ARKK: An Object Lesson in How Not To Invest

There's a massive gap between reported total returns and investors’ actual results.

/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)

As my colleague Katherine Lynch recently reported, ARK Innovation ETF’s ARKK downward trend over the past few months, in the wake of its spectacular rise in 2020, has taken shareholders on a wild ride. Because the actively managed exchange-traded fund didn’t attract widespread popularity until late 2020, the returns most of its shareholders have actually experienced have likely been far lower than its reported total returns.

In this article, I’ll dig into more detail on how big the difference has been between the fund’s reported total returns and the results shareholders have actually experienced, as well as why poorly timed asset flows are the major culprit.

Why Investor Returns Often Lag Total Returns

As I’ve covered in previous articles, a fund’s investor returns (also known as dollar-weighted returns or internal rates of return) often differ from its reported total returns because of the timing of cash inflows and outflows. Reported total returns (aka time-weighted total returns) assume a lump-sum investment made at the beginning of the period, with no purchases or sales made during the interim. But because investors often buy and sell funds for various reasons, their actual results can vary significantly if, for example, they buy more shares right before a major downturn or sell shares and then miss out on subsequent gains.

In our annual “Mind the Gap” study, we estimate the gap between investors’ dollar-weighted returns and funds’ total returns. For the most recent 10-year period ended Dec. 31, 2020, we found that in aggregate, investors earned about 1.7 percentage points less per year compared with reported total returns because of mistimed purchases and sales. We also found that this gap seems to persist over time, although it varies for different types of funds.

But while investor return gaps aren’t unusual, ARK Innovation’s results are on a completely different scale.

How Wide Is the Gap?

To estimate how ARKK’s shareholders have fared, I looked at monthly asset flows since inception, as well as asset totals at the beginning and end of each period. I then used these monthly cash flows to calculate an internal rate of return, which measures performance for the average dollar invested in the fund. It’s important to note that various complicating factors make it difficult to pin down exact investor-return numbers for ETFs,[1] but the numbers below should be directionally accurate.

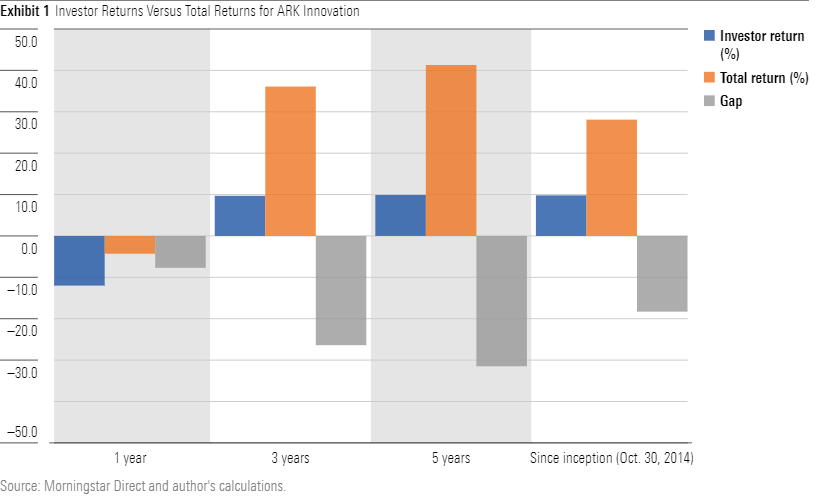

Note: Data as of Nov. 30, 2021. Investor returns are based on estimated monthly net asset flows and total assets as of the beginning and end of each period. Returns for periods greater than one year are annualized.

As the chart above illustrates, investors’ actual results lagged reported total returns over all four trailing periods--by large margins. Over the past five years, for example, the fund’s 41.3% annualized return places it among the top five best-performing U.S. equity funds and ETFs, and it trounced the S&P 500 (the benchmark listed in its prospectus) by more than 15 percentage points per year. After the adjusting for the timing of cash inflows and outflows, though, we estimate that investors earned less than a fourth of that return. ARKK’s estimated 9.9% investor return over the past five years lagged its benchmark by about 8 percentage points per year.

The investor-return gap hasn’t been quite as large over the past 12 months, but absolute performance has been considerably worse. We estimate that shareholders suffered a 12% dollar-weighted average loss, which is almost 3 times deeper than the fund’s 4.3% reported loss over that span. What’s more, ARKK has experienced breakneck volatility, making any risk-adjusted measure of its dollar-weighted returns even worse.

What Went Wrong

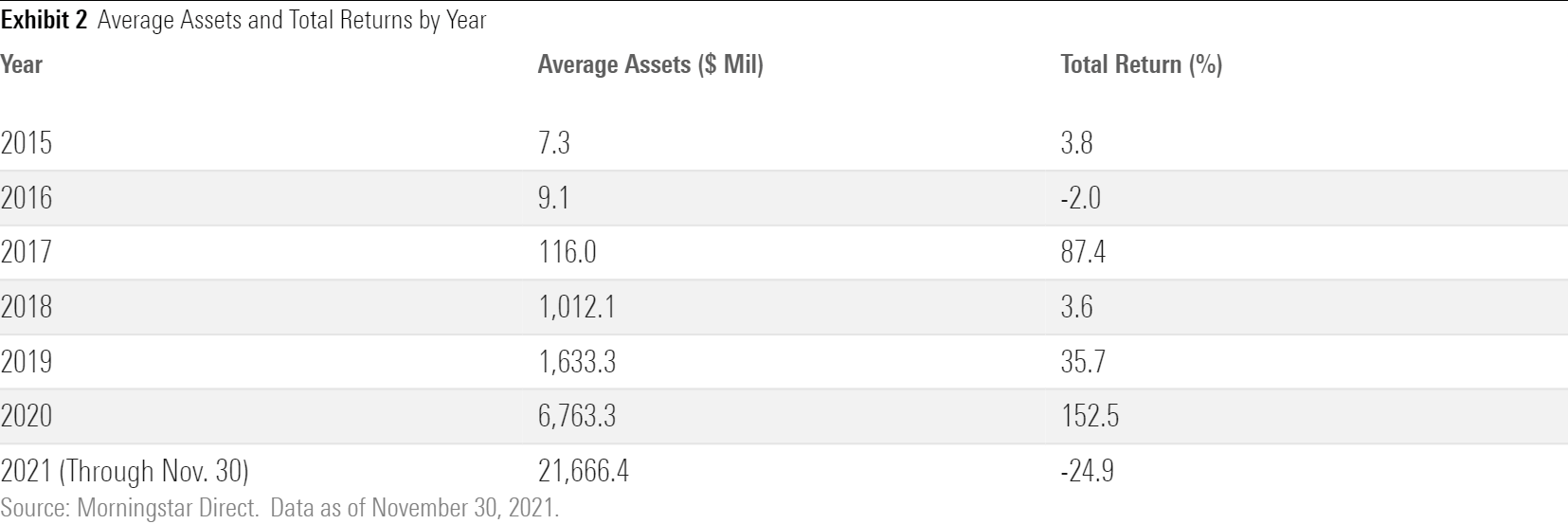

The difference between ARKK’s time- and dollar-weighted returns comes down to a simple reason: Most of its returns came when fewer shareholders were around to benefit from them. Even during 2017, when it posted an impressive gain of 87.4% (partly driven by a 1,300% runup in then-top holding Grayscale Bitcoin Trust GBTC), it averaged only about $116 million in assets. By the time assets peaked around $25.5 billion in June 2021, performance was just about to drop off. Previously high-flying holdings such as Teladoc Health TDOC, Roku ROKU, and Zoom Video Communications ZM have crashed back to earth in recent months, and the fund shed about 24.9% of its value for the year-to-date period through Nov. 30, 2021.

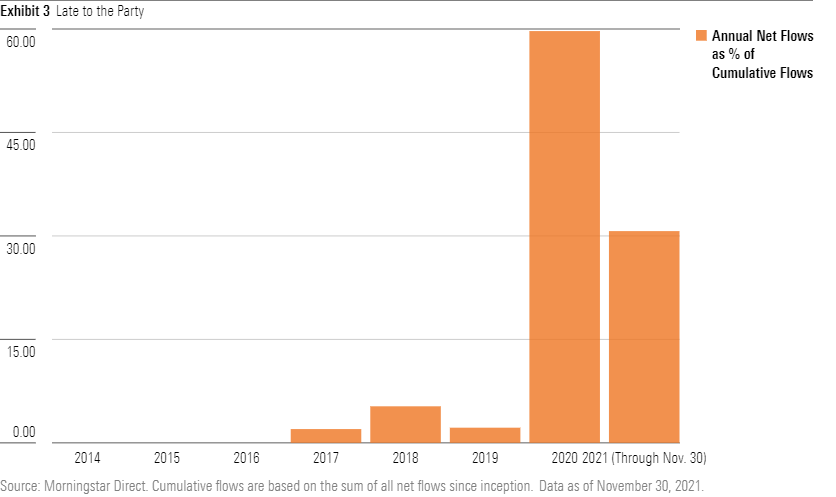

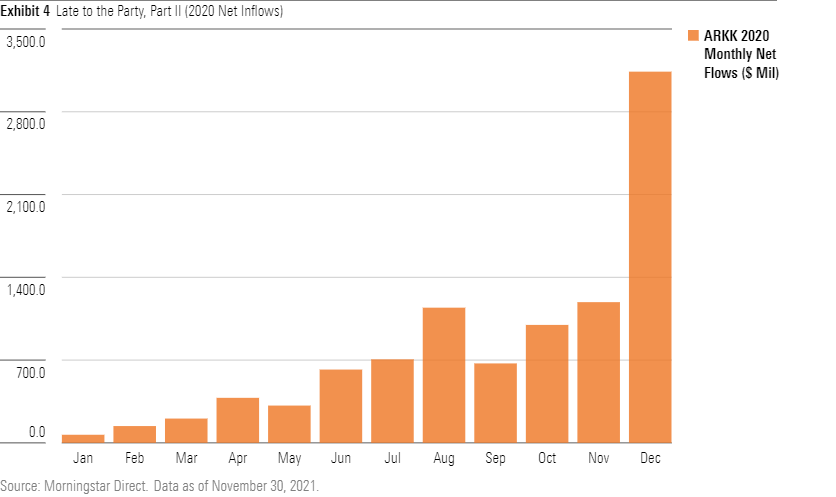

A look at the fund’s estimated net inflows year by year sheds more light on why shareholders’ results have lagged reported total returns by such a wide margin. As shown below, the lion’s share of ARKK’s net inflows took place during 2020 and 2021. Combined flows for those two years represent about 90% of all cumulative net inflows since inception.

What’s more, the spigot of 2020 net inflows didn’t really open up until late in the year; as a result, most shareholders who bought in during 2020 didn’t fully benefit from the fund’s triple-digit calendar-year gains. As shown below, more than half of all net inflows for 2020 came in during the last three months of the year. In fact, the fund’s $3 billion of net inflows in December 2020 made up about one fifth of all cumulative inflows since inception.

Glimmers of Light

To their credit, ARKK’s shareholders have not bailed out in droves as of this writing. ARK founder and portfolio manager Cathie Wood often emphasizes that she looks for stocks that can outperform over a five-year period, and some shareholders might have adopted a similar long-term perspective. We estimate that net outflows have totaled about $2.2 billion over the trailing six-month period ended Nov. 30, 2021. That’s a big number, but the majority of the fund’s shareholders have not abandoned ship. It’s also worth noting that even after adjusting for the impact of cash flow timing, investor returns are still in positive territory over most longer periods, albeit significantly lower than reported total returns.

In addition, we’ve previously written about potential liquidity issues related to the fund’s concentrated ownership positions in numerous portfolio holdings. Because the fund owns a significant percentage of the daily trading volume in many of its underlying holdings, this concentrated ownership could create a downward spiral of increased redemptions causing more selling pressure on key holdings, which in turn would worsen returns and lead to more redemptions. That’s still a potential issue, but the portfolio now has more exposure to larger, more liquid stocks than in the past, which should mitigate liquidity risk to some extent.

Lessons From the Flood

While ARKK’s story isn’t over, its latest chapter contains some lessons for investors.

- Triple-digit returns don't repeat. As we've pointed out in the past, it's highly unlikely for any fund to continue posting chart-topping returns year after year. Funds can typically rack up gains of 100% or more only by making concentrated bets on individual stocks in the market's hottest sectors, which usually means taking on nosebleed levels of valuation risk. That often leads to sharp losses when market trends reverse course and valuations drop to more realistic levels.

- Risk matters. On a related note, it's impossible to generate high returns without taking on high levels of risk. As I wrote in a previous article, ARKK's portfolio courts extreme levels of risk on almost every type of fundamental metric, including concentration, momentum, liquidity, valuation, and financial health. This high level of risk makes it imperative for shareholders to fully understand what they're getting into before climbing on board.

- Consider dollar-cost averaging. Dollar-cost averaging often gets a bad rap because it typically leads to lower total returns. That's because equity market returns are positive more often than not, so keeping any money on the sidelines is generally detrimental. But we've found that in practice, dollar-cost averaging can help improve investors' results because it helps enforce discipline and avoid the pitfalls of bad timing--namely, buying in after a huge runup and selling after a decline. That's especially true when it comes to highly volatile asset classes and funds, such as ARKK.

Overall, the gap between shareholders’ actual returns and reported total returns underscores the perils of getting caught up in the hype of funds with high-flying returns, which usually leads to disappointing results.

[1]There are various factors that make it difficult to calculate precise investor-return numbers for ETFs. For one, investors who establish short sales positions engage in create-to-lend transactions, and demand from these short sales registers as net inflows (at least initially) in the same way as demand from long buyers. Depending on the timing of purchases and sales, some of these short-sellers may actually experience positive investor returns.

Long demand from market makers who purchase ETF shares and/or associated options for the purpose of building inventory and/or hedging existing exposures can also have an impact on estimated net inflows and total assets.

Finally, many ETF trades are made on the secondary market. Because these secondary-market trades typically don’t prompt new share issuance, they’re not reflected in estimated net inflow figures.

/d10o6nnig0wrdw.cloudfront.net/04-29-2024/t_eae1cd6b656f43d5bf31399c8d7310a7_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/PKH6NPHLCRBR5DT2RWCY2VOCEQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/360a595b-3706-41f3-862d-b9d4d069160e.jpg)