Real Estate: Few Cheap Stocks

Sector is one of the most fairly valued.

/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)

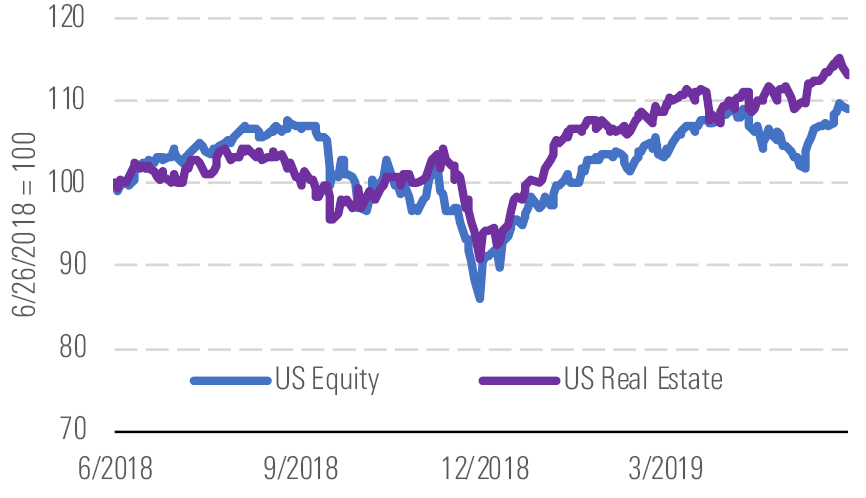

The Morningstar U.S. Real Estate Index rose 18% year to date (Exhibit 1) and is outperforming the broader U.S. equity market (17%), as growing economic concerns have led to declines in interest rates, which make the defensive nature of long-term leases with tenants and the high dividend payouts of REITs more attractive to investors.

Real estate is up and has outperformed the U.S. Equity Index - source: Morningstar Analysts

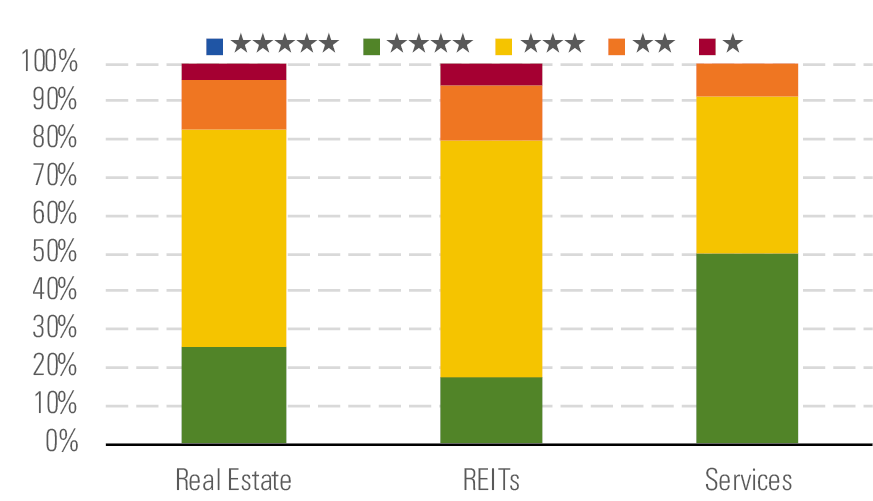

Real estate is one of the most fairly valued sectors. Our coverage currently trades at a 2% discount to our estimate of intrinsic value as opposed to a 4% premium at the end of the first quarter. Considering most of the names fall in the 3-star range, we only see a few attractively priced real estate companies, and no names trade at 5 stars (Exhibit 2).

Sector has mostly 3-star names, but there are some bargains - source: Morningstar Analysts

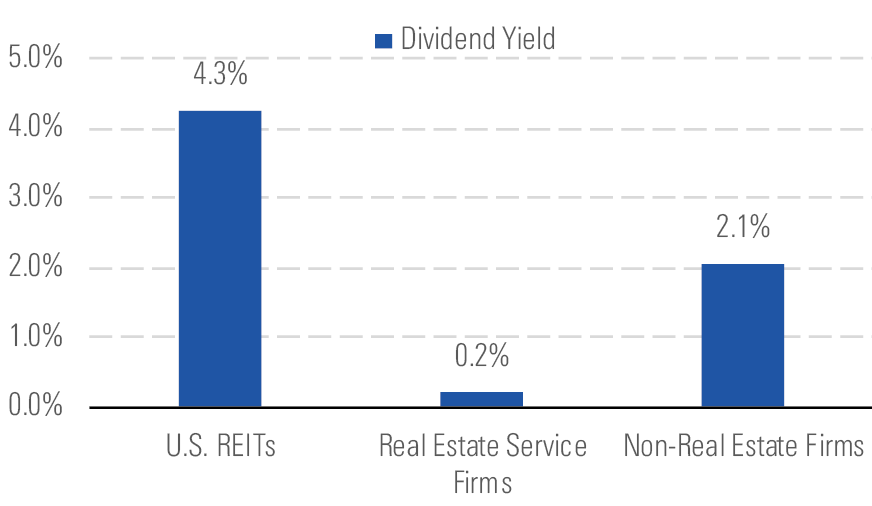

The average dividend for real estate firms is higher than the rest of our coverage (Exhibit 3). To receive tax-free status, REITs are required to pay out most of their net income as dividends to shareholders. These companies are frequently included in portfolios of income-oriented investors. As a result, the yields of REITs are often compared with government bond yields.

REITs have higher dividend yields than service firms and other sectors - source: Morningstar Analysts

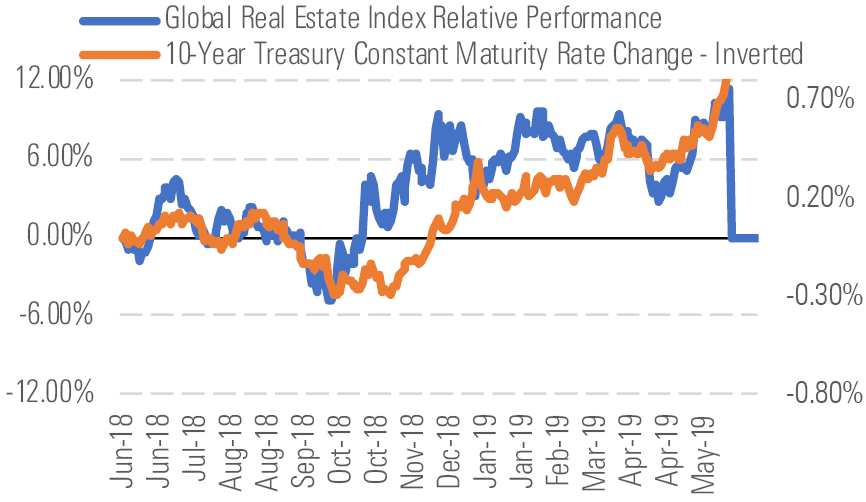

The high dividend payouts make REITs sensitive to changes in interest rates. When the yields of risk-free government bonds rise, REITs' yield spread falls and many income portfolios move from holding REITs to government bonds. Conversely, falling interest rates attract investors looking for more annual income than they can get from government bonds. As a result, the relative stock performance of real estate firms, REITs in particular, will correlate with movements in the risk-free rate.

Movements in the 10-year U.S. government bond have corresponded with periods of real estate outperformance and underperformance. When the interest rate rose 40 basis points in September/October, real estate underperformed by 4%. However, with interest rates dropping almost 120 basis points since November, real estate firms outperformed by about 12%. However, we caution that the relative performance of real estate often mean-reverts during periods of interest-rate stability. While real estate trades in the short term on interest-rate movements, the long-term impact isn't as strong. Therefore, we are cautious that much of the recent outperformance may eventually be given back.

Real estate relative performance has moved in line with interest rates - source: Morningstar Analysts

Top Picks Macerich MAC

Star Rating: 4 Stars

Economic Moat: Narrow

Fair Value Estimate: $57

Fair Value Uncertainty: High

Class A malls continue to outperform other forms of brick-and-mortar retail. Over the past 12 months, Macerich's tenants have produced 8.7% growth in sales per square foot, and occupancy costs dropped to 12.4%, the lowest in six years. This has let Macerich continue to push double-digit re-leasing spreads. The stock has underperformed recently because of several tenant closures that will hurt cash flows in 2019. However, we view these as opportunities to redevelop the assets and replace out-of-favor tenants, which should yield significant returns over the next few years.

Pebblebrook Hotel Trust PEB

Star Rating: 4 Stars

Economic Moat: None

Fair Value Estimate: $36.50

Fair Value Uncertainty: High

Growth for hotels has steadily slowed over the past few years. Despite reaching all-time highs in occupancies, hotel operators have been unable to push prices as online travel agencies dramatically increase price discoverability for consumers. However, Pebblebrook has an opportunity to push net operating income growth higher than its peers over the next few years through expense-savings measures. It acquired LaSalle Hotel Trust, a company Pebblebrook's current CEO previously founded, in 2018, and management believes they know how to drive industry-leading margins out of the acquired portfolio.

Jones Lang LaSalle JLL

Star Rating: 4 Stars

Economic Moat: Narrow

Fair Value Estimate: $181

Fair Value Uncertainty: High

Narrow-moat JLL continues to take share from smaller brokers amid consolidation in commercial real estate services. Although the market seems concerned about how Jones Lang LaSalle might fare in a cyclical downturn, we think its expansion into the more stable facilities management business insulates it somewhat from the potential negative effects of a downturn. We also think investors are attaching an unnecessary valuation premium to peer CBRE because of its larger size. Although we do forecast slightly better growth and margins for CBRE, both firms are similarly positioned to compete for contracts.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/SACNVSNDS5FTTFAEDRHVHNFB7M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/5GAX4GUZGFDARNXQRA7HR2YET4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/Q34JH4TM3JHGRMOWGT7EPZBE3A.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)