4 min read

Real Asset Investment Strategies Performance in 2024

The typical real asset strategy may seize on inflationary tailwinds in certain market conditions, but those results remain unproven over longer time horizons.

Diversified real asset strategies are a heterogeneous group of multi-asset funds that target equities, bonds, and alternatives in industries that are traditionally resilient in the face of rising inflation. We measure inflation by the Consumer Price Index.

In an earlier post, we listed our search criteria for real-asset strategies in Morningstar Direct:

- Open-end and exchange-traded funds domiciled in the United States.

- Long equity asset allocations below 85%.

- Long bond asset allocations below 85%.

- Long US Treasury TIPS percentages below 50%.

- Long commodity percentages below 50%.

- Long equity allocations below 50% for each of the following sectors: basic materials, energy, industrials, real estate, and utilities.

Using those criteria, we identified a sample group of real asset funds:

- DWS RREEF Real Assets (AAAZX)

- Principal Diversified Real Asset (PDRDX)

- Cohen & Steers Real Assets (RAPIX)

- Wilmington Real Asset

- Delaware Global Listed Real Assets (DPREX)

- Hartford Real Asset (HRLYX)

- PGIM Real Assets (PUDZX)

- Brookfield Real Assets Securities

- Lazard Real Assets

- Virtus Duff and Phelps Real Asset (PDPAX)

Note that Brookfield Real Asset Securities has closed, but its data for periods prior to April 2024 is still relevant for measurements of performance for the sample group. Here, we explore changes in investor preferences and total assets under evolving inflationary conditions

Ebbs and Flows of the Niche Real-Asset Strategies Group

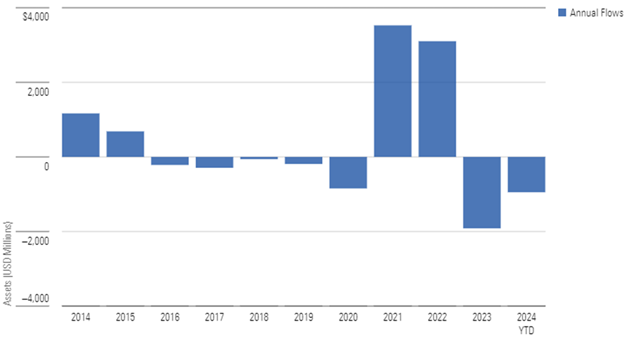

With limited inflationary pressure, diversified real asset strategies saw little investor attention from 2014 to early 2020. As the coronavirus-driven selloff roiled markets and prices surged, investors sought ways to avoid inflation. The chart below demonstrates the shift in sentiment for our sample group of real asset funds as flows skyrocketed post-2020.

Annual flows of real asset funds in the sample group above. Source: Morningstar Direct, author’s calculations, and surveyed data. Data as of June 30, 2024.

Diversified real asset funds saw inflows in 2021 and 2022 that eclipsed the preceding years. However, the course reversed in 2023, with net outflows largely undoing the trends of the prior year. While inflation persisted, investor interest did not.

Fund launches and closures add little to the story, with only a handful of real asset strategies launching or closing in the last decade. Most of the currently active funds in our sample group have been around for more than 10 years, with two passing the 20-year mark.

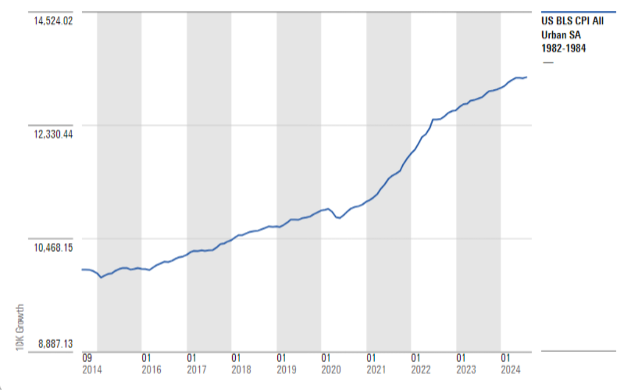

Measuring Inflation With the Consumer Price Index

As real asset funds typically target total returns via inflation-sensitive securities, their excess returns relative to the Consumer Price Index are a good measure of their performance. Here, we used the US Bureau of Labor Statistics CPI All Urban Seasonally Adjusted. The last decade demonstrates a good testbed as well, with markets experiencing low and high rates of inflation since 2014.

The growth of CPI shows a drastic shift in inflationary conditions.

With the interactive charts feature in Direct, we constructed a growth chart for CPI in the relevant period, 2014 through 2024. Data as of June 30, 2024.

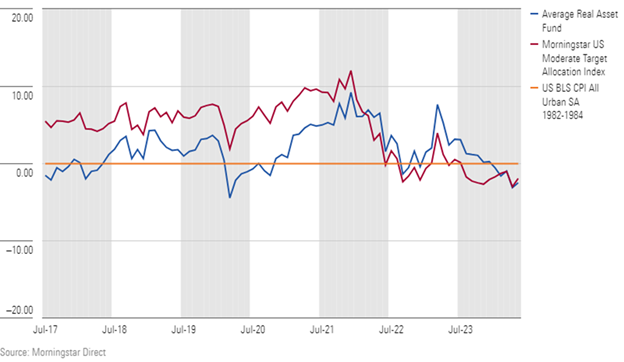

The typical real asset strategy demonstrated a capability to seize tailwinds from inflationary pressures, with average returns outpacing CPI in the second half of 2020 as broader markets rebounded from the coronavirus-driven selloff.

By March 2022, the real asset peer group started to outpace the excess returns of the Morningstar US Moderate Target Allocation Index, representing traditional 60% equity/40% bond portfolios. However, the real asset cohort did not maintain its trajectory.

Inflation persisted through 2022, but the excess returns of the typical real asset fund diminished. In the first quarter of 2023, real asset strategies benefited from a broader equity rebound, due to the typically high equity allocation of their portfolios, which also buoyed the index. However, as inflationary conditions continued through the rest of 2023 and into 2024, the typical real asset fund struggled to keep up with CPI.

The average 3-year rolling excess returns of the real asset strategy sample group in relation to CPI from July 2014 through June 2024. Source: Morningstar Direct. Data as of June 30, 2024.

Morningstar data shows how the typical real asset strategy may seize on inflationary tailwinds in certain market conditions, but those results remain unproven over longer time horizons. Using the same tools, we can readily recreate these charts to measure the performance and flows of other investment peer groups.