Be Thankful That You Don't Compete Against Vanguard

The industry leader sets a high bar for its rivals.

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

The Champs Last week, Morningstar published its semiannual Morningstar Fund Family 150 report. (Highlights of the paper are free to those who submit their information. For a briefer overview, see this post from Morningstar's Bridget Hughes.) The publication ranks the 150 largest U.S. fund companies from top to bottom. The current installment places Dodge & Cox first, and City National Rochdale dead last.

Dodge & Cox has indeed been impressive. The organization boasts several attributes. Its funds are cheap; its managers have long tenures and invest heavily in their own charges; and, unlike most competitors, Dodge & Cox has never launched a fund that it later liquidated. The firm’s backyard contains no skeletons.

(Unsurprisingly, Dodge & Cox is a private partnership. Long ago, Vanguard founder Jack Bogle argued that, aside from his own company’s at-cost structure, partnerships were best suited to run mutual funds. As they need not generate annual cash flows to satisfy outside shareholders, partnerships can be patient, keeping their funds’ expenses modest and creating new funds only when ready.)

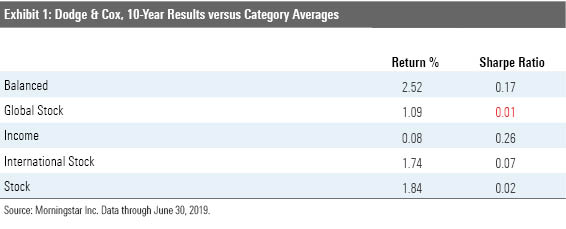

Strong Results None of which would matter if Dodge & Cox funds did not also perform well. That, they do. The chart below shows the 10-year relative performance for the five Dodge & Cox funds that have existed that long (a sixth, Dodge & Cox Global Bond DODLX, began operations in 2014). The comparison is against the relevant Morningstar Category averages.

The tale is straightforward. Every Dodge & Cox fund has outgained the average competitor over the past decade, mostly by large amounts. (The four Dodge & Cox funds that have 15-year records have also comfortably beaten the norms.) The risk-adjusted Sharpe ratio comparisons are closer, as the firm’s funds tend to be somewhat more volatile than most, but Dodge & Cox nonetheless prevailed four times out of five, with the sole exception being by a single basis point.

The news is even better than first seems. For one, although academic theory states that performance should be risk-adjusted, investors tend to pay greater attention to unadjusted returns--not without reason. Academic theory assumes the use of leverage, but few mutual fund owners will ever borrow to purchase more shares. They therefore may be pardoned for favoring the bottom line--which has been Dodge & Cox’s strength.

For another, these gains come largely after the fact. In January 2011, Morningstar debuted its Analyst Ratings. At the time, Dodge & Cox managed five funds. All five received the top Morningstar Analyst Rating of Gold, and all five have been rated Gold ever since. (Global Bond, the sixth, was rated Bronze when it was launched, and has since been upgraded to the second-highest rating of Silver.) The Fund Family 150 analysis, for the most part, consisted of foresight rather than hindsight.

This is how the fund industry is supposed to work. Dodge & Cox established topnotch investment practices; Morningstar’s analysts spread the word; and the funds subsequently justified both Dodge & Cox’s efforts and Morningstar’s opinions. (Unfortunately, investors have not been entirely convinced, as they have steadily redeemed the company’s Dodge & Cox Balanced DODBX and Dodge & Cox Stock DODGX funds.)

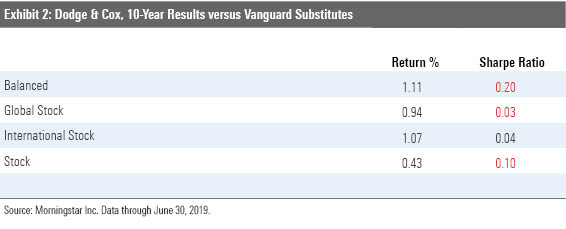

Plan V But … it must be said … another path led to a similar end: buying Vanguard. No Vanguard funds share Dodge & Cox Income's DODIX category, so that fund must be set aside. However, the four remaining Dodge & Cox funds that possess 10-year records have obvious Vanguard counterparts. Three Vanguard index funds can substitute for Dodge & Cox Balanced, Dodge & Cox Global Stock DODWX, and Stock, while actively managed Vanguard International Value VTRIX auditions for Dodge & Cox International Stock's DODFX slot.

The comparison between the Dodge & Cox and Vanguard funds appears below. Positive showings for Dodge & Cox appear in black, while underperformances show red. (Not that it much matters, because their expense ratios are much the same, but Vanguard’s figures are for the company’s Investor shares, as opposed to the lower-priced Admiral or Institutional share classes.)

Vanguard wins the risk-adjusted battle, while Dodge & Cox retains its total-return title. Thus, given my preference for total returns as the prime measure of success for nonleveraged portfolios (assuming the same asset class and roughly equal levels of risk), I give Dodge & Cox the overall nod. However, the contest was close. In none of the four cases would the Vanguard buyer have suffered anything more than modest regret.

And this, of course, was a rigged competition. It pitted the handful of funds that a boutique decides that it is qualified to manage, against randomly selected funds from a company that positions itself as a supermarket. The boutique must win such a contest. After all, if its specialized funds can’t beat the giant’s standardized offerings, then what purpose does that company serve?

As the top-rated family, Dodge & Cox passed the test, albeit not overwhelmingly. You can guess how things look further down Morningstar’s list. Never mind the bottom-fishers, which combined high fees and portfolio-manager turnover with poor performance. They are hopeless cases. The real problem for the fund industry lies in the middle. Those organizations also haven’t justified their existences. Some will do so during the next decade, but who today can say which companies those will be?

Hard to Beat To be sure, Vanguard has enjoyed a tailwind. In general, bigger investments have been better during the Teens, or whatever it is that we will end up calling this decade. The largest of all stock markets has dominated; within that market, blue-chip growth companies have led the way; and alternative strategies have waned. What's more, returns have been consistently positive. One couldn't ask for better conditions for Vanguard's mainstream, fully invested portfolio strategies.

At the same time, credit must be given: This company hasn’t rested on its laurels. It became the largest mutual fund company by outcompeting its rivals, and it’s not showing any signs of slowing. Sometimes, the decline is obvious. For example, General Motors GM in the 1970s. My father bought one Chevy that shed a door handle at 900 miles, then another one that blew out a carburetor at 500 miles. Taking market share from the 1970s version of GM was easy. Taking market share from 2019 Vanguard, on the other hand, is a challenge indeed.

Note: After reading this column, Morningstar's Russ Kinnel informed me that Jack Bogle told him that Dodge & Cox was his favorite fund family. "My God, they're boring," said Bogle. You can't ask for a higher fund-family compliment than that.

John Rekenthaler has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar's investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/d10o6nnig0wrdw.cloudfront.net/04-25-2024/t_d30270f760794625a1e74b94c0d352af_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/DOXM5RLEKJHX5B6OIEWSUMX6X4.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZKOY2ZAHLJVJJMCLXHIVFME56M.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)