Here's Why You Should Rebalance

Keep your portfolio's risks in check with this one simple trick.

/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)

/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)

Over the past decade, investors have become accustomed to U.S. stocks hitting new all-time highs. While the extended bull market has been a boon to portfolio balances, investors that have let the market's rise drive their equity allocations higher may now be holding riskier portfolios than they initially signed up for. For example, a hands-off investor that built a traditional 60/40 portfolio 10 years ago would have a portfolio that's closer to 80% in equities as of the end of 2019. It's possible our hypothetical investor's risk tolerance skyrocketed along with the stock market, but it's more likely that the current portfolio no longer resembles an appropriate blend of risky and safe assets.

Rebalancing, or selling a portfolio's best performers to buy the worst performers periodically, is one of the best ways to protect against market movements altering a portfolio's risk profile. The advantages of rebalancing are especially apparent in tax-favored accounts, such as IRAs or 401(k)s, where tax implications are not a concern. Rebalancing may also be prudent in taxable accounts, but the advantages aren't as straightforward, as it may trigger capital gains taxes depending on the investor's income level and capital gains exposure. As such, this article evaluates the merits of rebalancing in tax-favored vehicles.

There are multiple rebalancing strategies that investors can employ. Before we dive into those, we'll first examine what the investor experience would have been like over the past 26 years without rebalancing.

The Ebbs and Flows of a Buy-and-Hold Portfolio To illustrate a buy-and-hold investor's experience, we built a 60/40 portfolio using the following indexes:

- S&P 500 (45%)

- FTSE All-World ex U.S. Index (15%)

- Bloomberg Barclays U.S. Aggregate Bond Index (40%)

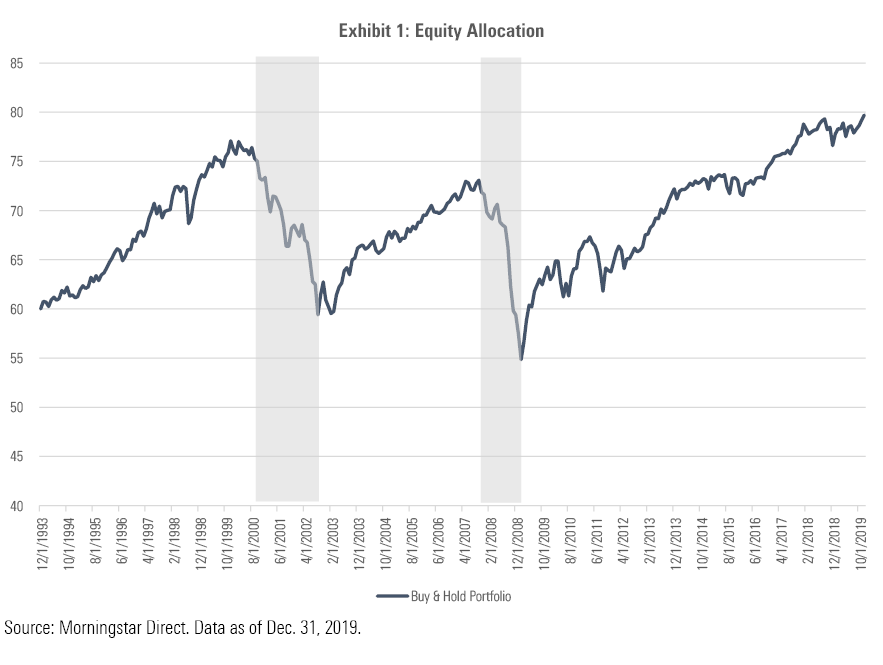

We ran the portfolio's returns over the past 26 years, from 1994 through the end of 2019, and tracked its equity allocation and drawdowns over the period. Exhibit 1 shows how the weighting to equities changed over time.

The portfolio's equity allocation grew to 76% from 1994 through August 2000, leading into the first major bear market of the 2000s. It again peaked just before the start of the financial crisis in October 2007, with 73% in equities. As of the end of 2019, the allocation to equities reached its highest level over the entire period, nearing 80% of assets.

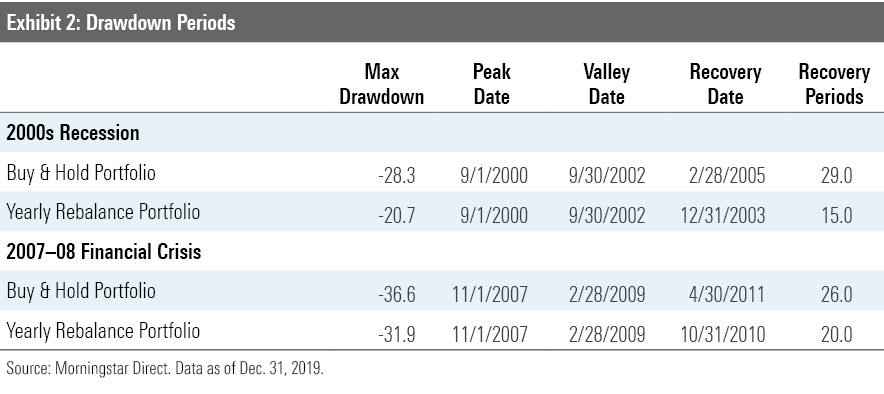

Unfortunately, the elevated allocations heading into the two bear markets of the past 20 years meant more pain during those drawdowns and a longer wait to recover those losses. Exhibit 2 shows the max drawdown during both periods and how long it took the portfolio to recover its losses compared with the same portfolio that was rebalanced annually at the end of each year, arguably the simplest rebalancing strategy.

During the bear market spanning September 2000 to October 2002, the buy-and-hold portfolio lost 28.3% and took 29 months to fully recover the losses. If the investor had rebalanced annually, the drawdown would have been less severe: Over the 25-month period, the rebalanced portfolio experienced a 20.7% loss, outpacing the buy-and-hold portfolio by 760 basis points. A byproduct of its more subdued drawdown, the rebalanced portfolio recovered almost twice as fast, reaching its previous high 15 months after it troughed.

The story was similar during the 2007-08 financial crisis, when the buy-and-hold portfolio's overweighting in equities led to a loss of 36.6%. Once again, it took more than two years for this portfolio to fully recover. In comparison, the annually rebalanced portfolio lost 31.9% over the 16-month drawdown period, clearly ahead of its unbalanced counterpart. The time to fully recover those losses was also shorter, with a recovery period of 20 months.

Given what research has shown about investor behavior, investors struggle to hold on during severe drawdowns. They often sell out of their declining equity positions for safer havens, locking in losses, extending the recovery period, and consequently hampering overall performance.

How Often Should You Rebalance? The experience of a buy-and-hold portfolio can be tumultuous, but rebalancing can help smooth out the ride. To illustrate this, we created six different rebalancing versions of the initial 60/40 portfolio. Five of the strategies employed rebalancing frequencies spanning from daily--the least realistic for the average investor--to annually--arguably the most realistic. The last strategy rebalanced only when the underlying stock allocation drifted more than 5 percentage points from the strategic allocation for each index.

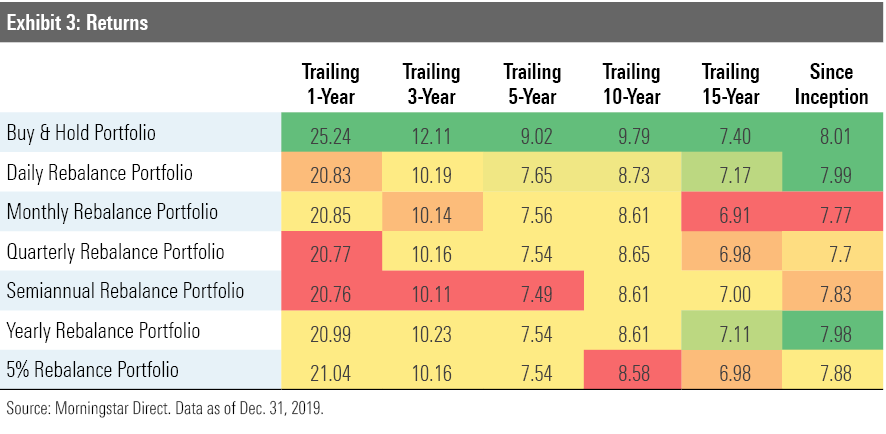

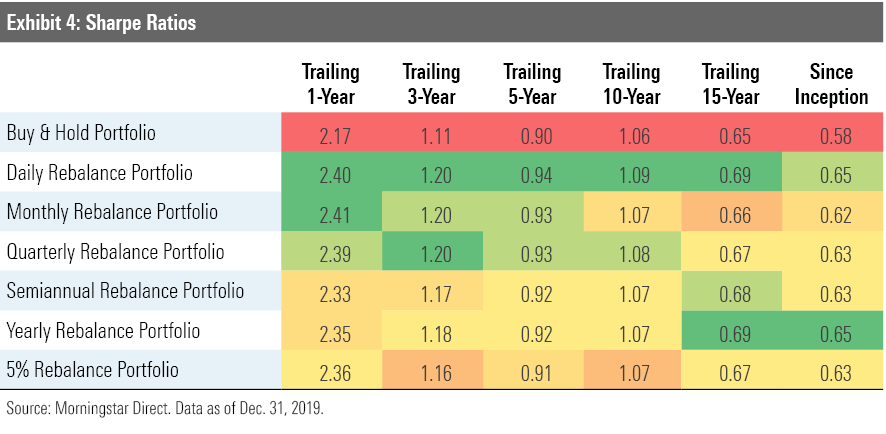

Exhibits 3 and 4 compare both the trailing returns and Sharpe ratios for each portfolio. We can draw several conclusions from these exhibits:

- Exhibit 3 illustrates that the buy-and-hold portfolio earned slightly higher returns than all of the rebalancing portfolios. However, it also had significantly higher volatility because its equity weighting increased to such high levels during stock market rallies, making the return advantage not worth the risk.

- Exhibit 4 shows that all of the rebalancing portfolios had higher risk-adjusted returns, as measured by Sharpe ratio, than the buy-and-hold portfolio over the trailing one-, three-, five-, 10-, and 15-year periods and since the 1994 inception. That result owes to the lower volatility experienced by the rebalancing portfolios.

- Daily, monthly, or even quarterly rebalancing may be an unrealistic expectation for do-it-yourself investors, but a combination of annual rebalancing and periodic reviews for large fluctuations, such as 5-percentage-point deviations, should be within the realm of possibility. (Plus, over the 26-year span, the annual rebalanced portfolio's equity weighting eclipsed 65% only once; in other words, the deviations from strategic weightings using that approach are reasonable.) Our research shows that doing so will lead to better outcomes over the long term relative to buy-and-hold investors.

In summary, it's tough to predict where the market is headed, but we can control our portfolio's risk exposure through prudent rebalancing, and history suggests that will lead to better results for investors.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/a3ffb7d7-3689-49a2-bfde-9235ef1e06ad.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/af89071a-fa91-434d-a760-d1277f0432b6.jpg)