Coronavirus Crisis Highlights Need for Stakeholder Capitalism

Sustainable investing can help bring it about.

/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)

Editor’s note: Read the latest on how the coronavirus is rattling the markets and what investors can do to navigate it.

The global pandemic we're struggling with today, unimaginable in its breadth and depth just two months ago, underscores the need for a more resilient, inclusive, and just economy. We need a new operating system, wrote Martin Whittaker, CEO of JUST Capital last week in Forbes, one in which:

"business drives value for all stakeholders, where long-term systems thinking supplants short-term opportunism, and where as many people as possible have a stake in the recovery."

The old shareholder primacy model “is no longer fit for purpose,” says Whittaker. That’s because companies with a narrow focus on short-term profit maximization do so at the expense of long-term value creation, which ultimately imposes significant costs on shareholders and society. The result, already apparent prior to the pandemic, has been lower productivity and growing inequality, the latter worsened by holes in the social safety net.

The very nature of the pandemic is forcing companies to focus on their stakeholders, especially their employees, but also their customers and communities. Those that don't rise to the occasion will find it harder to recover, argues Jessica Alsford, head of sustainability research at Morgan Stanley:

"Corporate behavior in a time of crisis--both in how companies treat employees and customers, and their impact on society in a time of need--can have lasting implications, both positive and negative. These factors can be linked to long-term performance and returns."

When companies do things like increase healthcare benefits, hike pay for workers on the front lines, lower executive compensation to help avoid layoffs, and take extra steps to protect worker and customer safety, they will benefit from having a more engaged and productive workforce and a more loyal customer base during a recovery.

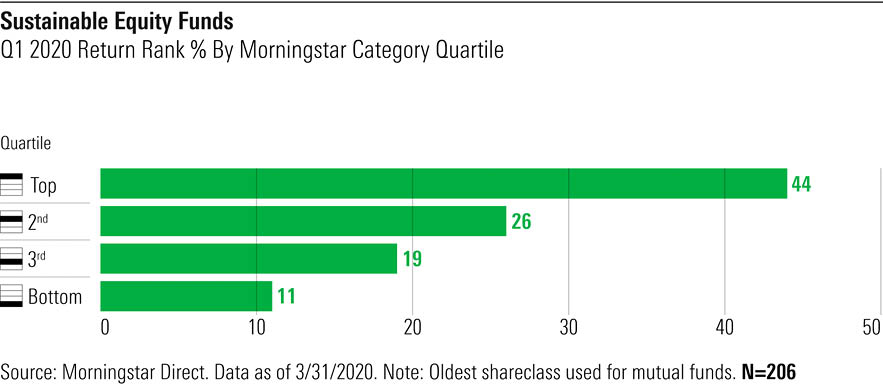

What Does All This Have to Do With Sustainable Investing? Importantly, companies that are doing the kinds of things outlined above tend to be the types of companies that do well on the various environmental, social, and governance evaluations and ratings scheme used in sustainable investment strategies. Sustainable funds clearly outperformed during the first quarter, with 70% finishing above the median in their peer groups and 44% finishing in the top quartile compared with only 11% in the bottom quartile.

Nearly all ESG index funds outperformed the closest relevant market-cap-weighted index fund, and the main reason, based on attribution analysis, was their ESG stock selection. (Energy sector exposure--ESG funds were underweight energy, which was the worst-performing sector for the quarter--was a secondary contributor.)

So, I think it’s great that sustainable investing is showing it can deliver competitive performance on an ongoing basis, in both up and down markets, aided by the insights of ESG analysis, but keep in mind the bigger-picture purpose of sustainable investing: It’s about investors helping/encouraging/cajoling companies to move toward a long-term stakeholder-centric model of corporate behavior that is better for people and the planet and will be, over the long run, better for shareholders.

Jon Hale has been researching the fund industry since 1995. He is Morningstar’s director of ESG research for the Americas and a member of Morningstar's investment research department. While Morningstar typically agrees with the views Jon expresses on ESG matters, they represent his own views.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/NNGJ3G4COBBN5NSKSKMWOVYSMA.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6BCTH5O2DVGYHBA4UDPCFNXA7M.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EBTIDAIWWBBUZKXEEGCDYHQFDU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/42c1ea94-d6c0-4bf1-a767-7f56026627df.jpg)