In recent years, investors have increasingly purchased mutual funds through new share classes, which jettison two potential sources of traditional conflicts of interest: explicit fees for distribution and front-end loads that are shared with brokers.

While the changes are mostly positive, these new share classes expose investors to a different kind of conflict, which is becoming increasingly harder for regulators and the public to evaluate when compared with the traditional conflicts of interest. These modern conflicts mostly involve revenue sharing—the practice of a fund sharing money with broker/dealers in an opaque way and in a variety of different arrangements.

The SEC has introduced a new rule, Regulation Best Interest, into the mix, which takes effect in June 2020. The rule will require brokers to mitigate conflicts of interest. So, what do we know about these modern conflicts of interest? What could Regulation Best Interest mean for brokers and asset managers when it goes into effect?

What we know about revenue-sharing arrangements

Despite changes in industry practice, the SEC has not historically focused on revenue-sharing arrangements, but rather on the once-typical practice of paying for distribution out of the expense ratio. Even though revenue sharing has not been heavily scrutinized, it has the potential to create a variety of distortions in the advice investors receive from brokers. Furthermore, because of the lack of focus, the disclosures on revenue sharing are very limited; they are presented in an open-end format that stifles efforts to summarize and quantify the wide variety of potential conflicts of interest they create.

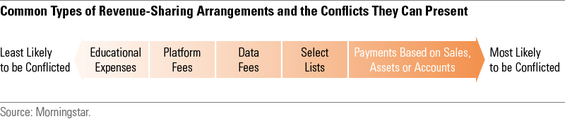

In our latest white paper on Regulation Best Interest, we examined the limited disclosures on these conflicts and found that not all revenue-sharing payments create problems. We broke down the kinds of revenue-sharing payments—from the least likely to those most likely to create conflicts of interest. Most importantly, we discovered that the degree to which any revenue-sharing arrangement creates a conflict depends on the magnitude of the payments and the degree to which the payments are directly tied to sales, as shown below.

What does Regulation Best Interest mean for conflicts in fund distribution?

Despite historically low levels of scrutiny, recent regulatory developments may force changes in revenue sharing as brokers work to mitigate conflicts of interest to comply with Regulation Best Interest. Brokers now will have an obligation to mitigate and disclose the kinds of conflicts that revenue sharing can create, and certain arrangements will most likely receive scrutiny as the regulation goes into force. Revenue sharing may, but need not, create a conflict of interest for brokers when recommending one fund over another.

3 categories of conflicts that brokers should evaluate given Regulation Best Interest

- Payments based on sales or assets: First, consider the sales contests, bonuses, and payments tied to the volume of sales or total assets in a fund where brokers are incentivized to recommend a fund for reasons other than it being in a particular client’s best interest. The SEC has explicitly prohibited sales quotas and bonuses tied to product sales. We believe that any incentives for individual brokers to meet certain volume or asset goals for funds are similar explicit conflicts. These conflicts, as required by Regulation Best Interest, would have to be eliminated altogether or disclosed and mitigated. It’s difficult to imagine how intermediaries could mitigate such inducements.

- Payments for services: At the other end of the spectrum are payments for services, particularly ones that brokers charge to all fund sponsors who are operating on their platforms. Such fees could be called platform fees or access fees, and they act similarly to the distribution fees paid as part of a fund’s expense ratio. Education, training, and conference expenditures to teach brokers about products also may not create a conflict unless they are viewed as rewards for achieving certain fund-sales targets—it then becomes an issue for brokers to recommend fund products with these perks. If education and training is provided simply to inform brokers, then brokers may be more likely to recommend funds with which they are more familiar through such training. Whether or not, and to what extent, these kinds of payments may create a conflict will vary on a case-by-case basis, as will the need to mitigate them. Also, the SEC’s response to these conflicts will most likely vary based on facts and circumstances.

- Payments for recommended or preferred funds: The third category of payments are those paid for by asset managers, including funds within recommended or preferred lists, or as part of robo-platforms. These inclusions are intended to drive more flows to these funds. If, however, funds are more likely to be recommended to clients based on the fees and without consideration of the client’s needs, then these payments will clearly create a conflict. Intermediaries and brokers will need to assess their policies and evaluate which funds will be placed on their recommended lists as they consider complying with Regulation Best Interest.

Next steps for the SEC

Regulation Best Interest will both challenge and alter the industry in its fund-distribution practices. It will also provide the commission and the public with tremendous amounts of data through the client-relationship summary and broker disclosures. As a next step, we encourage the SEC to gather more data on inducements to allow for empirical analysis of its effects. The narrative disclosures in Form ADV are difficult to systematically compare across fund sponsors. Broker disclosures will also be in different forms and in different locations. We also encourage the standardization of such disclosures, specifically around magnitude, circumstances warranting payment, and the exact split between the intermediary and the fund complex. This will help investors and will allow third parties to assess the effects of such payments on recommendations and investor performance.

To learn more about the impact Regulation Best Interest may have on brokers, watch our on-demand webinar or discover how we can help.