Should I Buy Tesla Stock Now?

We take a fresh look at Tesla with updated projections for electric vehicle adoption and higher profitability.

/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)

Tesla’s TSLA stock value is not determined by how many cars it will sell this year or next, or by some multiple of next year’s sales or earnings. The value is determined by estimating the present value of the free cash flow stream that Tesla will generate over its lifetime.

The auto industry is set to undergo a rapid transition over the next 10 to 20 years as battery electric vehicles, or BEVs, increase as a percentage of new car sales and internal combustion engines, or ICEs, are phased out. Tesla’s stock value will be determined by how much market share the firm will be able to maintain of this growing share as legacy auto manufacturers roll out their own BEVs. In fact, the value is not just in revenue growth but also in how profitably Tesla can sell vehicles.

But Tesla is not just an auto manufacturer. It has several other business lines such as subscriptions for autonomous driving and energy generation and storage as well as startup technologies. These ancillary businesses will also generate economic value over the long term and must also be analyzed and valued based on their long-term prospects.

The greater the growth potential over the long term, the higher the valuation. Yet, the value of a stock also becomes more volatile as the valuation is dependent on the assumptions driving the long-term forecasts.

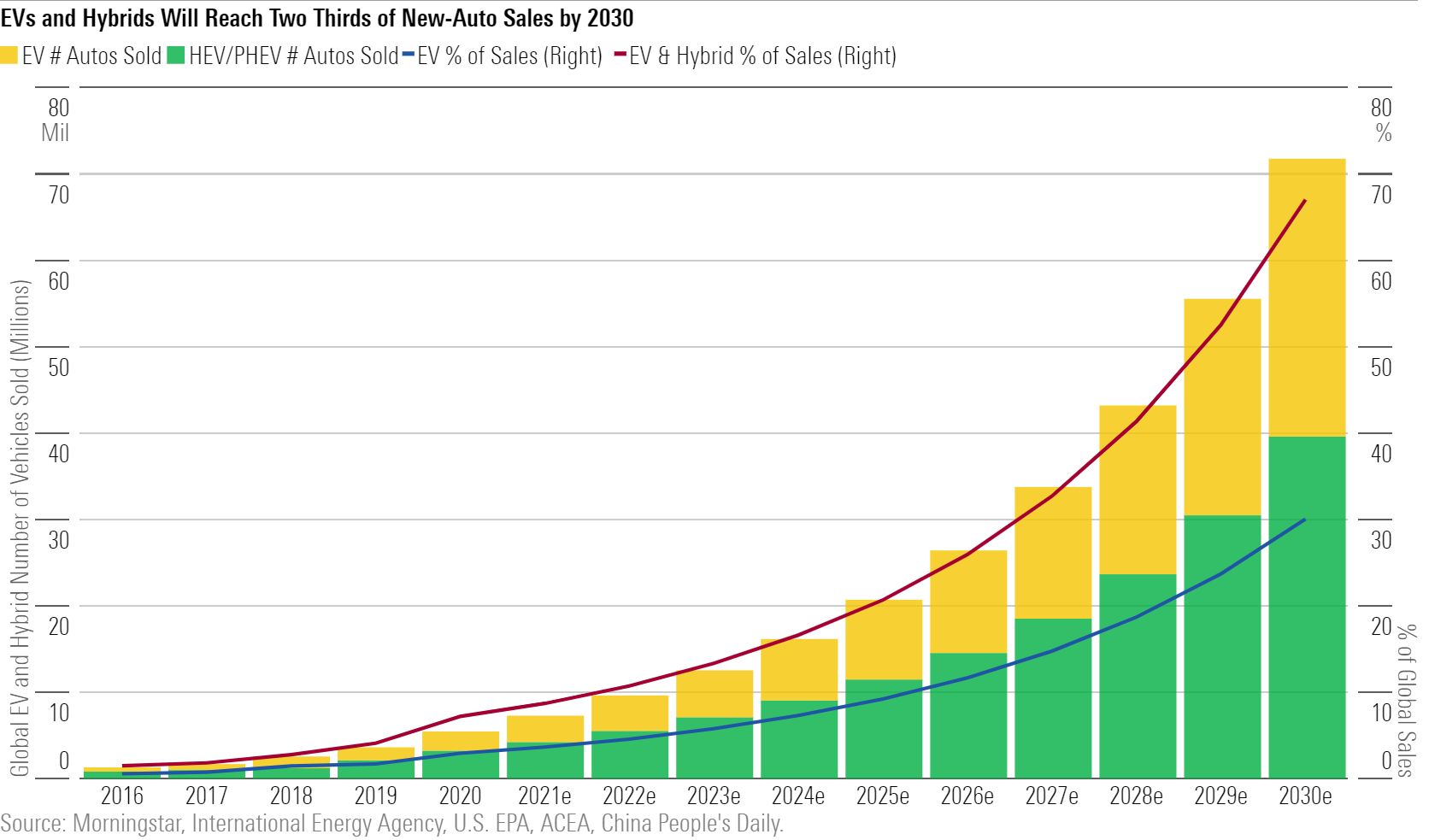

Tesla: Our Long-Term Assumptions

At the end of June, we significantly increased our valuation for Tesla after taking a fresh look at both our projections for the adoption of electric vehicles, or EVs, and Tesla’s profitability. Subsequently, we have bumped up our fair value even further following second-quarter earnings and Tesla’s AI Day.

In 2020, BEVs only accounted for approximately 3% of global auto sales. In our updated projections, as shown on the chart below, we estimate that number will jump to 30% by 2030--a significant increase from our prior projections of 20%.

Of the remaining new auto sales, we estimate hybrids will be 37% of sales and ICEs will be 33%. In our prior projections, these numbers stood at 30% and 50%, respectively. The increased adoption rate of electric vehicles stems from the re-evaluation that they will become cheaper for entry-level cars and reach performance parity with ICEs by 2025. In addition, as even more charging infrastructure is built across China, Europe, and the United States, EV adoption will accelerate in the second half of this decade.

In our financial model, we project that Tesla’s auto deliveries will increase from

- 500,000 in 2020,

- 845,000 in 2021,

- 1,202,000 in 2022,

- ultimately to over 5,400,000 in 2030.

This level of auto deliveries in 2030 equates to around 5% of global share of the auto market. That level of market share would place Tesla well into the top 10 largest global auto manufacturers today. Within the BEV space, this level of deliveries would equate to approximately 16% of the global market share in 2030.

In addition to increasing the unit sales projection, we forecast that Tesla will be able to boost its gross profit margins in the automotive business to 37.2% in 2030 from 26.6% in 2020. The basis for the gross margin improvement is a combination of improved efficiencies as production scales up, our assumption that Tesla will be successful in its efforts to reduce its cost of batteries, and our forecast that Tesla will sell a growing number of high-margin autonomous driving software subscriptions. As such, our forecasted operating margin for the next five years increases to 14.4% from 6.3% in 2020.

As comparison, our forecasted operating margin for the next five years of several other large global auto manufacturers ranges from:

- as low as 3.7% for Ford F and 5.3% for GM GM,

- to as high as 9.9% at BMW BMW and 8.8% at Volkswagen VOW,

- and 8.0% at Toyota TM.

Among Tesla’s other business lines, we forecast that services sales will grow in proportion to auto sales with a 10-year compound annual growth rate of 26%. In the energy generation and storage segment, we forecast growth from $2 billion in revenue in 2020 to $7.2 billion in revenue in 2030, representing a compound annual growth rate of 14%.

We project that Tesla’s vehicle sales will be $39.5 billion (84% of total revenue), services and other sales will be $3.7 billion (8% of total revenue), and energy generation and storage will be $3.7 billion (8% of total revenue) in 2021.

Determining Tesla’s Intrinsic Value: A Brief Synopsis of Our Discounted Cash Flow Model

While many investors will use metrics such as price/earnings or enterprise value/sales to estimate the value of a stock, these simplistic calculations are unable to properly measure the intrinsic value of a stock such as Tesla.

To capture both the timing and profitability of the long-term growth dynamics, a discounted cash flow model is needed. Our discounted cash flow model consists of three stages:

- I: explicit forecast period in which we use a standardized model to project the income statement, balance sheet, and statement of cash flows based on the underlying assumptions to drive revenues, margins, and sources/uses of cash

- Stage II: interim period to normalize our forecasts after the end of the explicit forecast period to those that we think are indicative of the long-term competitive outlook for the company

- Stage III: terminal value of the company

Our model for Tesla includes:

- Stage 1: a 10-year explicit forecast period using the assumptions discussed earlier

- Stage II: a five-year period with return on new invested capital of 60% and earnings before interest growth of 10%

- Stage III: a perpetuity formula based on the year-15 cash flows

In addition, we use a 9% cost of equity to discount the cash flow stream to today’s value, which plays a pivotal role in the ultimate valuation. All else equal, lowering to a 7.5% cost of equity would increase our fair value to $795 and, conversely, increasing cost of equity to 11% would lower our fair value to $440.

Tesla’s Stock Valuation

Our current fair value estimate for Tesla’s stock is $600 per share. With the stock currently trading at $701, we rate the stock with 3 stars, which means we think the stock is fairly valued, although we note that it is trading on the higher end of our fairly valued range.

Considering the bulk of Tesla’s stock value is dependent on its future growth rates, our Morningstar Uncertainty Rating is Very High. Tesla’s stock price is highly volatile, with a 52-week trading range from $330 to $900. We’d expect that this volatility will continue and that better entry points in the future will provide investors with an adequate margin of safety.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F2S5UYTO5JG4FOO3S7LPAAIGO4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZZNBDLNQHFDQ7GTK5NKTVHJYWA.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/HE2XT5SV5ZBU5MOM6PPYWRIGP4.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/54f9f69f-0232-435e-9557-5edc4b17c660.jpg)