How Do Rising Rates Impact Stock Returns?

Predicting the winners and losers of the next rate hike is a difficult undertaking.

/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)

A version of this article appeared on Oct. 29, 2015.

Question: I know longer-duration bonds do worse when interest rates rise, but what happens to stocks when rates rise?

Answer: Investors who have a basic understanding of how bond duration works know that rising rates mean bond prices fall. Holding all else equal, investors could reasonably expect higher-quality, longer-duration bonds to sell off when the Fed hikes rates.

However, all else is rarely, if ever, equal. As Morningstar senior analyst Eric Jacobson points out, the bond market doesn't always react to rising rates in the same way because they happen against varying backdrops, and those backdrops can make all the difference.

So, if figuring out what happens to bonds during periods of rising rates is not all that straightforward, it's a good bet that figuring out what happens to stock sectors during periods of rate rises is even less so. As Morningstar StockInvestor editor Matt Coffina pointed out in this interview, all else equal, stock prices should fall when rates rise. That's because you have both direct effects like higher interest expenses and also important indirect effects like a higher cost of equity. That is to say, investors will demand to be compensated even more for holding stocks when bonds become relatively more attractive.

But, of course, it's not that simple. For one thing, the Federal Reserve tends to raise rates during periods when the economy is robust enough to handle a rate increase. As Coffina points out, cash flows also tend to go up during periods when interest rates are rising because the economy tends to be strong during those periods. So, in essence, what we've seen is that stocks tend to do better during periods of rising rates than they do during periods of falling rates.

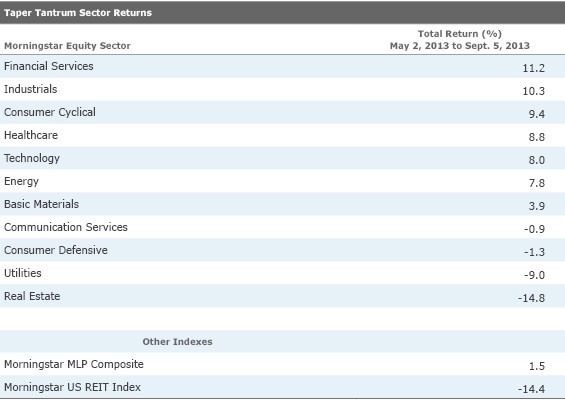

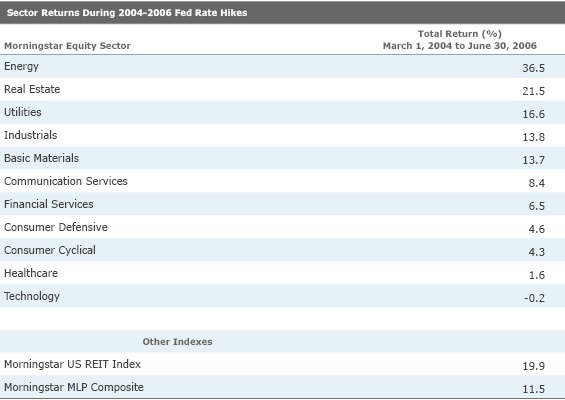

A Look at How Different Stock Sectors Performed During Previous Rate Rises To look at what has happened with equities in the past, we isolated two periods. The first was the period from March 2004 to June 2006, when the Federal Reserve raised rates 4% in 17 measured increments of 0.25%. The second period, though not characterized by the Fed adjusting its fed-funds target, was the "taper tantrum," a period from early May 2013 to early September 2013 when interest rates rose after then-Fed chairman Ben Bernanke indicated that the Fed may slow down the rate of bond purchases, which was part of its quantitative-easing program. During these two periods, we looked at Morningstar sector equity indexes' performance.

Let's first look at the performance of different stock sectors during the taper tantrum period, from May 2, 2013, through Sept. 5, 2013:

This taper-tantrum period was very short (four months), and investors were more focused on bond yields during this time. During this period, stock sectors performed closer to how one might expect them to: The conventional wisdom is that, during rate rises, more defensive sectors that are more bondlike and tend to pay relatively high dividends, have relatively slower growth, and are less exposed to the economic cycle tend to perform the worst, Coffina said. On the other hand, companies that are more economically sensitive--such as technology, basic materials, and energy--tend to do better during periods of rising rates.

Now, let's look at the other period, a two-year period characterized by more measured increases:

Stock sectors didn't perform as one would expect them to during this period. For instance, why were utilities and REITs--two sectors that one might expect would struggle to find their footing during a rate rise--two of the top-performing categories? A lot of the explanation comes down to valuation.

During the period from 2004-06, there were many factors at play, including the health of the overall economy and the outlook for global growth. The economy was fairly robust: GDP rose at a low-single-digit rate in every year; the housing market was strong; the price of oil was volatile but nearly doubled; and corporate profits were relatively robust.

In addition, during the period from 2004-06, utilities and REITs were coming out of a bear market and were a lot cheaper than they would ordinarily be. REITs were especially cheap during the dot-com bubble, and they did a little better during the bear market but were still relatively cheap. Utilities also faced cheap initial conditions going into the period, as they had gotten very cheap after the dot-com bubble burst and were also punished a bit after the Enron scandal, Peters said.

It's Tough to Call the Winners of the Next Rate Rise It would be difficult to predict the winners of the next rising-rate period by either considering rules of conventional wisdom or by extrapolating from past trends. For instance, energy was a standout in the previous rising-rate period; going forward, that may not be the case. Energy stocks are fairly valued today, according to our metrics. And although crude oil prices have held above $65 per barrel for West Texas Intermediate in 2018, we expect growing U.S. production to tip oil markets back into oversupply; our midcycle forecast for WTI is $55/bbl.

And as for REITs, Morningstar believes that underlying performance is healthy overall, as REITs have been focusing on repositioning and strengthening their portfolios, deleveraging, and capital recycling. That's no guarantee of resilience in the face of continued interest-rate increases, though.

"Many investors wonder whether we are near the peak of the commercial real estate cycle--higher interest rates could pressure growth rates, cap rates, return expectations, and ultimately asset prices," notes analyst Kevin Brown. "Also, to the extent that low interest rates have steered investors searching for higher yield and capital preservation toward REITs, the same funds could flow out of REITs if interest rates rise, further pressuring commercial real estate valuations." Clearly, it's challenging to predict how any sector would perform during a rate rise. If rates are going up because the economy is growing, growth stocks will respond faster than value stocks to an acceleration in economic growth--in theory. But in practice, the timing and pace of the rate increase as well as the health of the overall economy and valuation concerns at the sector and stock levels would all be factors, too.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ZM7IGM4RQNFBVBVUJJ55EKHZOU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-22-2024/t_d910b80e854840d1a85bd7c01c1e0aed_name_file_960x540_1600_v4_.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/K36BSDXY2RAXNMH6G5XT7YIXMU.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3a6abec7-a233-42a7-bcb0-b2efd54d751d.jpg)