Sustainable Funds Landscape - Highlights and Observations

Let's try for greater transparency in 2022.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Sustainable funds and investors had enormous success in 2021. Investors poured nearly $70 billion into sustainable funds, and returns generally outpaced those of conventional funds. With so many more people investing sustainably, and doubtless many more still on the sidelines, I’d like to see 2022 be a year marked by greater transparency to minimize gaps that I think are emerging between what investors expect and how funds are actually executing their sustainable investing mandates.

First, some highlights from our latest "Sustainable Funds U.S. Landscape Report" and then we'll get to the need for greater transparency and a few other observations. The report, ably written this year by Morningstar sustainability analyst Alyssa Stankiewicz, can be downloaded here.

Sustainable Funds Landscape Highlights

The sustainable funds landscape in the United States continued to grow in 2021. Investors added nearly $70 billion into open-end and exchange-traded funds that claim some type of sustainable investing mandate, and these 534 funds now have more than $350 billion in assets. During the year, 121 new sustainable funds launched and 26 existing funds adopted a sustainable investment mandate.

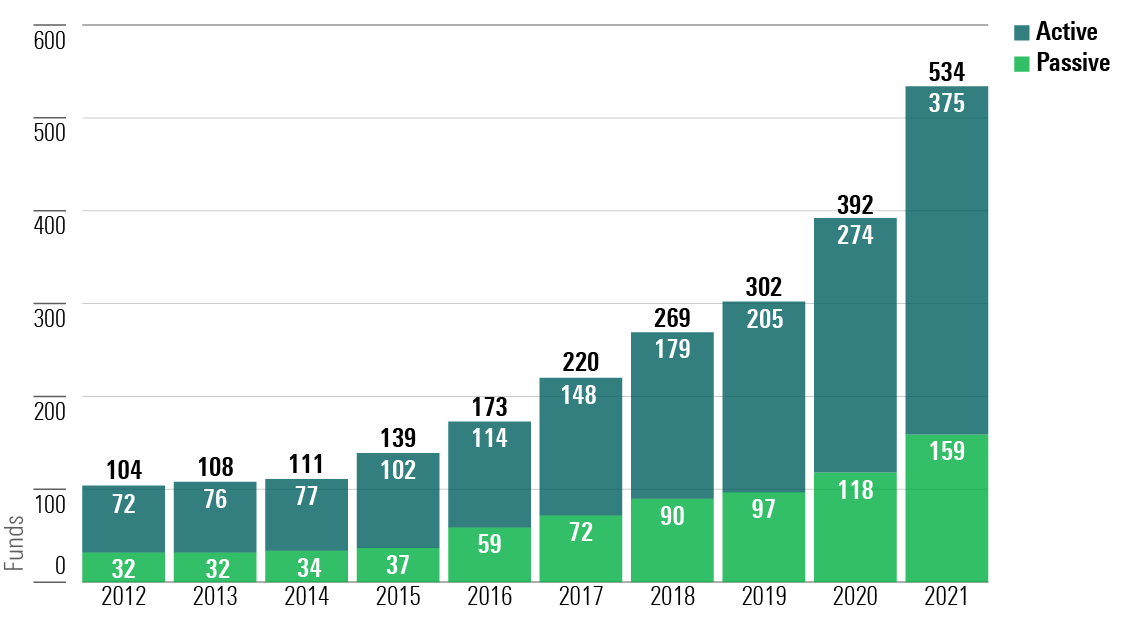

There are 5 times as many sustainable funds in the U.S. today than a decade ago, and 3 times more than five years ago.

Exhibit 1 Growth of U.S. Sustainable Funds Universe, 2012-21

Source: Morningstar Direct. Data as of Dec. 31, 2021. Note: Includes funds that have been liquidated during this period.

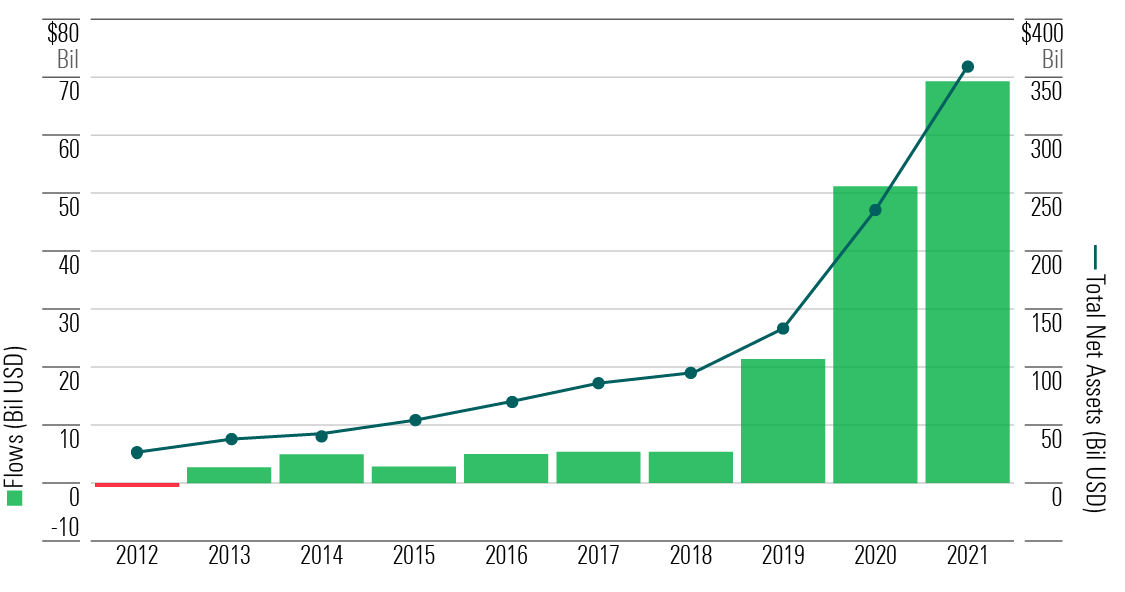

Net flows flew past the record set in 2020 and are 14 times what they were three years ago. Net assets have increased 3.5 times since 2018.

Exhibit 2 Growth of U.S. Sustainable Funds Flows and Assets, 2012-21

Source: Morningstar Direct. Data as of Dec. 31, 2021. Includes Sustainable Funds as defined in Sustainable Funds U.S. Landscape Report, January 2022. Includes funds that have liquidated; excludes funds of funds.

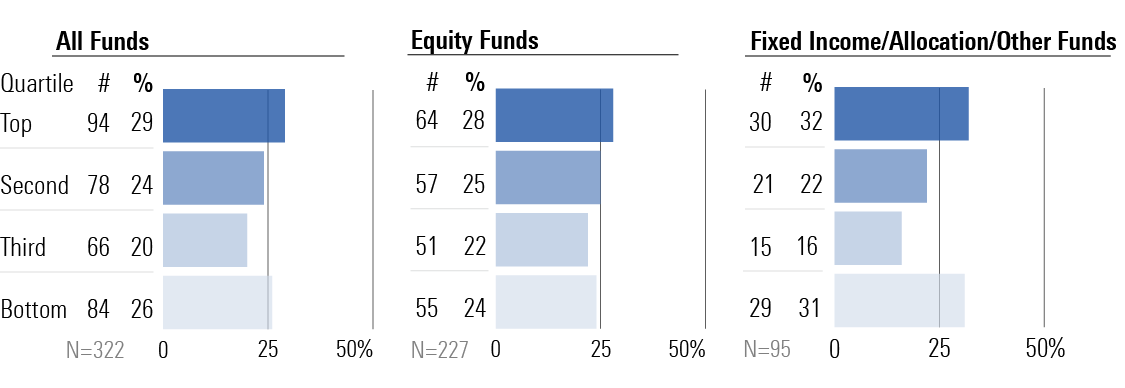

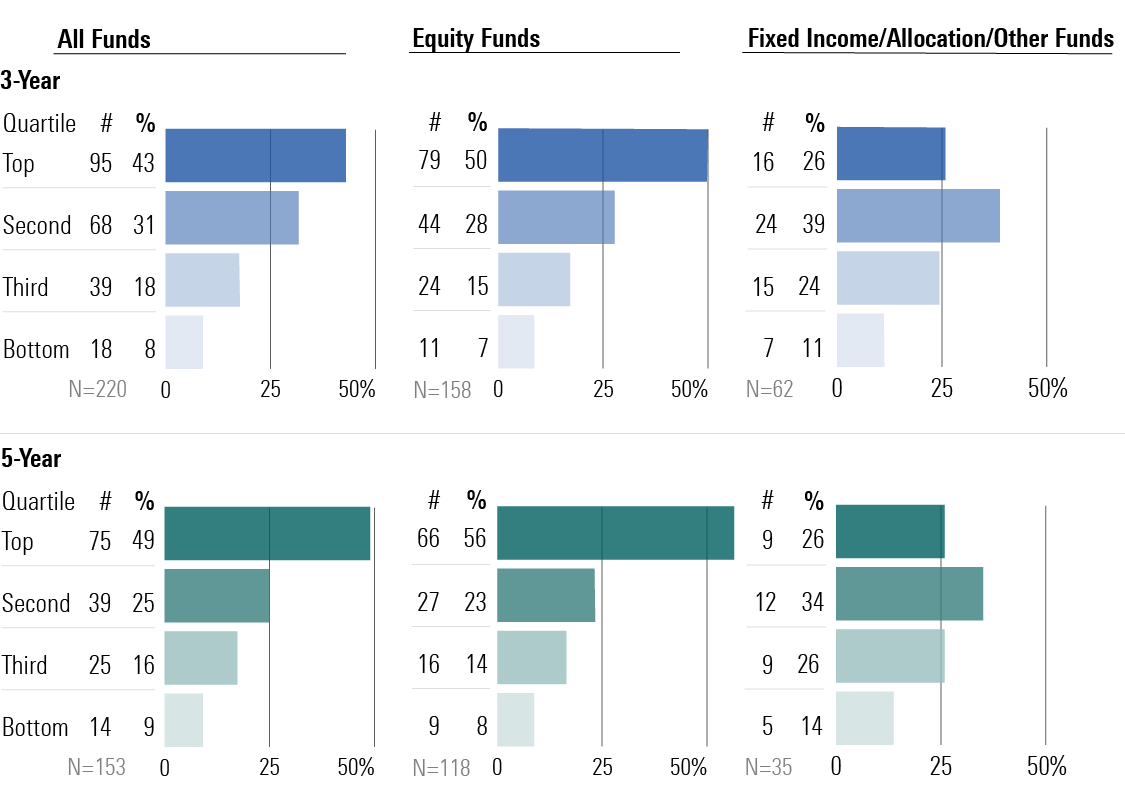

The collective performance of sustainable funds was on par with the overall fund universe in 2020, perhaps even a bit better--and for the trailing three and five years, quite a bit better. Nearly three of every four sustainable funds with records that long place in their Morningstar Category's top half, driven mainly by the performance of sustainable equity funds.

Exhibit 3 U.S. Sustainable Funds 2021 Return Rank by Morningstar Category Quartile

Source: Morningstar Direct. Data as of Dec. 31, 2021. Does not include repurposed or obsolete funds.

Exhibit 4 U.S. Sustainable Funds 3- and 5-Year Trailing

Source: Morningstar Direct. Data as of Dec. 31, 2021. Does not include repurposed or obsolete funds.

Performance by Morningstar Category Quartile

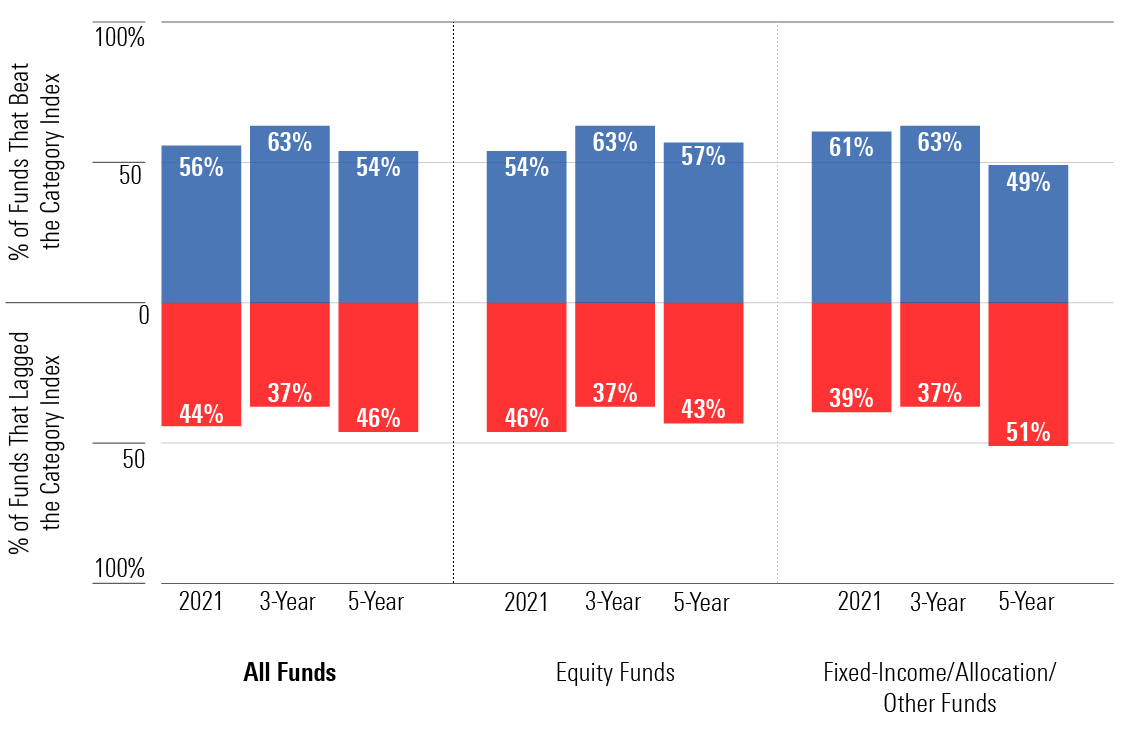

Another way to look at performance is comparing returns against those of a relevant index. Here, sustainable funds also did well in 2021 and have done well for the trailing three- and five-year periods.

Exhibit 5 U.S Sustainable Funds Success Rates Versus Morningstar Indexes

Source: Morningstar Direct. Data as of Dec. 31, 2021. Does not include repurposed or obsolete funds.

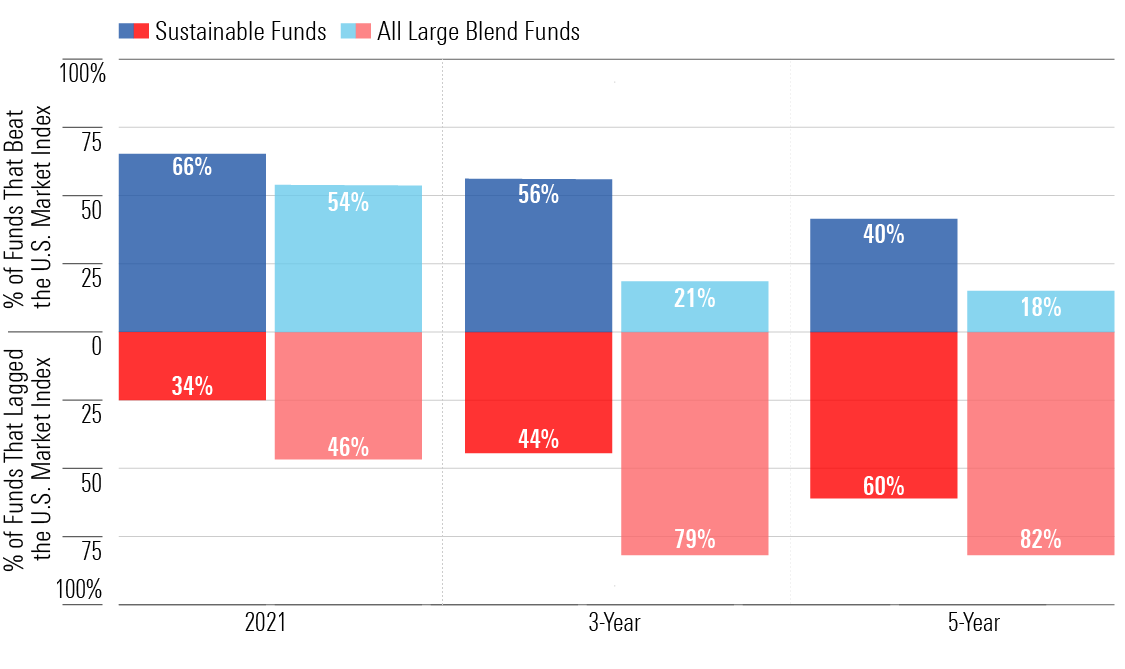

Focusing on core U.S. equity funds, two thirds of sustainable offerings in the large-blend category topped the U.S. market index last year compared with 54% of all funds in the category. And take a look at those three- and five-year numbers.

Exhibit 6 U.S. Sustainable Large-Blend Fund Success Rates Versus Russell 1000 Index

Source: Morningstar Direct. Data as of Dec. 31, 2021. Does not include repurposed or obsolete funds.

Observations on the Sustainable Funds Landscape

On performance. Over the past five years, sustainable funds on the whole have shown they can perform on par with or better than conventional funds. For investors and advisors who have been hesitant to invest in sustainable funds because they are under the impression that such funds as a group chronically underperform, last year is further evidence that this isn't true--as are the past five years. Even prior to that, as I argued in this older piece, sustainable funds have tended to perform better than their detractors claimed.

That doesn't mean you should always expect outperformance from sustainable funds. So far in 2022, to take an example staring us in the face, about two of every three sustainable funds place in the bottom half of their category. But if you want to be a sustainable investor, don't let old performance myths stand in the way.

On the different types of sustainable funds. Despite my own characterization of these funds as a single group so far in this piece, keep in mind that sustainable funds employ a range of approaches. Any given sustainable fund may not be much like another.

First, not all of them are equity funds. The universe now contains more than 100 bond funds and well covers the range of asset and sub-asset classes that most fund investors want and need in their portfolios.

In areas where you can't find an appropriate sustainable option, substitute conventional funds that consider environmental, social, and governance factors, not as central their investment process but as one component of it. This is sometimes hard to ascertain, but you can look at their prospectus or website for descriptions of the role ESG analysis plays in their investment processes. You can also consider conventional funds with Morningstar Sustainability Ratings of 4- or 5-globes, which is an indicator that the companies they hold in their portfolios are exposed to lower levels of material ESG risk than their peers.

Second, there is a clear distinction between funds taking what I consider to be a general ESG approach and those that focus on sustainability themes. Those taking a general ESG approach typically use exclusions and company ESG metrics to craft portfolios that give you exposure to an area of the market (U.S. large caps, emerging markets, and so on) similar to the exposure you would get from a conventional option. The difference is that the ESG funds avoid ESG underperformers and accentuate the outperformers in some way. The resulting portfolios may not look as different from conventional portfolios as you might expect.

Funds that focus more on sustainability themes don't rely as much on company ESG metrics as they do on the products and services produced by a company. They look for companies that are well-positioned to benefit from the transition to a more-sustainable low-carbon economy. Tesla TSLA, for example, may be a prominent holding for a sustainability-themed fund, but a much more problematic one for a general ESG fund because of its treatment of workers, including a troubling racial discrimination and harassment lawsuit.

On the need for greater fund transparency. Sustainable funds almost by definition should be more transparent than conventional funds about what they're doing. This starts with a clear description of which approach or combination of approaches a fund employs to fulfill its sustainable investing mandate. No one should be left to guess about the centrality of a fund's sustainability principles to its process or about how it is applying those principles in practice. This should include a fund's approach to engagement and proxy voting with regard to sustainability issues and how the fund assesses its own impact beyond generating financial returns.

Two new tools are available for funds to use. The Morningstar Sustainable-Investing Framework lays out six key sustainable investing approaches. Funds can use it as a template for reporting. They also can use the CFA Institute's new Global ESG Disclosure Standards, which I regard as complementary to the Morningstar framework.

Sustainable funds should make better use of the prospectus to describe their approach, and more of them are already doing so. This comes on the heels of many years of funds of all types providing only the bare minimum of information in the “Principal Investment Strategies” section of the prospectus so as to leave managers with greater flexibility. But transparency should be the watchword for sustainable funds, and the place to start is the prospectus. Regulators may soon require this anyway.

Another opportunity for greater transparency can be found in impact reporting. Many sustainable funds have been producing impact reports of varying quality. These reports can be more heavy on marketing than substance, reminiscent of early corporate sustainability reports. But just as the latter have gotten more substantive over time, so too can sustainable fund impact reports.

Finally, investors of all types need to know more about climate change and how it figures in any investment strategy. Every asset manager should have a clear and accessible Statement on Climate Change that lays out the firm's approach to assessing climate risks in portfolios; whether, and the extent to which, it is investing in climate-related opportunities; how it is engaging with companies and voting on climate-related issues; and its climate-related policy activities and expenditures. They should also make clear how these things apply to each of their funds.

Improving transparency will help reduce the mismatch between investor expectations and their sustainable investments, which I think is at the root of a lot of greenwashing concerns. It is something that sustainable investors, from end investors to asset managers, should fully embrace in 2022.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OMVK3XQEVFDRHGPHSQPIBDENQE.jpg)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WJS7WXEWB5GVXMAD4CEAM5FE4A.png)