Is Apple Stock a Buy After Its Selloff?

Keeping a close watch on iPhone sales trends.

/s3.amazonaws.com/arc-authors/morningstar/5c8852db-04a9-4ec5-8527-9107fff80c09.jpg)

After a strong rally to start the year, Apple AAPL stock has seen a significant pullback. Shares lost 11.6% during the third quarter, with a nearly 9% drop in September. That selloff comes after Apple’s gain of more than 50% from the start of 2023 through the end of July had taken the stock well into territory considered overvalued by Morningstar. Here’s what we think of Apple stock now that it’s fallen back.

Key Morningstar Metrics for Apple

- Fair Value Estimate: $150.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

What We Think of Apple Stock

Apple’s stock is approaching our $150 fair value estimate, nearing a 3-star rating. We think the first cause for this is a broader pullback in the stock market, with the Morningstar US Market Index down roughly 5% and Apple down 9% over the past month.

On a fundamental basis, Apple announced its iPhone 15 lineup. Early demand signals for these devices appear to be decent, but they don’t suggest the next 12 months will bring massive growth for the iPhone. There is some modest concern about the development of Huawei’s Mate 60 Pro phone in China, as it may gain interest among Chinese consumers. Apple was a clear share gainer at the high end of the market when Huawei was crippled by U.S. sanctions, but now that it appears that Huawei can build a phone while getting around such sanctions, it might be able to claw back some of its market share losses.

On a longer-term basis, we anticipate healthy growth out of Apple’s services and wearables segments, and we’re relatively optimistic about the firm’s innovation and technological expertise. However, we view the company’s core iPhone business as a mid-single-digit grower over the long term. In contrast, when Apple’s stock is trading at $190 or higher, we surmise investors must be assuming Apple will grow at a high-single-digit or even 10%-plus pace, so we don’t think there is an attractive margin of safety for investors when the stock is trading that high.

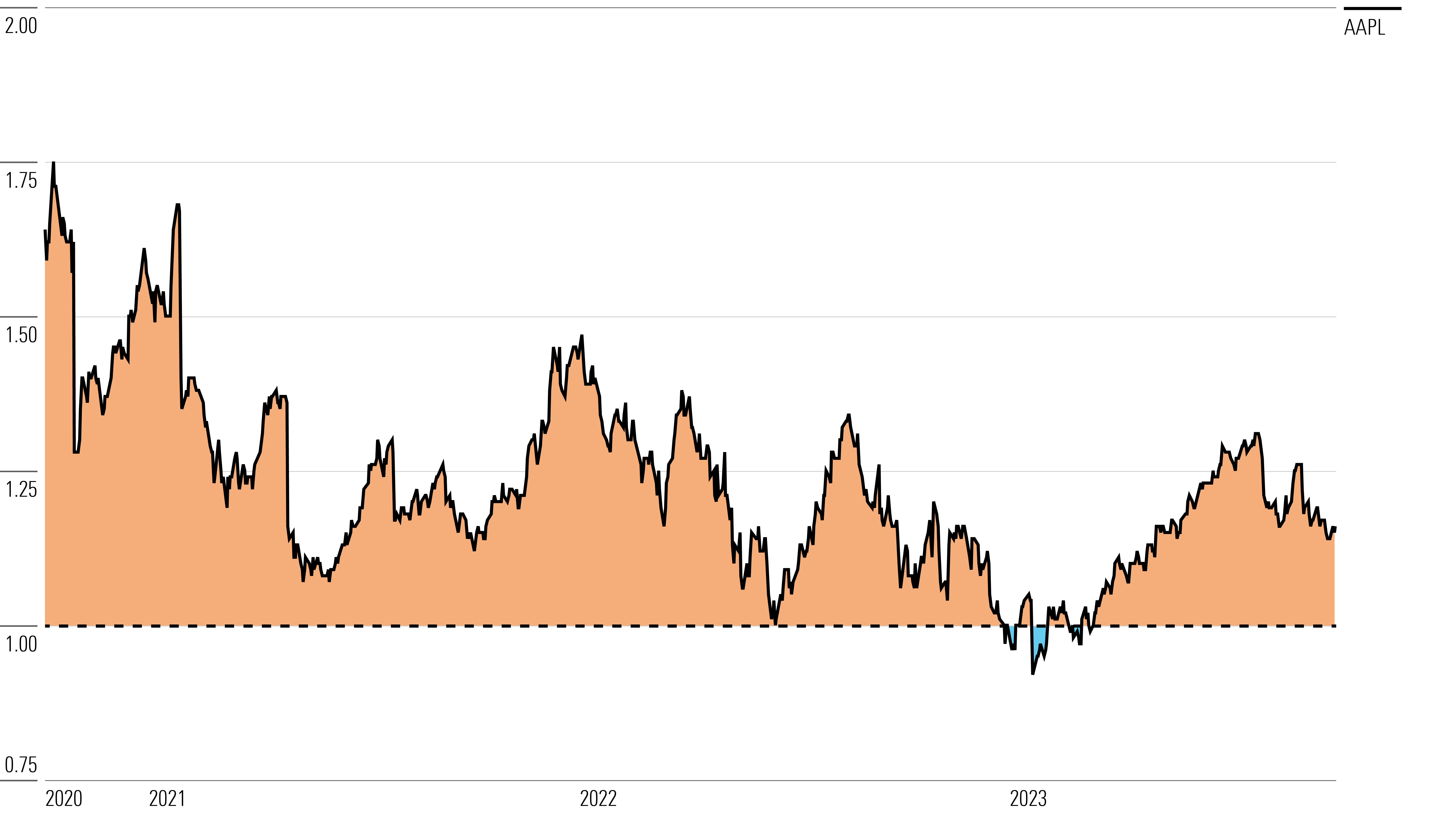

Apple Stock Price

Fair Value Estimate for Apple

With its 2-star rating, we believe Apple’s stock is overvalued compared with our long-term fair value estimate.

Our fair value estimate is $150 per share. Our estimate implies a fiscal 2023 (ending September 2023) price/earnings ratio of 25 times. In fiscal 2023, we expect total revenue to be down 2%, as services growth and flattish wearable revenue will be offset by modest declines in iPhone and iPad revenue and a sharp drop in Mac revenue. We view these declines as reasonable, coming after multiple strong years due to trends in working and learning from home caused by the COVID-19 pandemic.

We model iPhone revenue growth at a 3% CAGR over the next five years, with such growth coming off a strong fiscal 2022, again because of a spike in sales during COVID-19. We anticipate low-single-digit growth in both iPhone unit sales and iPhone average selling prices over our forecast period. We anticipate flattish CAGRs in both iPad and Mac revenue, again off of a strong base in fiscal 2022. We expect services to grow at a 6.5% CAGR over the next five years, as iOS users buy more and more of the firm’s services like Apple TV+, Apple Music, and so on. We model Apple’s wearables, home, and accessories segment to grow at a 17% CAGR over the next five years. We anticipate strong growth in watches and airPods in the years ahead, as well as the launch of an AR/VR headset over the next five years. Our fair value estimate assumes a launch with minimal revenue in fiscal 2024, but growing to an $11 billion business by fiscal 2027.

Read more about Apple’s fair value estimate.

Apple Historical Price/Fair Value Ratios

Economic Moat Rating

We assign Apple a wide economic moat rating because of its combination of switching costs, intangible assets, and network effects associated with its iOS ecosystem. Combined with the company’s asset-light business model, we think it is nearly certain that Apple will generate excess returns on capital over the next decade and more likely than not over the next 20 years.

We think Apple’s primary moat source stems from high customer switching costs, based on a variety of aspects of its hardware, software, and services. First, we think about the risk of customers moving away from today’s electronic devices, such as smartphones. Despite innovations in smart speakers, AR/VR headsets, and the Internet of Things, we don’t see the smartphone going away any time soon. The smartphone has already replaced a host of standalone electronic devices (cameras, MP3 players, portable game consoles, etc.) while emerging as the primary portal with an intuitive interface for many other digital services (email, books, web browsing, shopping, social media, videos, and more) in a pocket-sized form factor. Apple’s iPhone fostered the industry and has maintained its position as the premier smartphone. We expect the firm to increasingly monetize its valuable installed base, with the iPhone as the catalyst.

Perhaps the stickiest aspect of the iPhone is the integration of iOS across multiple devices. Users of ancillary products—including the iPad, Mac, Watch, and AirPods—lose significant functionality when pairing those products with competitors’ smartphones. An iMessage will show up on one customer’s iPhone, iPad, Mac, and Watch. We do not believe these other hardware products are wide-moat businesses on their own, but together with the iPhone, they create a formidable customer lock-in. Wearables such as AirPods and the Apple Watch have also disrupted their respective predecessor industries, and have created another expensive hook to keep customers tied to Apple’s ecosystem. Apple’s active installed base (iPhone, Mac, and iPad) reached 1.8 billion at the end of 2021—up 9% from a year prior—highlighting the growing adoption of multiple iOS products by individuals.

We don’t foresee Apple’s captive user base scaling its walled garden anytime soon. We believe switching costs from iOS are as strong as ever thanks to more auxiliary products and services and greater inertia for users, making switching away from iOS more difficult over time. Regarding intangible assets, Apple’s differentiated user experience via iOS coupled with its expertise in hardware, software, and now semiconductor design allows the firm to build vertically integrated products more seamlessly. We also see network effects around iOS and its 1 billion-plus installed base with new app development favoring iOS. Going forward, we expect Apple to better monetize its captive user base via supplemental products and services that will evolve into a more robust recurring revenue stream. We see no other technology titan with comparable expertise across consumer hardware, software, services, and chip design.

In turn, we believe this integration allows Apple to build premium devices that command industry-leading average selling prices and margins, most notably the firm’s crown jewel: the iPhone. Although Apple’s midteens market share in the smartphone space doesn’t seem excessive, the firm does enjoy the lion’s share of industry profits (we estimate 25% operating margins for the iPhone versus about 10% for Samsung’s mobile device segment). In an industry in which the greatest concern a decade ago was the commoditization of the smartphone, we’ve actually seen Apple lift the average selling prices for the iPhone much higher than those within the Android device space in recent years.

Read more about Apple’s moat rating.

Risk and Uncertainty

We assign Apple a High Morningstar Uncertainty Rating. As the largest firm in the world, it is prone to material competition. Consumer hardware is inherently inclined toward cutthroat competition, as short product cycles and customers hungry for ever-superior features make it difficult to maintain market leadership. Although Apple has done well with its walled garden approach, it competes with Chinese original equipment manufacturers and Samsung across all tiers.

We also suspect many customers are holding onto their phones for longer than before, as premium devices are more than good enough for today’s needs (web browsing, streaming, social media). Analogous to the decline of PCs, Apple faces the possibility of smartphone unit stagnation or even declines once emerging markets saturate or consumers gravitate to mid-tier devices. Should it be unable to innovate, Apple may lose its ability to charge premium prices for hardware that is no longer unique relative to competitor devices.

Read more about Apple’s risk and uncertainty.

AAPL Bulls Say

- Between greater smartphone penetration in emerging markets and repeat sales to current customers, Apple has plenty of opportunity to reap the rewards of its iPhone business.

- The iPhone and iOS have consistently been rated at the head of the pack in terms of customer loyalty, engagement, and security, which bodes well for long-term customer retention.

- We think Apple is still innovating with its introductions of Apple Pay, Apple Watch, Apple TV, and AirPods. Each of these could drive incremental revenue, but more crucially, they could help retain iPhone users over time.

AAPL Bears Say

- Apple’s decision to maintain a premium pricing strategy may help fend off gross margin compression, but it could also limit unit sales growth, as devices may be unaffordable for many customers.

- If Apple were to ever launch a buggy software update or subpar services, it could diminish the firm’s reputation for building products that “just work.”

- Apple is believed to be behind firms like Google and Amazon when it comes to artificial intelligence development (notably Siri voice recognition). This could be problematic as tech firms look to integrate AI when delivering premium services.

This article was compiled by Tom Lauricella

3 Dividend Stocks for October 2023

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/5c8852db-04a9-4ec5-8527-9107fff80c09.jpg)