As Rising Interest Rates Hit Home, Real Estate Sector Declines

Decline comes despite growth in fundamentals

/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)

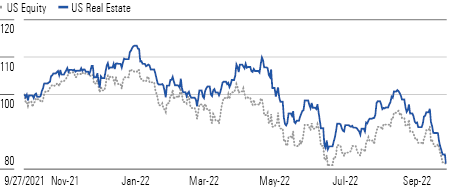

The Morningstar US Real Estate Index is down 18.5% over the trailing 12 months, which is slightly better than the 19.1% decline seen by the broader U.S. equity market over the same period. The real estate sector declined 9.5% in the third quarter of 2022, significantly below the U.S. equity market’s down 3.1%. However, the sector’s negative performance over the past 12 months does not reflect the state of real estate fundamentals, with occupancy continuing to recover from the pandemic lows and high inflation allowing many real estate subsector to drive record level rate increases in the second quarter.

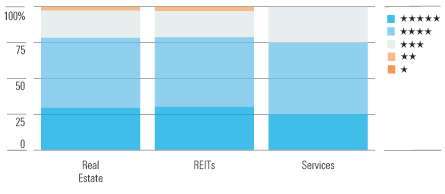

The real estate sector is currently trading below our fair value estimates. Our real estate sector coverage currently trades at a 17% discount to our estimate of fair value, which is in line or better than many other North American sectors. Currently, 78% of the real estate sector is trading in either the 5-star or 4-star range, 19% is trading in the 3-star range, and 3% is trading in the 2-star range while no company is currently trading in the 1-star range.

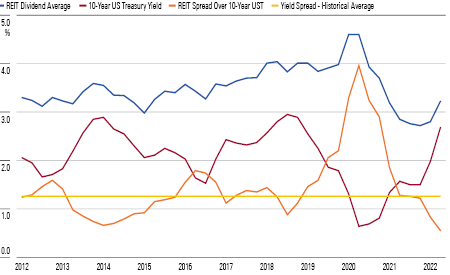

Over the past decade, REITs have provided a dividend yield that is approximately 1.5% higher than the available rate on the US 10-year Treasury. While the spread jumped during the first year of the pandemic as the Federal Reserve lowered interest rates to stimulate the economy while the drop in share prices increased REIT dividend yields, the sector returned to the historical average spread in the second half of 2021. However, the rise in interest rates in 2022 has negatively affected the sector as REITs are not able to raise dividends as quickly as interest rates, so income-oriented investors have reduced their REIT exposure across their portfolios, which has led to a drop in share prices.

Real estate declines have been roughly in line with the broader market.

- source: Morningstar Analysts

Majority of Stocks in Real Estate Sectors Trade at a Discount to our Fair Value Estimates.

- source: Morningstar Analysts

Rising Rates Fuel Decline in Sector's Performance Despite Strong Fundamental Growth

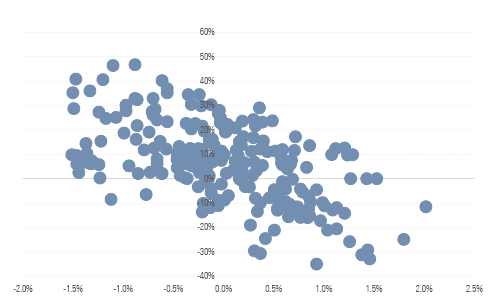

Since 2000, the relative performance of REITs compared to the broader equity market has shown a significant negative relationship to interest rate movements for the 10-year U.S. Treasury. This trend has continued in 2022, with announcements of rising rates leading to REITs underperforming the broader equity market. However, despite the short-term negative stock price performance for REITs caused by income-oriented investors rotating out of the sector, interest rates have little impact on the long-term cash flows generated by most REITs. While acquisition activity might slow as debt becomes more expensive, we believe the impact to long-term fair value estimates is small. Therefore, we believe the short-term disruption to the sector has created significant discounts for investors looking to increase their real estate exposure.

REIT dividends historically have been 1.25% above the 10-Year UST rate.

- source: Morningstar Analysts

REIT relative performance is negatively correlated with interest rates.

- source: Morningstar Analysts

Top Picks

Simon Property Group SPG Star Rating: ★★★★★ Economic Moat Rating: None Fair Value Estimate: $160 Fair Value Uncertainty: Medium

Class A malls continue to outperform other forms of brick-and-mortar retail. While the stock sold off significantly during the height of the pandemic, it recovered to prepandemic levels by the end of 2021 as brick-and-mortar sales rebounded with consumers returning to shop in store. Tenants are now much healthier with occupancy costs at the lowest levels in over 6 years, which should allow Simon to see further occupancy and rent increases. Additionally, Simon recently acquired Class A mall competitor Taubman Centers, which should increase cash flows and provide more leverage when negotiating with tenants.

Park Hotels & Resorts PK Star Rating: ★★★★★ Economic Moat Rating: None Fair Value Estimate: $28 Fair Value Uncertainty: High

While the coronavirus significantly affected Park's operating results with high-double-digit revPAR declines and negative hotel EBITDA in 2020, the company's portfolio started to recover in 2021 that has carried into 2022. Leisure travel has rebounded to near pre-pandemic levels, leading to a return of positive hotel EBITDA. Additionally, business and group travel have shown recent signs of improvement in 2022. We think business and group demand will eventually return close to pre-pandemic levels by the end of 2024, leading to years of strong growth for Park.

Ventas VTR Star Rating: ★★★★★ Economic Moat Rating: None Fair Value Estimate: $25 Fair Value Uncertainty: Medium

Ventas owns high-quality assets in the senior housing, medical office, and life science fields. While the company’s medical office and life science portfolios should be relatively unaffected by either the pandemic or a potential recession, the senior housing portfolio saw a large drop in occupancy in the first year of the pandemic as the coronavirus has the highest lethality rate among senior citizens. However, occupancies have slowly recovered in 2021 and 2022 and the industry should see strong long-term growth from the coming wave of baby boomers aging into senior housing facilities.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/T5MECJUE65CADONYJ7GARN2A3E.jpeg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/VUWQI723Q5E43P5QRTRHGLJ7TI.png)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_ffc6e675543a4913a5312be02f5c571a_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/b9459b20-3908-4448-a36c-b728946ddbe5.jpg)