Manager Question of the Month: What’s the Biggest Risk Factor?

Valuations and the effect of loose monetary policy on asset prices and capital allocation are top of mind for some equity managers.

/s3.amazonaws.com/arc-authors/morningstar/e6b4cff4-0d77-4881-abc5-5b0b34d64bf6.jpg)

Each month Morningstar manager research analysts speak with dozens of portfolio managers. The main purpose of these interviews is to inform our annual coverage and rating of more than 2,200 strategies in the United States and even more globally. Each time we speak with a manager we revisit their team, process, and any portfolio changes they have made, while also touching on performance.

These conversations give Morningstar access to a wide-ranging breadth of manager opinion and insights. One of the most fun parts of this job is learning what they see in the markets. Since our global fund reports, however, focus mainly on the managers’ strategies, many interesting tidbits we hear about companies, economic trends, markets, and other topics end up on the cutting-room floor.

There are a lot of interesting--and potentially actionable--insights in that pile on the floor. It would be a shame to let them go to waste. In this, the first installment of what could become a regular feature, we’ll share a sample of some of what we’ve heard from managers recently, generalized or anonymized so managers can still feel comfortable speaking as candidly as possible.

This article will focus on a question we posed to the equity managers we spoke to before the end of 2020: What's the biggest risk factor you see when looking at potential companies to invest in? The diversity of responses (and risk factors) reflects the variety of managers we speak with each month.

For starters, several managers were concerned about the deluge of monetary stimulus that central banks have injected into their economies and markets. One large-value manager expressed concern over the unprecedented amount of monetary stimulus and the resulting debt (a common concern), and what the long-term effects of such stimulus might be, including the possibility of greater inflation.

Similarly, two specialty-equity managers cited a concern over the mispricing of risk owing to central banks taking rates essentially to zero, which has even led to negative rates for some sovereign bonds. In one manager’s view, this has led to distortions in the pricing of risk in the bond market, with currencies potentially at risk as well. The other manager worried that low borrowing costs could lead corporate executives to misallocate capital, perhaps choosing to grow for growth’s sake rather than focusing on return on capital.

Related to this, an international-equity manager said he was concerned about increasing corporate leverage when the global economy seems to be late in its cycle. He worries how such indebted companies might deal with their obligations should economic conditions worsen.

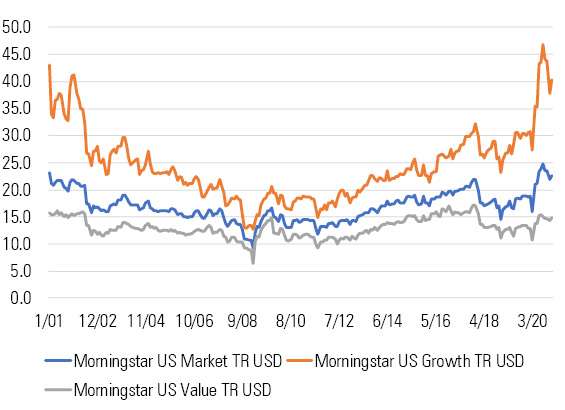

Naturally, that flood of stimulus has influenced valuations, too. Two value-oriented managers lamented the lack of investment opportunities created by high price multiples. Part of what happens at such times is that the market, always forward-looking, begins pricing in ever-more-distant earnings. It’s not uncommon for the market to discount earnings a year or so away, but these managers said that the market is already assigning high price multiples to 2022 earnings.

Exhibit 1: High Growth-Stock Valuations Are a Concern

Meanwhile, the market has also gotten more concentrated, with just a handful of names leading U.S. indexes higher in 2020. Apple AAPL, Microsoft MSFT, Amazon.com AMZN, Tesla TSLA, Facebook FB, and Alphabet GOOG alone accounted for a combined 23.2% of the S&P 500 as of Jan. 8. An increasingly lax approach to valuation compounded their concern over concentration risk.

As has been well documented, all these companies fall firmly in the growth-stock camp, which has made life very difficult for value managers. To this end, two value managers worried over when and if value stocks might ever fully rebound and overtake growth stocks as market leaders. An emerging-markets equity skipper voiced a similar concern, lamenting that U.S. growth stocks seem to dominate investors' consciousness, leaving him wondering what it would take for emerging-markets stocks to get their due.

Finally, managers also voiced concerns over increased regulatory risk, the possibility of COVID-19 doing additional damage, and the possibility of technological disruption as digital platforms continue to pose threats to more traditional business models.

So, while there is no shortage of potential risks on the horizon, it’s worth keeping in mind the fact that, as Warren Buffett has said, the future is always uncertain. We also may revisit some of these risks when we poll managers in future months. Until then, stay tuned for additional manager insights.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/FGC25JIKZ5EATCXF265D56SZTE.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/e6b4cff4-0d77-4881-abc5-5b0b34d64bf6.jpg)