Energy Is Powering Large-Value Fund Performance

Some funds are bucking the trend.

/s3.amazonaws.com/arc-authors/morningstar/d8236d6f-dcec-4d1b-b5ba-e086adefd364.jpg)

Energy stocks are continuing their feverish pace in 2022. After returning 55.2% in 2021, the Morningstar US Energy Index was up 60.2% for the year through June 10, while the broader Morningstar US Market Index was down 15.5%. As a result, energy has become a more significant stake in value benchmarks. Energy is also having a bigger impact on fund performance in the large-value Morningstar Category, which, on average, has more exposure to the sector than other categories in the Morningstar Style Box.

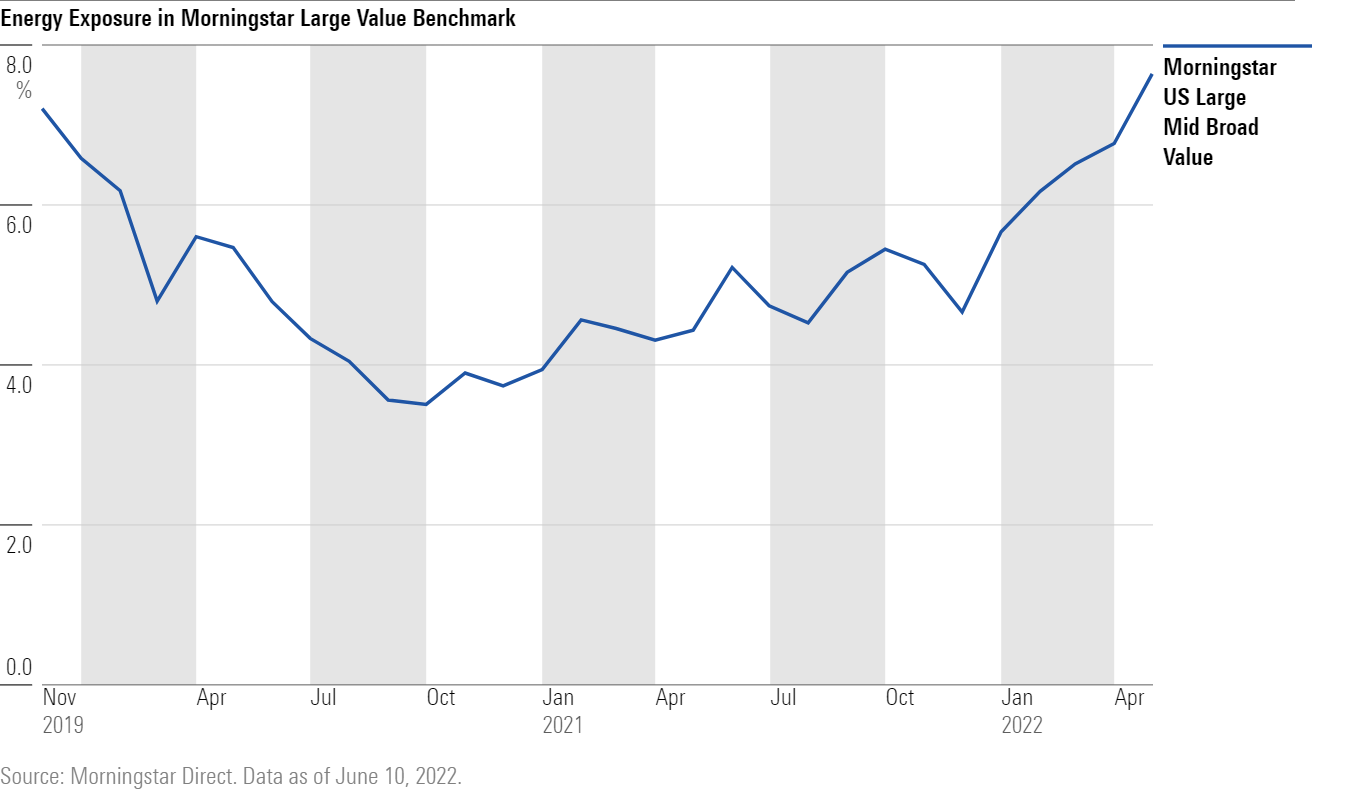

Energy exposure in value benchmarks has nearly doubled since its lows at the beginning of the pandemic. In October 2020, the energy sector represented only 3.4% of the Morningstar US Large-Mid Cap Broad Value Index, the Morningstar index for the large-value category, and as of mid-2021, energy still represented only 4.5%. However, that number increased to 7.6% of the index as of June 10. While still only a fraction of the exposure seen in the late 2000s, when energy was a 21.1% stake, this was still a significant increase from early pandemic levels.

Despite its strong performance, energy did not have an outsize impact in 2021, even on large-value funds. But this year, as funds' stakes in the sector have increased, and as energy outperforms other sectors, energy has driven many of the best-performing large-value portfolios.

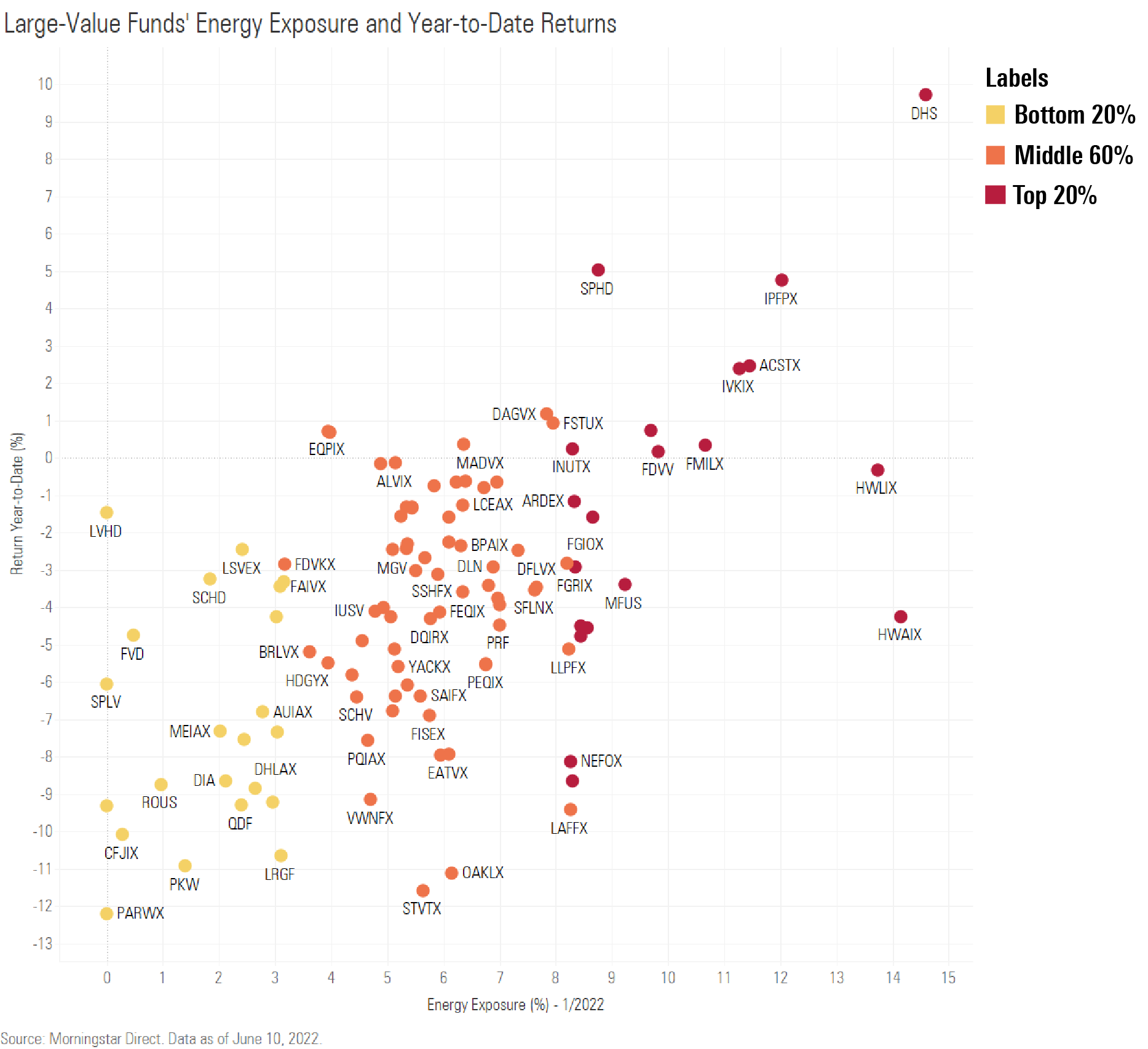

Looking at net energy exposure versus percentile rank for funds in the large-value category, the data shows a correlation between energy exposure and outperformance in 2022. Funds with higher exposure to energy tended to have higher returns. For example, large-value funds that landed in the top 20% when it came to energy exposure returned negative 1.1% for the year to date. Those with energy stakes in the bottom quintile returned an average of negative 7.8%.

While the majority of the top-performing funds had significant energy exposure, some have been strong performers year to date in spite of relatively small stakes in the sector. And some funds underperformed despite an overweight in energy.

We looked at some interesting large-value funds covered by Morningstar analysts using the Portfolio Analysis tool in Morningstar Direct to compare the funds' sector weights and stock picks against the Morningstar US Large-Mid Cap Broad Value Index.

Top Performers

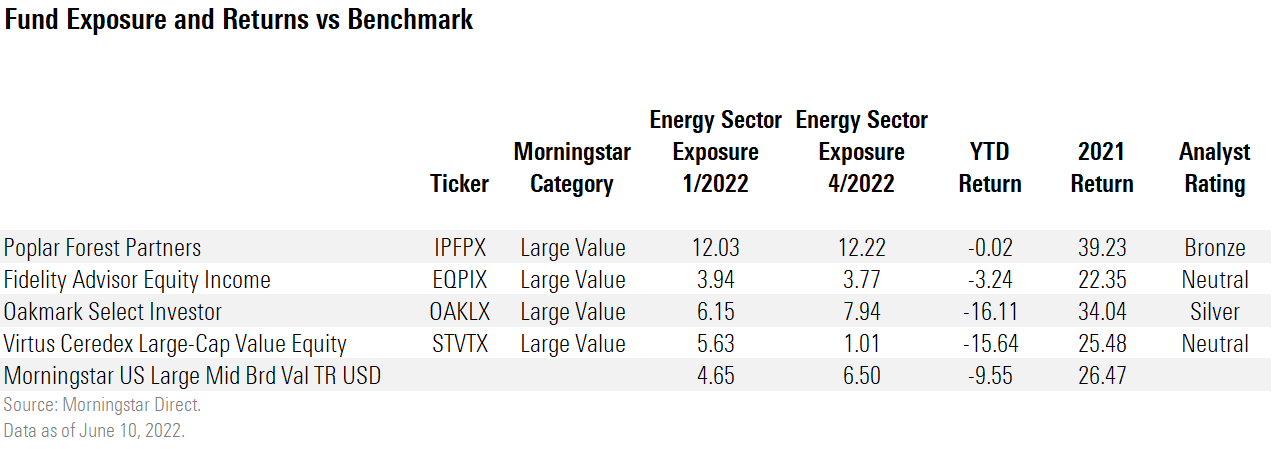

Poplar Forest Partners IPFPX was in the sixth percentile in the large-value category for the year to date through June 10. Like many other top performers, the fund benefited from an above-average allocation to energy. The top three largest contributors to its returns this year have been Chevron CVX, Murphy Oil MUR, and National Fuel Gas NFG. The fund also benefited from strong technology stock picks, notably DXC Technologies DXC and International Business Machines IBM.

The fund has a deep-value approach that isn't for the faint of heart. "Poplar Forest Partners' extreme volatility can try the patience of even the most risk-tolerant investors, but veteran manager J. Dale Harvey's aggressive style has shown it can be effective over a full market cycle," writes Morningstar manager research strategist Alec Lucas. The fund earns a Morningstar Analyst Rating of Bronze.

Fidelity Advisor Equity Income EQPIX lands in the 13th percentile despite an underweight in energy. Fidelity made up for this with strong healthcare picks. Four of them are up more than 20% so far this year: McKesson MCK, Organon OGN, Bristol-Meyers Squibb BMY, and AbbVie ABBV.

The Neutral-rated fund, run by John Sheehy, has stuck to its mandate and invests in more high-dividend-paying stocks than nearly all funds in the large-value category. However, the fund "has yet to show tangible advantages. It has posted mostly middle-of-the-road results on Sheehy's watch and hasn't typically shown superior resilience to most of the large-value category's highest-yielding funds during market pullbacks," writes Morningstar strategist Robby Greengold.

Bottom Performers

Oakmark Select OAKLX has underperformed in 2022 despite a relatively heavy stake in energy. The fund, which is in the 98th percentile for the year to date, was hurt by stock selection in the communication-services sector.

The fund had a concentrated stake in four holdings in that sector, Netflix NFLX, Meta Platforms FB, Charter Communications CHTR, and Alphabet GOOG, all of which were down over 20%. Netflix and Meta struggled the most, losing 67.0% and 43.3%, respectively.

Large swings are not abnormal for the Silver-rated fund run by Bill Nygren, points out Morningstar director Katie Rushkewicz Reichart in her analyst report. The strategy, which she describes as boom-and-bust, is suited only for long-term investors. "The strategy should get back on track, but investors must be aware of what they're signing up for: volatility, but also potentially big returns, as we've seen before," she writes.

Virtus Ceredex Large-Cap Value Equity STVTX is also one of the bottom performers in 2022 among the large-value funds covered by Morningstar analysts.

The fund has a relatively low stake in energy, and it also struggled with stock selection, specifically in the industrials sector. Stanley Black & Decker SWK (down 35.9%) and Vertiv Holdings VRT (down 56.2%) were the largest detractors. The Neutral-rated fund, run by Mills Riddick, has had some stock-picking success historically, specifically in the tech sector. However, absolute and risk-adjusted returns have been lukewarm over trailing periods and Riddick's nearly three-decade tenure. In addition, "fees haven't helped," writes analyst Drew Carter. "Across share classes, asset-weighted fees [were] higher than 81% of peers" as of March 2022.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IGTBIPRO7NEEVJCDNBPNUYEKEY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HDPMMDGUA5CUHI254MRUHYEFWU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/d8236d6f-dcec-4d1b-b5ba-e086adefd364.jpg)