yields on the 10-year U.S. Treasury at 3.67% recently, after rising to the 4% level for a stretch in October and November.

The higher yields in the wake of last year’s brutal losses in bonds now offer “meaningfully positive total return prospects after inflation—following an extended period of not keeping up with consumer prices,” says Straehl.

U.S. fixed-income markets, including U.S. Treasuries, corporates, and Treasury Inflation-Protected Securities, or TIPS, hold particular appeal for their improved risk/reward profile. And “major investment-grade bond markets are priced to deliver a return after inflation of 1.5%-2.0% over the next decade,” says Straehl.

Ken Leech, chief investment officer at Western Asset Management, also highlights the attractiveness of bond yields, especially amid deep investor pessimism that is reflected in widening spreads, or the difference between yields on corporate bonds and U.S. Treasuries of similar maturities.

“Despite yields on almost all fixed-income sectors being at one- or two-decade highs, investors continue to fear the worst,” he says. Concerns about persistent inflation and possible recession are making U.S. investment-grade credits appealing, particularly in the banking and energy sectors, he says. “Corporate fundamentals may have peaked, but they are coming off a strong starting point,” says Leech.

A Potential China Reopening Play

The reopening of the world’s second-biggest economy as its leadership eases restrictions after three years of zero-COVID lockdowns could give a tremendous boost to the country’s domestic growth and to economies worldwide as factories reopen, supply chains unsnarl, and Chinese consumers begin to spend more.

“China, after a hesitant start, will likely see much improved economic growth in 2023, while most of the world will be sluggish,” predicts John Vail, chief global strategist at Nikko Asset Management.

In recent weeks, China has shifted from a zero-COVID policy to a living-with-COVID policy. It most recently announced that, effective Jan. 8, it will drop the quarantine mandate imposed on overseas travelers entering the country, requiring only a negative result from a PCR (polymerase chain reaction) test taken 48 hours before departure. More incoming flights will also be allowed.

“Maintaining zero-COVID was increasingly intolerable,” says Olga Bitel, global strategist at William Blair & Co., a boutique investment management firm. “In the absence of growth, China’s GDP was 5% to 7% below what it would have been.”

In the past month, since China’s leadership started easing restrictions, the SPDR S&P China ETF GXC, which tracks an equity index based on the Chinese composite market, is up 11.5% at a recent $79.85. Still, it is off nearly 23% for the year to date.

Bitel notes there will be a global middle class of 250 million consumers who have been cooped up for three years who will be ready to travel and spend. “That is a non-negligible force,” she says.

At the same time, Bitel says a China reopening “further complicates the Fed’s job” as it could add to inflation pressures. Already, amid China’s moves, oil prices reached a three-week high in the final days of 2023.

Bridging Into Infrastructure Stocks

Another theme on the radar of many money managers and strategists are infrastructure investments, where the pandemic and its aftereffects laid bare shortcomings around the globe. Infrastructure assets are categorized as alternative investments and are private or public companies involved in developing or running physical assets, such as ports and airports, or providing energy supplies, such as utilities and oil and natural gas companies, transportation systems, and certain aspects of technology networks.

Russia’s war against Ukraine highlighted national security vulnerabilities in the energy sphere, and China’s lockdowns disrupted the flow of vital technologies. The major push to transition from traditional energy sources to renewables is another big driver of the interest in infrastructure assets.

New infrastructure projects will be at the center of efforts to create self-sufficiency in key areas such as increasing energy capacity in the United States and Europe, improving transportation and trade routes as countries reposition factories, enhance communication technologies, and expand electrification capabilities to meet climate goals.

Macquarie Asset Management names infrastructure as among its top three investment picks for 2023, along with fixed-income and agriculture.

“Infrastructure is a standout,” said Ben Way, group head of Macquarie Asset Management, in an outlook piece. “It offers inflation protection, defensiveness, high yield, and exposure to structural growth drivers, all of which should be attractive to investors in 2023.”

“Infrastructure should benefit from several macro drivers in 2023 and beyond,” according to a report by comanagers for ClearBridge Investments’ Global Infrastructure Strategies.

The managers call the U.S. Inflation Reduction Act of 2022, passed by Congress in August, “the most significant climate legislation in U.S. history.” They say, “We believe it will be industry transformative for utilities and renewables, in particular. We already see its impact in the 2023 capital expenditure plans of utilities, together with the forward-order books of companies involved in the energy transition, such as renewable, storage, and components suppliers, increasing their growth profile.”

Maria Vassalou, co-CIO of multi-asset solutions at Goldman Sachs Asset Management, notes the Biden administration’s “embrace of a more muscular industrial policy,” which uses tax incentives and subsidies to support vital domestic industries and infrastructure. She mentions the passage of the Chips and Science Act, signed into law in August, which provides support for microchip makers and advanced semiconductor technologies, as another example of the new policy of supporting critical industries to protect national security.

And the folks on Nuveen’s global investment committee highlighted public infrastructure investments as its highest-conviction preference in 2023, noting, “regulated utility revenue tends to be relatively decoupled from the economy and can experience growth from rising capital costs and policies related to energy transition and the Inflation Reduction Act. We also like midstream energy and waste investments for their growth and inflation-hedging characteristics.”

Emerging Markets for Added Diversification

Approaching 2023, the buzziest of all asset classes is emerging markets. It’s hard to find an investment manager not recommending some exposure to the group.

While U.S. stocks are a lot less expensive this year than last, that’s not to say they’re inexpensive, says Straehl of Morningstar. Bigger bargains can be found overseas, especially in the emerging markets, he says.

Vanguard’s Investment Strategy Group expects emerging-markets growth of 3.4% in 2023 that will “significantly outperform” developed-markets growth of 0.3%. And for the next decade, the Vanguard analysts expect returns from emerging markets of between 7% and 9%, 2.3% higher than U.S. equities.

Vanguard now expects emerging markets to deliver returns on a par with non-U.S. developed markets and views emerging markets as an “important diversifier in equity portfolios.”

Emerging-markets equities have a lower correlation with U.S. equities than developed ex-U.S. markets, the analysts at Vanguard note. The asset class is attractively priced for the first time since the pandemic began in early 2020 after declining by nearly 22% in dollar terms this year.

Morningstar’s Straehl says there is “significant opportunity within emerging-markets equity.” He expects the stocks to deliver inflation-adjusted returns of about 7% in the next decade and has upgraded the firm’s conviction level on the asset class to “Medium to High.”

Alastair Reynolds, portfolio manager for global emerging markets at Martin Currie, says there will be wide divergences in performance across the regions that comprise the emerging-markets class. India, he says, is set to deliver the strongest growth in the coming year on solid domestic demand. China, too, should see a pickup in domestic growth.

Reynolds says the asset class held up well at the country and sector levels during challenging times amid “significant changes” in investment conditions the past few years.

“We remain excited by the powerful combination of technology adoption, urbanization, and services sector growth that is evident in emerging markets,” he says.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MQJKJ522P5CVPNC75GULVF7UCE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZYJVMA34ANHZZDT5KOPPUVFLPE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/S7NJ3ZTJORFVLCRFS2S4LRN3QE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/ed88495a-f0ba-4a6a-9a05-52796711ffb1.jpg)