The Real Tax Magic of ETFs

The ETF wrapper doesn’t provide the same tax advantage for bonds as it does for most stocks. Here’s why.

/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)

A version of this article previously appeared in the December 2021 issue of Morningstar ETFInvestor. Click here to download a complimentary copy.

Exchange-traded funds have long been lauded for their improved tax efficiency over mutual funds. The advantage stems from their ability to purge low-cost-basis securities from their portfolios through the in-kind redemption process, the same mechanism that keeps ETFs' share prices in line with the value of their assets throughout the day.

Leveraging ETFs' tax efficiency to defer capital gains is more advantageous for some asset classes than others. Funds held in taxable accounts that derive more of their total return from capital appreciation (that is, stock funds) should benefit more from the ETF format than those that primarily provide income (bond funds).

The ETF Advantage

Mutual funds and ETFs have a lot in common. Both are subject to the Investment Company Act of 1940, which includes rules regarding distributions to fund investors. With regard to income, whether it comes from a stock dividend or a bond coupon, it all must be paid out to a fund's investors in the year it is received.

Mutual funds and ETFs differ in their ability to manage capital gains and losses. Mutual funds typically sell securities when they need to turn over specific names or meet redemption requests from their shareholders. This leaves them vulnerable to taxable capital gains distributions if the securities have appreciated in value.

ETFs can do the same, but they are also allowed to offload their shares to a specific type of market maker known as an authorized participant through an in-kind redemption. This transaction involves a trade of ETF shares collected by an AP for a basket of securities from the ETF. These trades shrink the number of ETF shares outstanding, keeping the supply of shares in line with demand. This, in turn, helps ETFs' share prices to hew closely to the value of the assets they own throughout the trading day. In-kind redemptions are tax-free transactions, allowing ETFs to rid their portfolios of securities with potential capital gains.

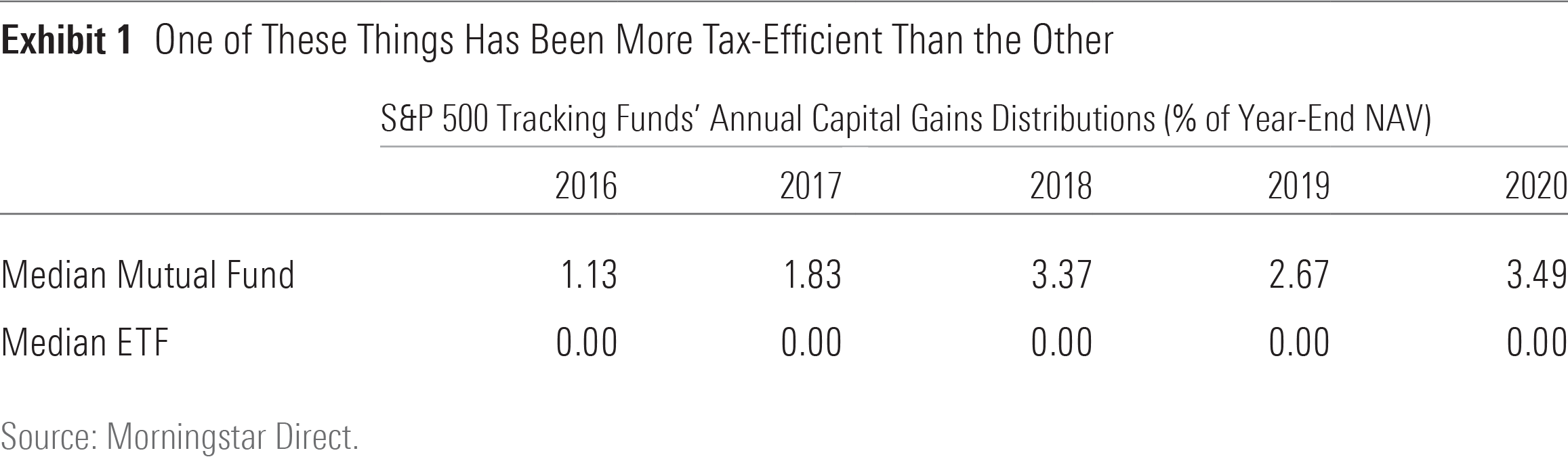

Real-world numbers illustrate the impact. Exhibit 1 shows the median capital gains distributions for ETFs and mutual funds in Morningstar's database that track the S&P 500 over the trailing five years through 2020. S&P 500-tracking ETFs flexed their tax advantages in each of those five years; none made a capital gains distribution.

On the other hand, almost every S&P 500-tracking mutual fund made a distribution in each of these five years, and those distributions weren't small. Typical payouts ranged between 1% and 4% of a fund's net asset value in any given year. Those are steep numbers, given the paltry turnover of the S&P 500. Lack of the in-kind redemption mechanism is a big part of the reason, but circumstances are also to blame.

Over the five years highlighted in Exhibit 1, investors collectively pulled money from many of these mutual funds, forcing them to sell holdings that had appreciated in value. Mutual funds (and ETFs) can sell shares at a loss to offset capital gains, but those opportunities are difficult to find when the market has been consistently marching higher and redemptions have been relentless.

Differences in the management processes may also explain the large capital gains distributions from mutual funds. For example, some of the funds included in the data featured in Exhibit 1 are most widely distributed through 401(k) plans. Reducing capital gains distributions is not necessarily a priority for these funds' managers. In these cases, big capital gains distributions won't necessarily result in higher tax bills for their investors.

Tax-Efficient Doesn't Mean Tax-Free

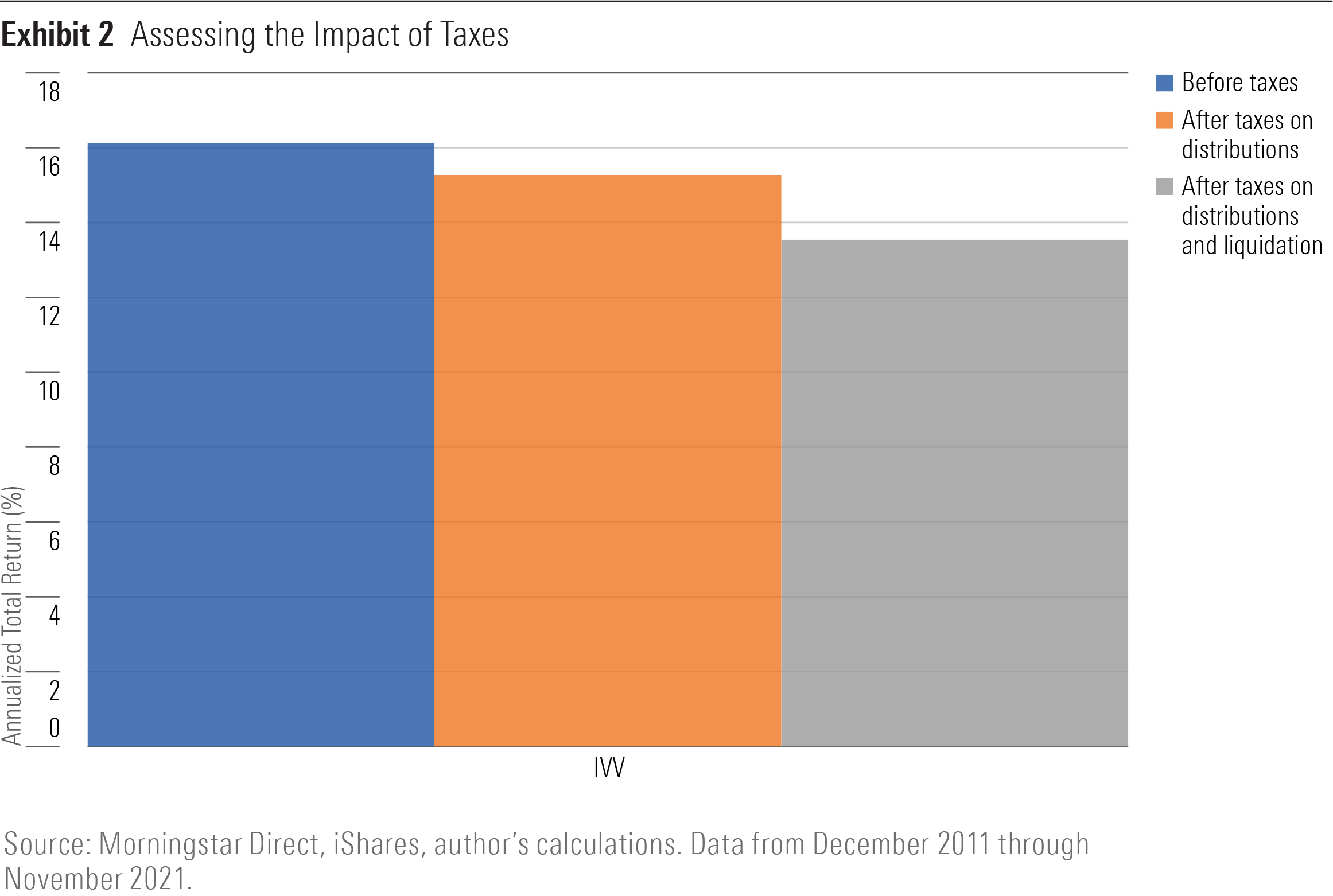

While ETFs may substantially reduce or even eliminate capital gains distributions, investors are still on the hook for taxes owed on income distributions paid by the stocks and bonds these funds own, which can have a meaningful impact on ETFs' aftertax total returns. Exhibit 2 shows the annualized total return for iShares Core S&P 500 ETF IVV under three different tax scenarios over a 10-year period from December 2011 through November 2021.

The first column is the fund's total return before accounting for any taxes on dividends or capital gains. The second column subtracts taxes owed on dividends as they are incurred over the 10-year period--a more realistic total return for an investor holding IVV in a taxable account. The third column is IVV's total return after an investor sold all shares on Nov. 30, 2021, and paid taxes on dividends and capital gains. The most-punitive marginal tax rates were used in these calculations. Income and short-term capital gains were taxed at 37%, while long-term gains were docked by 20%.

A few things are worth mentioning. First, IVV was among the ETFs in Exhibit 1 that made no capital gains distributions. The taxes incurred in the middle column were solely those owed on dividend payments. In total, those taxes reduced IVV's total return by about 5%: to 15.27 percentage points per year from 16.12.

A bigger tax hit occurs when an investor liquidates shares and pays taxes on the associated capital gains. The third column shows that selling IVV after 10 years further cut the fund's annualized total return to 13.54 percentage points, or a 16% reduction from the initial 16.12 pretax mark.

A sometimes-overlooked advantage lurks within those numbers. By avoiding capital gains distributions, IVV delays the associated taxes to a date when an investor chooses to sell. Reducing or eliminating capital gains distributions throughout the 10-year period allows those potential distributions to compound over time and further grow an investor's wealth. The real tax magic of many ETFs is that they help investors to defer capital gains taxes in a taxable account.

What About Bonds?

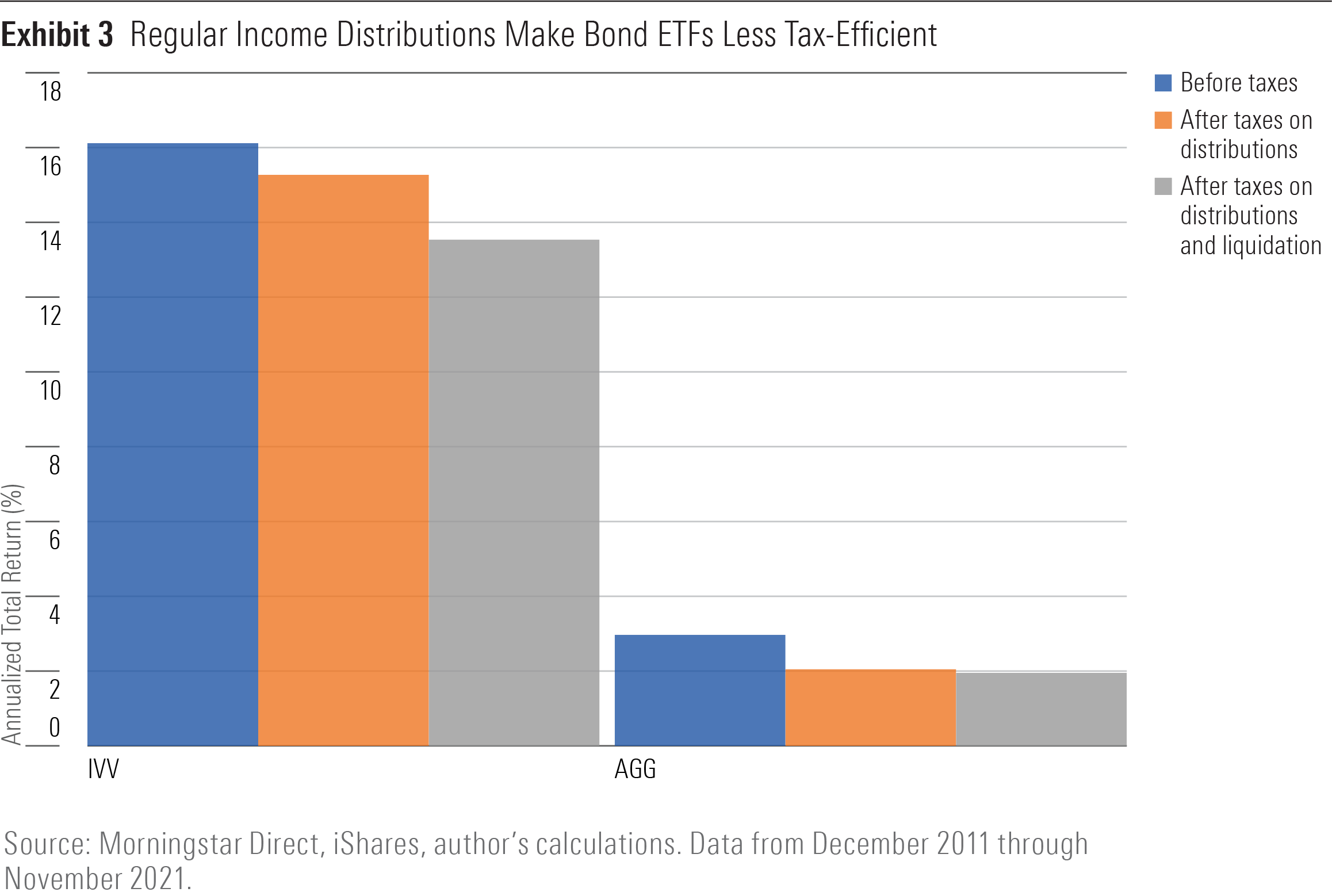

Not all asset classes benefit from ETFs' tax advantages to the same degree. Exhibit 3 builds on Exhibit 2 by adding the total returns for iShares Core U.S. Aggregate Bond ETF AGG under the same three tax scenarios.

The magnitude of AGG's total returns were considerably lower than those for IVV, reflecting the large performance gap between stocks and bonds over the past decade. Before any tax considerations, AGG returned more than 13 percentage points less per year than IVV over that period.

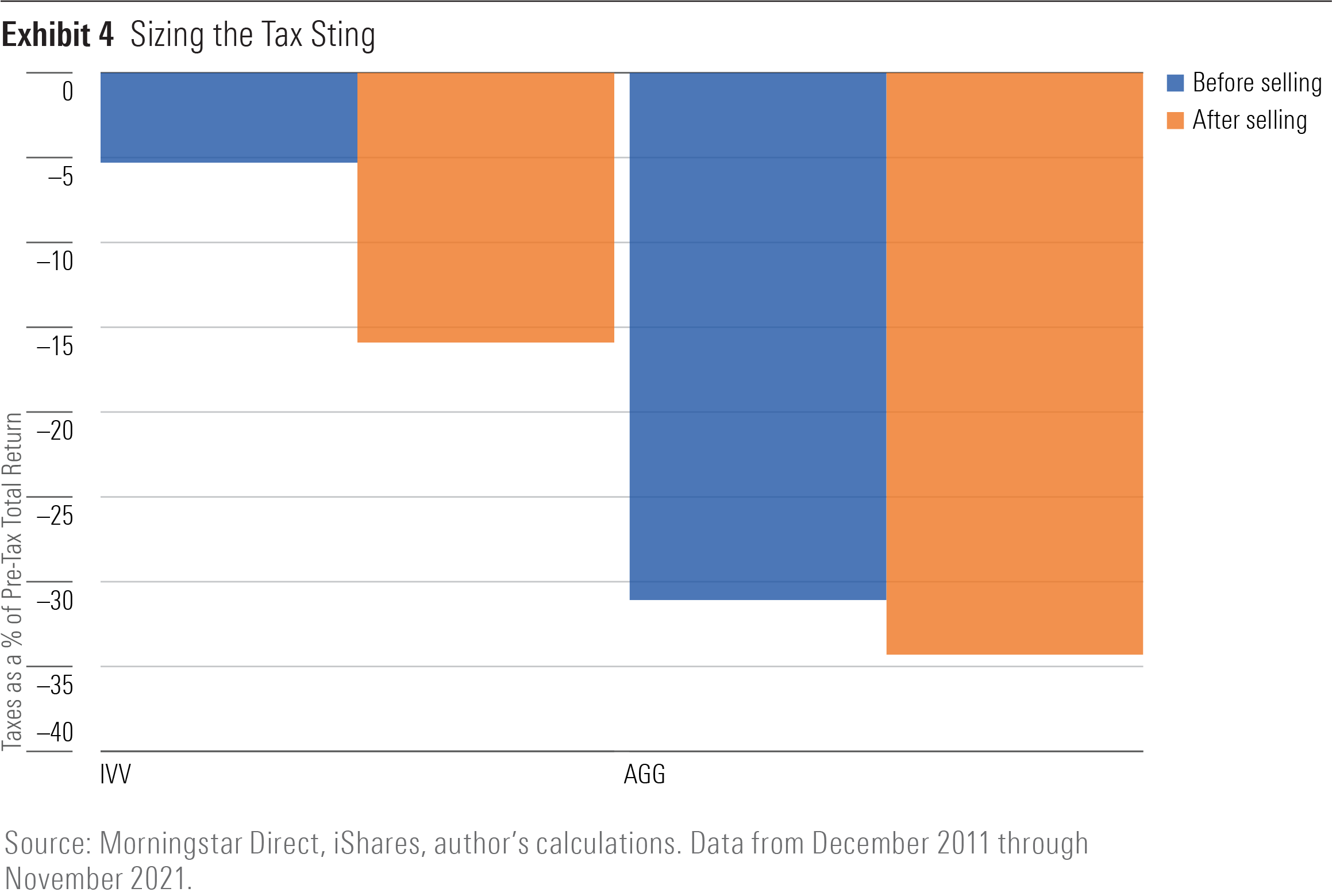

The reduction in AGG's total return from paying taxes on income distributions is the more important item to note. Compared with IVV, AGG's total return declined by a much larger portion of its pretax total return, dropping 31% to 2.05 percentage points from 2.97--a substantially larger reduction than the 5% hit incurred by IVV. Exhibit 4 illustrates the impact of taxes on IVV and AGG as a percentage of pretax annualized total return.

The reason for those big differences is straightforward. Most of AGG's total return came from coupon payments that are taxable at ordinary income rates. Like IVV's dividends, the ETF structure does not have a provision for delaying or avoiding taxes owed on those payouts. Investors must pay them as they are received. By comparison, most of IVV's total return came from capital appreciation.

The improved tax efficiency from the ETF wrapper comes from delaying realized capital gains, but fixed-income securities have lesser gains. Exhibit 4 further supports that fact. After liquidating a stake in AGG, an investor realized a 10-basis-point reduction in total return, or 3.3% of the fund's pretax total return over those 10 years. That's a minuscule amount compared with the reduction from income taxes.

The ETF wrapper does not provide the same magnitude of tax advantage for bonds as it does for stocks. ETFs are best-suited for stocks in taxable accounts. They offer a milder tax advantage for bonds, or any asset that throws off a substantial portion of its total return as income. But those assets are best held in a tax-deferred account such as an IRA or 401(k).

Disclosure: Morningstar, Inc. licenses indexes to financial institutions as the tracking indexes for investable products, such as exchange-traded funds, sponsored by the financial institution. The license fee for such use is paid by the sponsoring financial institution based mainly on the total assets of the investable product. Please click here for a list of investable products that track or have tracked a Morningstar index. Morningstar, Inc. does not market, sell, or make any representations regarding the advisability of investing in any investable product that tracks a Morningstar index.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/WDFTRL6URNGHXPS3HJKPTTEHHU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IFAOVZCBUJCJHLXW37DPSNOCHM.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/JNGGL2QVKFA43PRVR44O6RYGEM.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/78665e5a-2da4-4dff-bdfd-3d8248d5ae4d.jpg)