Target-Date Funds Have Suffered Losses. What Should Near-Retirees Do?

Four questions investors should ask.

/s3.amazonaws.com/arc-authors/morningstar/2e13370a-bbfe-4142-bc61-d08beec5fd8c.jpg)

When markets drop significantly, target-date funds do too. They are not guaranteed investments, and most—especially those intended for younger investors—carry significant allocations to stocks. Those younger investors needn’t blink over even fairly big losses, because their very long horizons until retirement give them more than enough time to ride out the rough periods.

The story is a bit different for investors very close to, or just entering, retirement. Near-retirees are more prone to what’s called sequence-of-returns risk; investors in this group simply don’t have as much time to recover from a big hit to their nest egg, which could affect the sustainability of their savings through retirement or the level of income they are able to draw from it. It’s for this very reason that suites of target-date funds employ an asset-allocation glide path which reduces equity exposure and increases the fixed-income component over time, with the intention of cushioning any potential shocks that occur around the retirement date.

The most recent spell of market volatility has been the most sustained since the 2007-08 bear market. So it’s a good time to check in and ask whether near-dated target-date funds have been holding up their end of the bargain. To get at an answer to this bigger question, we can zoom in on a few more focused questions:

- What has the actual range of losses been?

- What accounts for those losses?

- How significant are these losses?

- Should investors be concerned or take any action in responses to losses?

What is the range of losses?

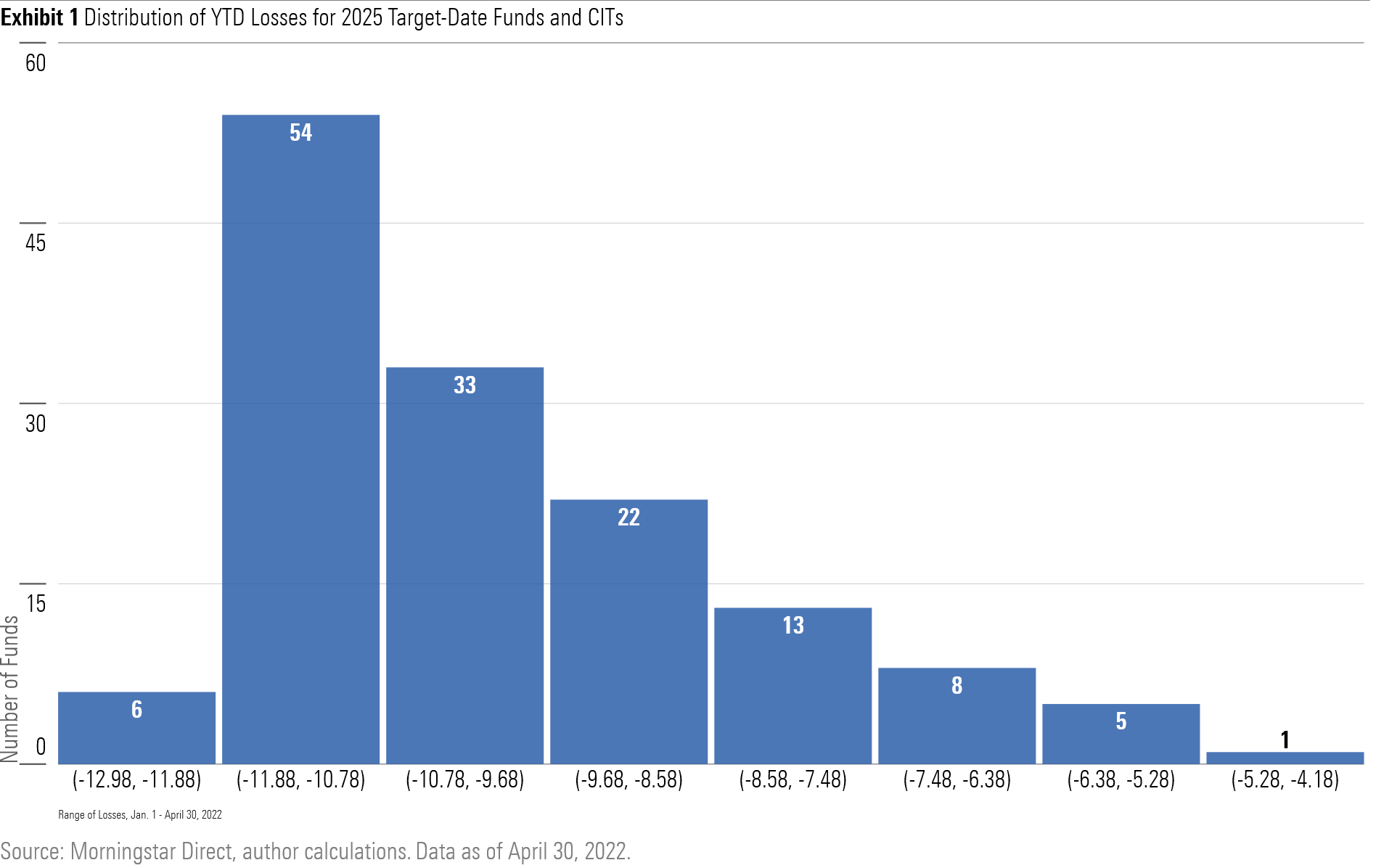

My analysis focuses on target-date funds with a 2025 vintage. In theory, those funds are intended for workers planning to retire in about three years, though in practice there is some degree of flexibility around the selection of funds, and investors in those funds could already be retired or some years further off from retiring. But given their intended profile, they should offer a significantly greater degree of cushion than funds with vintages 20 or 30 years later. I have combined funds from both Morningstar’s open-end mutual fund and CIT categories, as CITs have been a big area of growth for target-date funds in recent years. This gave me a robust sampling of 143 distinct funds with monthly returns available as of April 30, 2022. (Had I updated returns through May 31, 2022, the numbers would have been broadly similar and the trends consistent.)

The spectrum of returns (or, to be precise, losses, as every fund in the category was in the red through April) ranged from negative 4.33% for the best-performing funds in the category to negative 12.98% for the worst performer. This span of approximately 9 percentage points is fairly wide; when I ran the same exercise for 2055 funds, for example, the range of returns was only about 6 percentage points. It’s not surprising to find a greater degree of variance for the shorter-dated funds; asset-allocation philosophies tend to engender a much wider array of opinions and strategies for investors closer to retirement as opposed to the longest-dated funds, where equity allocations of 90%-plus are the norm and there tends to be a much tighter range of allocations. I will look into the differentiation among 2025 funds in greater detail in the next section.

It’s worth noting that the losses are not evenly distributed across the funds in the category. The median loss was negative 10.38%, and as Exhibit 1 illustrates, the preponderance of losses was in the negative 9.68% to negative 11.88% buckets. Only a half-dozen funds sustained losses of less than negative 6.38%. In a column earlier this week, John Rekenthaler also noted and elaborated upon this tendency of 2025 funds to produce similar losses.

What accounts for these losses?

This next question is more complex. Several factors come to mind that could plausibly contribute to divergent returns. Running a full regression on these factors would be the most “scientific” approach, but a project of that magnitude is beyond the scope of this article, and with only a few months of data to go on would not be likely to produce statistically significant results. Instead, I’ve looked for trends and correlations to see which of the hypotheses seem to have the strongest claims.

Equity Allocations

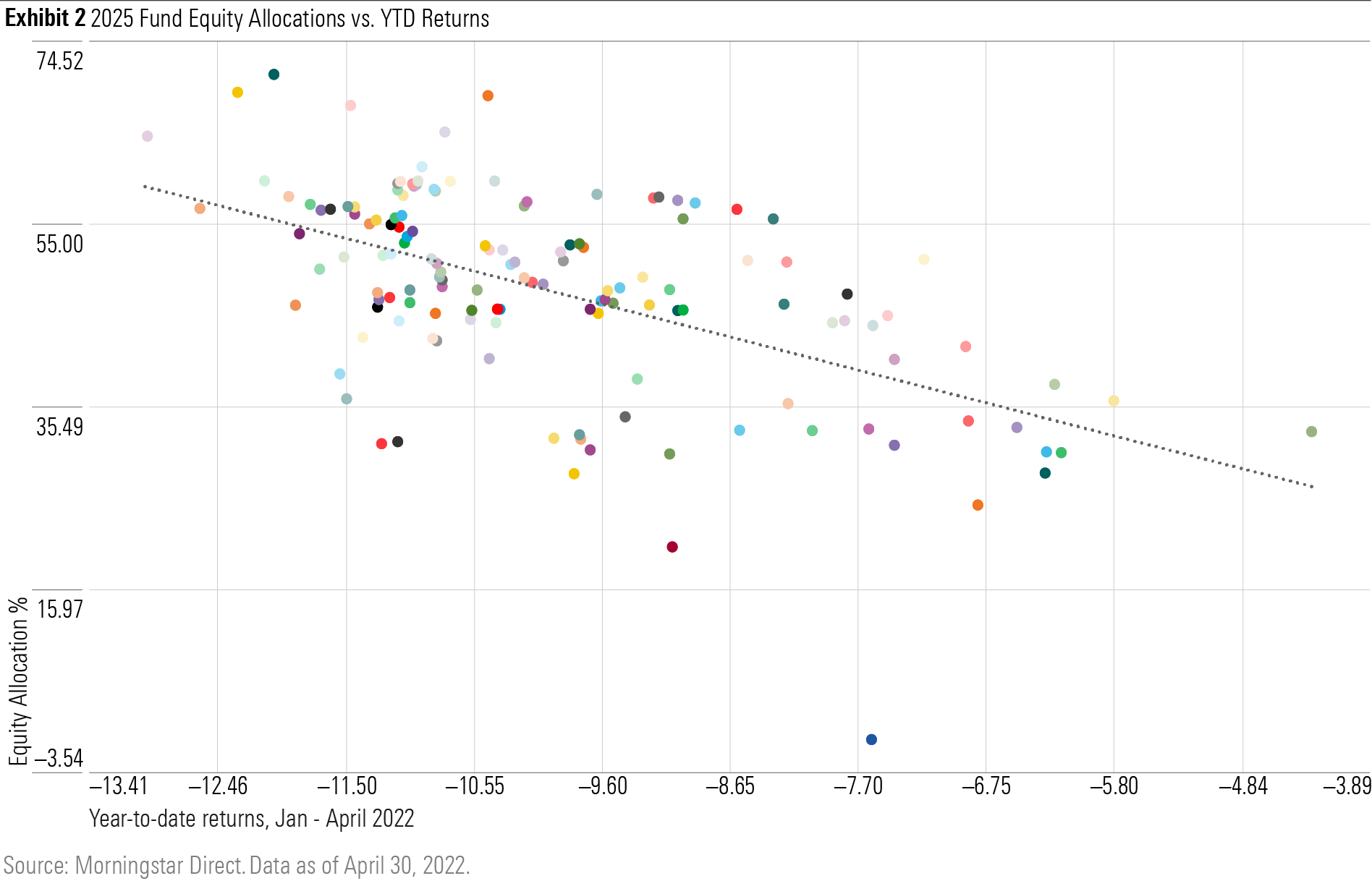

How much a fund allocates to stocks is the front-runner here. As I mentioned earlier, target-date providers tend to diverge philosophically the most around near-dated funds, and this is reflected in how much is allocated to stocks at different times throughout the asset-allocation glide path, which shifts the stock/bond mix as investors age. Some target-date architects believe the primary directive for investors close to retirement is to preserve capital, necessitating a significantly bigger stash of safer bonds; others, however, maintain that the demands of longer lives and potentially lower returns require a higher allocation to equities for longer periods.

Indeed, the degree of difference among strategic equity allocations (that is, the stated policy equity weights) for 2025 funds is eye-opening. The highest tops out at 75%, while the lowest bottoms out at 20%. The extremes are certainly far from the norm. The highest-equity strategies tend to be found in series labeled “aggressive,” usually from CIT providers who offer multiple risk options to plan sponsors, and those options tend to be lightly owned. The average equity allocation for the funds in my sample was 50%.

As Exhibit 2 shows, there is a detectable relationship between equity allocation and losses in 2022. In general, the higher the equity allocation (y-axis), the greater the losses (x-axis). There are, of course, some exceptions, but that general, expected pattern holds, and probably accounts for the lion’s share of explanatory power. Still, other factors can come into play.

Value versus Growth

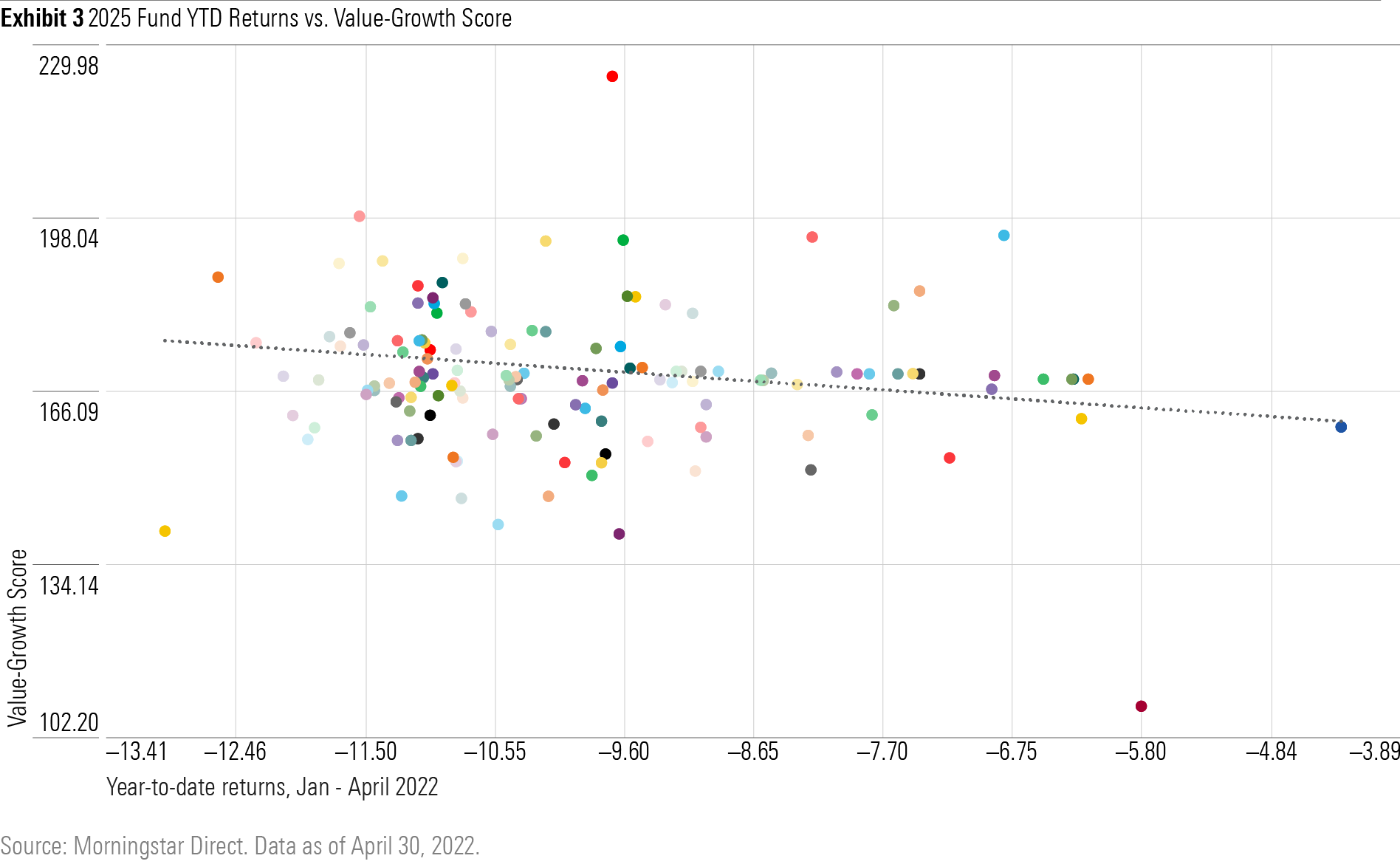

Another possible contributor could be style bias. After its long stretch of leadership, the growth style has retreated sharply relative to value over the past year, and the popular tech names that led the way have been among the hardest hit. The counter to this possibility, however, is that most target-date funds are structured to be widely diversified with minimal style biases. This supposition is borne out by the data.

When I plotted returns against the funds’ value-growth score (a Morningstar measure that assigns a score to how growthy or value-leaning a strategy is), there was no prominent trend and, moreover, most funds receive a value-growth score within a narrow band, so there is little variation among the funds. A few funds with particularly low scores (meaning they have a more pronounced value tilt) did produce narrower losses, and the value bias probably helped buffer losses. But for the most part, a target-date fund’s style does not appear to be a noteworthy contributor to return patterns.

Commodities Exposure

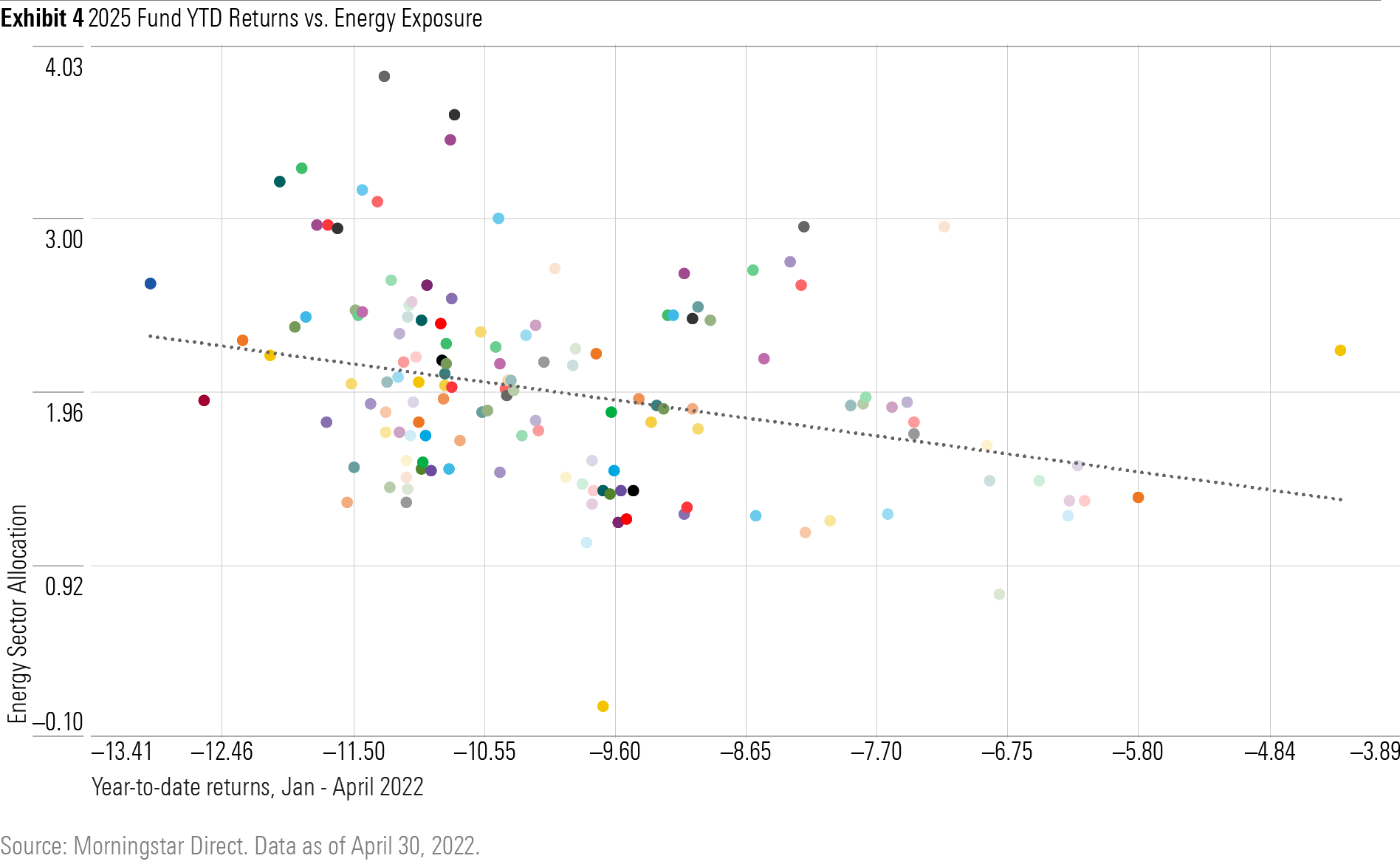

There’s one asset class that has bucked the trend during the recent down market, and that’s commodities. The combination of inflation concerns, constrained supply, and rising oil prices propelled the Bloomberg Commodities index up 31% for the year to date through April 30, 2022. Target-date managers tend to be cautious about investing in commodities owing to their volatility, but it stands to reason that any funds that made outsize allocations to commodities would get a boost, even at relatively small absolute weights.

The results turned out to be noncommittal or even contradictory to expectations. I looked at energy exposure in 2025 funds (the best available proxy for broader commodities), using both long exposure and long rescaled (which shows the energy exposure as a percentage of stocks as opposed to the fund as a whole). The long rescaled scatterplot shows little evidence of a trend. While the best-performing fund did have the highest energy exposure of nearly 7% of the equity sleeve, there were other funds with high energy weights that returned among the worst results. The straight long exposure is even more puzzling: The chart shows a slight downward slope, with higher energy weights clustering with bigger losses (Exhibit 4). My theory is that funds aggressive enough to take larger commodity or energy positions are also likely to have larger relative equity weights, which as we have already seen is correlated with steeper losses.

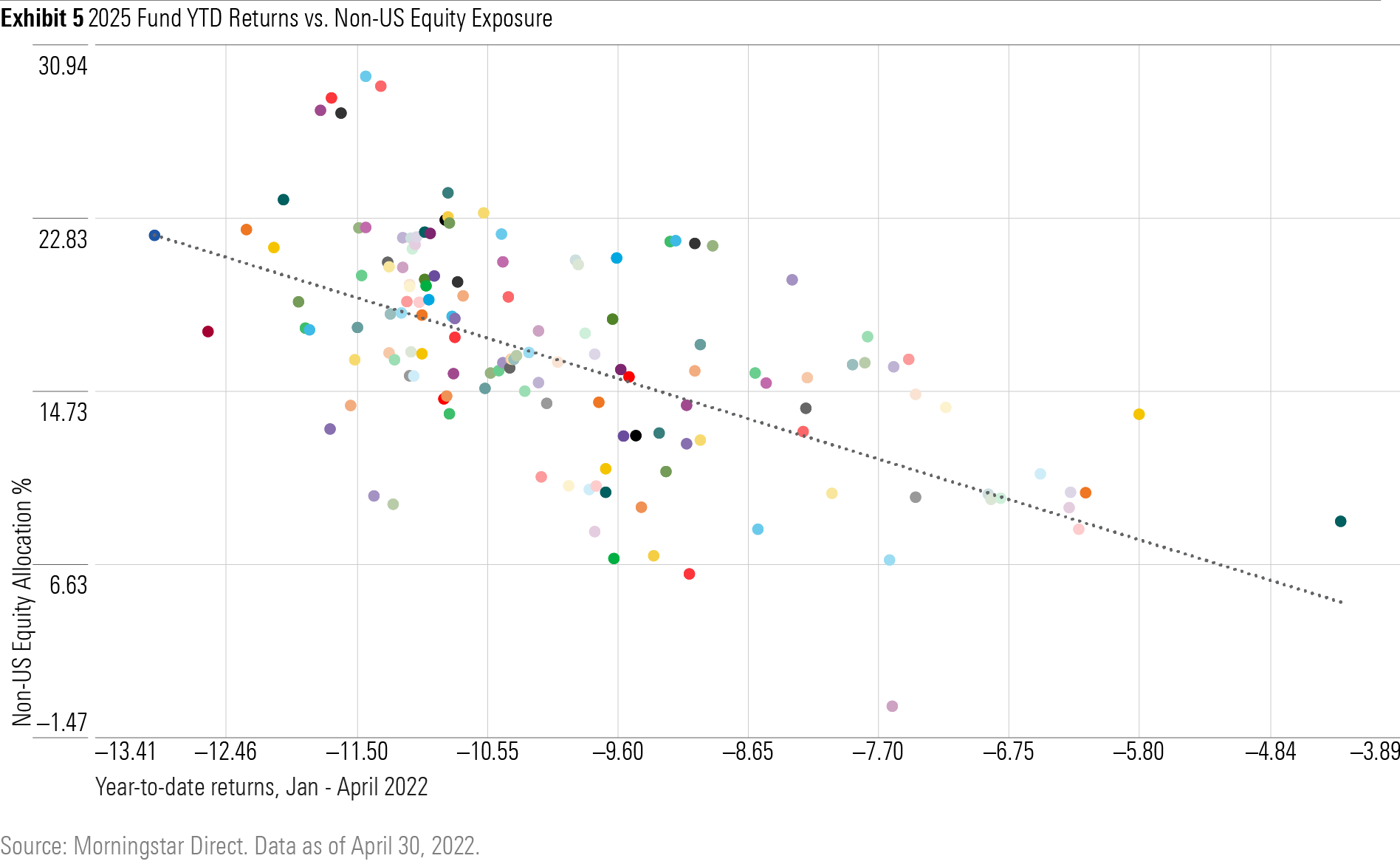

International-Equity Exposure

My first inclination was that international-equity exposure would not be a great differentiating factor, because while overweighting U.S. stocks has in general been a winning strategy over the past decade, losses for developed-market indexes in 2022 have been relatively close between U.S. and non-U.S. markets. However, the data proved my hypothesis wrong, as there is a clear trend of greater non-U.S. equity exposure leading to greater losses. Some of this, to be sure, is simply the correlation of higher non-U.S. exposure to higher equity exposure overall. Some of the effect may also be owing to managers’ allocating more to underperforming international countries or regions, or to shifts to more-defensive equities within U.S. stock sleeves.

Active Manager Risk

A final factor to note is the risk that a target-date fund filled with active managers will have some that simply outperform. This can be magnified in more-concentrated portfolios, even more so if the target-date series has an equity-heavy glide path. To take one example: Nationwide Destination 2025 features a 27% allocation to Nationwide Multi-Cap Portfolio, a multimanager, actively run portfolio that is intended to beat the broad Russell 3000 benchmark. So far in 2022, though, the fund has trailed its bogy by several percentage points. This is not to pick on Nationwide, or to make a statement about active versus passive, but simply to underline that on the margins actively managed underlying funds can affect performance (on the upside as well) in ways that aren’t always visible to investors in target-date products.

How significant are these losses?

Question 3 is more of a philosophical matter. As an investor close to retirement, how should one feel about the losses incurred? Is it an acceptable level of loss, or something more worrisome?

As I’ve noted already, 2025 funds all have some level of exposure to equities, so a degree of losses should be expected. Furthermore, we’ve been living through an unusual stretch when bonds have not served as much of a buffer, with most core bond funds also losing money and not serving their traditional safe-haven role (though they’ve lost less than stocks).

What I found somewhat surprising is how close many 2025 funds have come to the level of the stock market’s losses. For the four months through April, the S&P 500 lost 12.92% while the Russell 3000 lost 13.78%. As noted above, most funds lost between 10% and 12%, while a handful lost close to 13%.

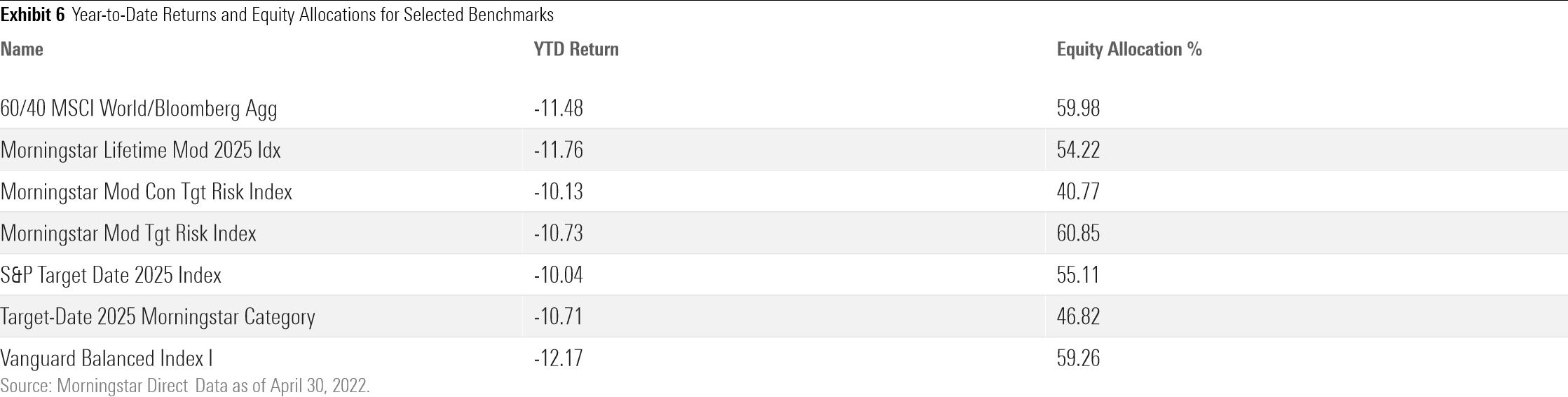

However, looking at a sampling of allocation-fund and target-date benchmarks, we can see that losses on this scale were the norm, not the exception. For example, the Morningstar Moderate Conservative Target Risk index, which has a 40/60 stock/bond mix, produced a negative 10.13% year-to-date return. With the “imperfect” storm of high inflation, a tightening Fed, high stock valuations, and global geopolitical uncertainty, the typical forms of diversification have simply not provided any shelter for investors in 2022.

To say that 2025 funds’ losses have been within a reasonable range relative to benchmarks is not the same as saying that they are comfortable, or even acceptable, for near-retirees. How alarmed should such investors be by a 10% to 12% decline in their nest eggs?

As my colleague Amy Arnott recently noted, sequence-of-return risk, while real, has usually been overcome by the forward progress of the stock market over time. This has been the case even in the face of deep market collapses, although the recovery time for nest eggs was extended in those cases. As Amy notes, “The key takeaway is that even during horrible market environments—and unfavorable patterns for sequence of returns—retirees have historically still been able to recover their lost wealth.”

To put matters into some historical context, the target-date 2000-2010 Morningstar Category, which would have been roughly equivalent to the 2025 fund for investors during the global financial crisis, experienced a peak-to-trough decline of 34%. So while current losses sting, there is historical precedent for even greater declines; patient investors were eventually made whole, and then some, in the subsequent bull market. Keep in mind that in the most difficult cases the times to recovery can be lengthy. Amy’s article points out that for investors who retired in 2000, the one-two punch of the tech crash in the early 2000s and the 2008-09 bear market meant their portfolios did not fully recover until 2013 (but then benefited from the lengthy bull market to follow).

What Should Investors Do?

When it comes to investment choices, the best option for most nervous investors is to do nothing and sit tight, as hard as that can be. Attempting to time markets is notoriously difficult, and the with sharp losses already in the books, the chances of missing out on a rebound escalate.

There are steps retirees and near-retirees can take to adjust to the impact of a (temporarily) reduced nest egg. Christine Benz walks through many of these options in a recent column, and they range from working longer to reducing expenses to adopting the “bucket approach” to investing, among others.

Finally, for investors who are further out from retirement, say 10 years or longer, and who have the bulk of their 401(k) assets in a target-date fund, it’s worth taking a moment to assess the glide path philosophy of your target-date investment. While most employers don’t offer multiple target-date options, if you determine that the vehicle has a more-aggressive approach than you’re comfortable with, there are still steps you can take to mitigate the equity risk, such as diverting a portion of those assets to a cash-like investment as you get closer to retirement. At the very least, it is a useful opportunity to check in on your retirement investments and make sure that it still fits with your own risk preferences and investment goals.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/2e13370a-bbfe-4142-bc61-d08beec5fd8c.jpg)