ETFs vs. Mutual Funds: The Benefits That Really Matter

How ETFs stack up against mutual funds on tradability, tax efficiency, transparency, accessibility, and fees.

/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)

In many ways, exchange-traded funds are an evolution of mutual funds. ETFs are like mutual funds that trade throughout the day but are more tax-efficient, transparent, and accessible. And they are often cheaper than their mutual fund forebears.

But these advantages don’t apply to every ETF. Some purported benefits of ETFs are oversold, while others are underrated.

Let’s take a closer look at ETFs and mutual funds and which advantages really matter to investors.

Tradability

Investors can trade ETFs like stocks: They can go long ETF shares, sell them short, buy them on margin, buy and sell options on them, and lend them to others to collect a fee. This versatility can draw in a diverse investor base, which aids ETFs’ robust liquidity ecosystem. This keeps ETFs trading at or near their net asset value and limits costs for investors.

Mutual fund orders are priced at the end-of-day NAV, which means investors can only trade at closing prices. They also don’t share the same versatility as ETFs in terms of shorting, options, and lending; and sales loads can make them extremely costly to trade, making mutual funds much less flexible than ETFs.

The ability to trade ETFs like stocks, however, is not much of an advantage for most investors. Jack Bogle infamously detested ETFs (at least initially) because of their tradability. He believed trading to be a losing proposition for investors, and I agree. But flexibility adds value if investors stay disciplined.

Tax Efficiency

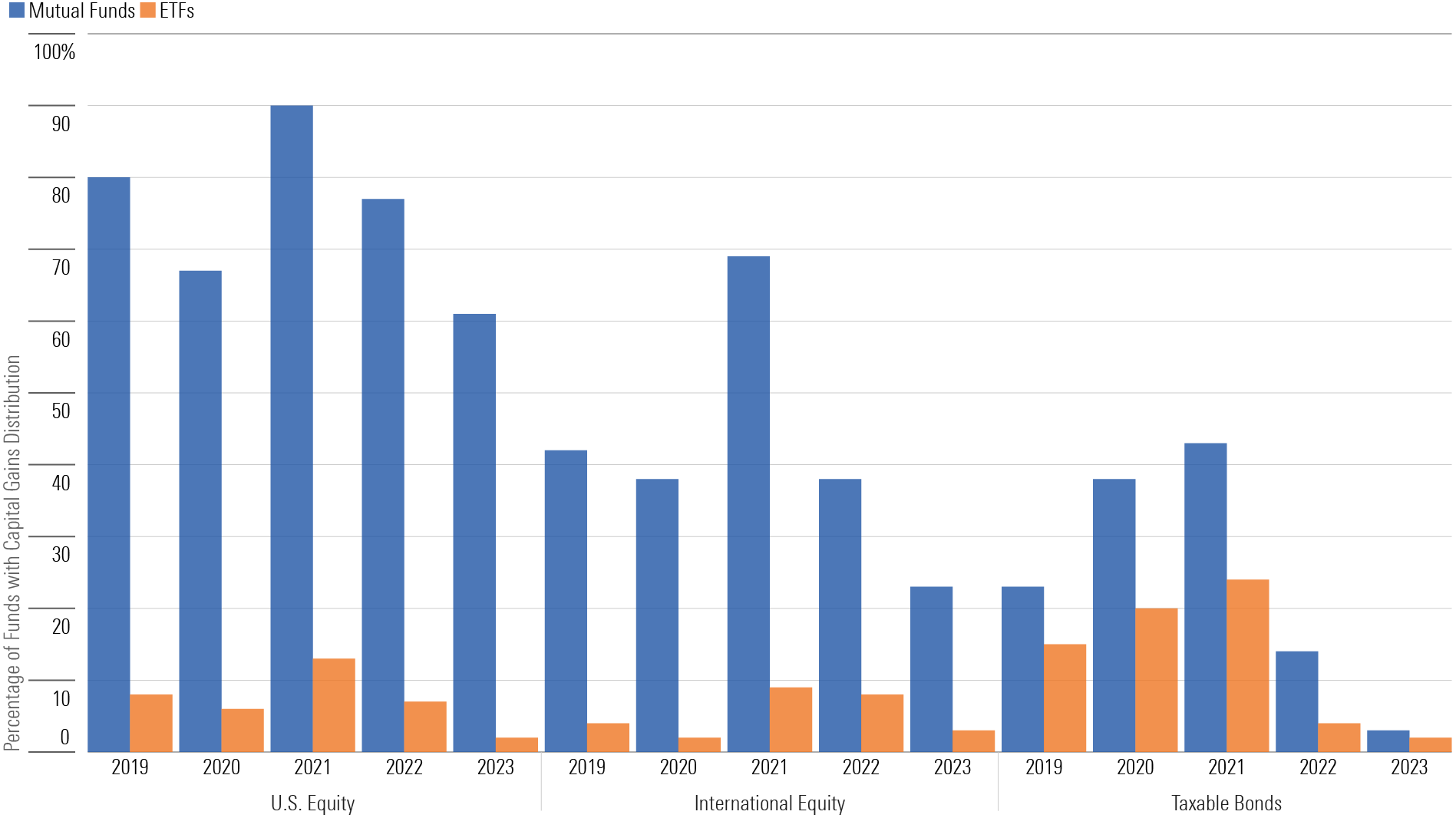

ETFs have a tax advantage over mutual funds, but the size of their advantage depends on the investment strategy and asset class of the fund.

By virtue of in-kind creations and redemptions, ETFs come with tax magic that’s unrivaled by mutual funds. This creates a huge advantage for ETFs among investment strategies that kick off capital gains. The more funds trade, the more susceptible they are to selling winners and realizing capital gains. The effect is more pronounced in strategies that differentiate themselves from the market, like strategic-beta or concentrated active funds, which have higher turnover.

For example, momentum strategies trade often to keep recent winners in their portfolios. Two Fidelity momentum funds demonstrate how the ETF wrapper avoids capital gains distributions for a more tax-efficient experience:

ETFs Flex Their Tax Advantage

Other types of strategies, like market-cap-weighted index funds and bond funds, don’t benefit that much from the tax advantage of ETFs. Market-cap-weighted index funds tend to require little trading, and much of bond funds’ returns come from income.

For example, Schwab S&P 500 Index SWPPX is a mutual fund that had no capital gains in 2023 and minimal gains over the past five years (0.07% in 2021 and 0.09% in 2019). This is higher than top S&P 500 ETFs like iShares Core S&P 500 ETF IVV and Vanguard S&P 500 ETF VOO, but the difference is negligible.

Likewise, bond investors may not benefit as much from the ETF wrapper. A high portion of bonds’ total return comes from income, which is taxed separately from capital gains. In-kind redemptions have no effect on taxes tied to income.

Other gaps in the tax efficiency of ETFs may exist when they hold derivatives, physical commodities, and certain foreign securities that don’t benefit from in-kind redemptions.

Overall, ETFs’ tax advantage is clearest in U.S. equities. And the ETF structure should never hurt tax efficiency.

ETFs' Tax Advantage Is Most Effective for Stock Funds

Transparency

Most ETFs disclose their holdings every day, allowing investors to see what’s inside their portfolios daily instead of quarterly like most mutual funds. Daily transparency adds accountability and removes some of the mystique of discretionary active managers. But it adds little value for most investors, who would be wise to go outside and get some fresh air rather than check their ETF’s daily holdings.

Accessibility

No investment minimums and innovative strategies, when appropriate, give ETFs a leg up on mutual funds for their accessibility, but investors don’t need most of the thousands of ETF strategies available. I’m looking at you, single-stock covered-call ETFs.

Fees

While ETFs often have lower fees than mutual funds, there are additional factors to consider when measuring the cost of owning an ETF.

Asset managers often price ETF fees at the same level as the institutional share class of mutual funds, with no sales loads. This is part of the reason why the average ETF costs half as much as the average mutual fund (0.50% vs 1.01%).

If you’re comparing an ETF and a mutual fund that track the same index, the fee difference may not outweigh the trading costs associated with the ETF. Trading at NAV can be an attractive feature for low-cost index-tracking mutual funds.

ETFs vs. Mutual Funds: The Bottom Line

ETFs carry advantages over mutual funds. Some, like lower tax bills and fees, can make a big difference for investors; others won’t be noticeable. But they rely on disciplined investing to work, as Jack Bogle believed. Investors should consider their own behavior before deciding whether to buy an ETF or a mutual fund.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T2LGZCEHBZBJJPPKHO7Y4EEKSM.png)

/d10o6nnig0wrdw.cloudfront.net/07-25-2024/t_56eea4e8bb7d4b4fab9986001d5da1b6_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/BU6RVFENPMQF4EOJ6ONIPW5W5Q.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/0fa19b38-60f6-4a0f-9e06-9869d9c57d52.jpg)