Financial Services Stocks: Balance Sheet Changes Can Be As Important as Interest Rates

Our top picks in this sector are PayPal, MarketAxess, and US Bancorp.

/s3.amazonaws.com/arc-authors/morningstar/75bbf764-3b6f-4f5a-8675-8f9488c74c04.jpg)

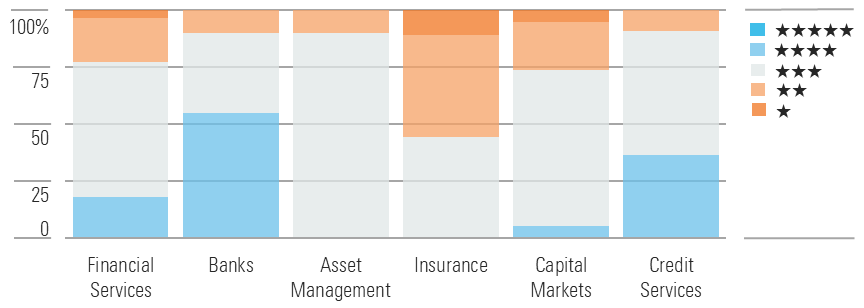

Even after the gains in the stock market this year, we still see pockets of opportunity. We think banks and credit services are relatively undervalued because of uncertainty over when loan charge-offs will peak and because declining interest rates will drag on revenue growth over the next several years.

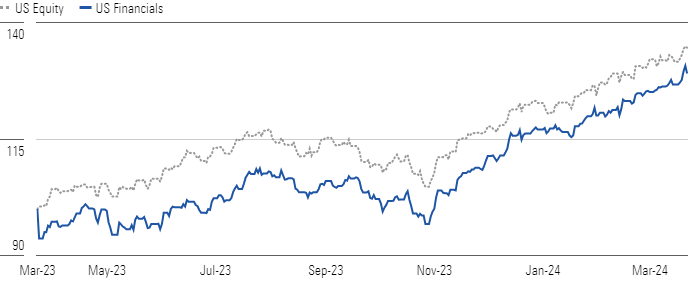

Financial Sector Has Closed Return Gap as Existential Risk Subsides

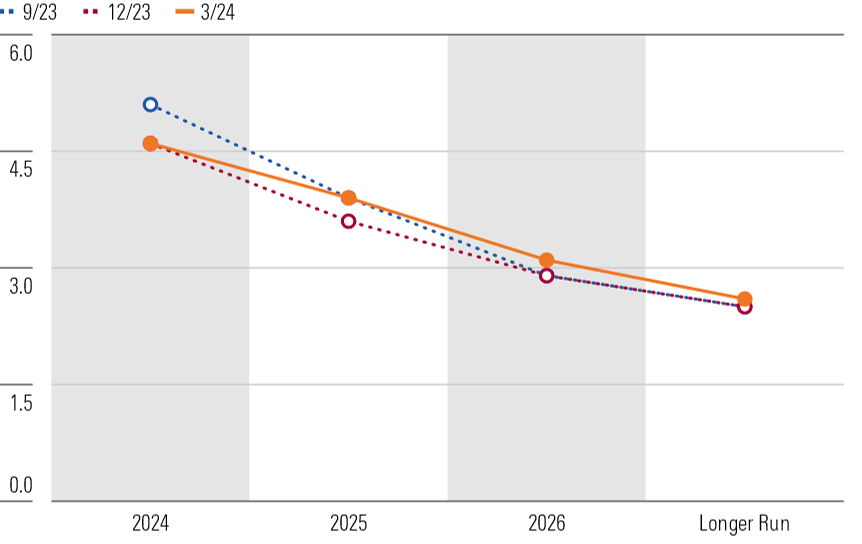

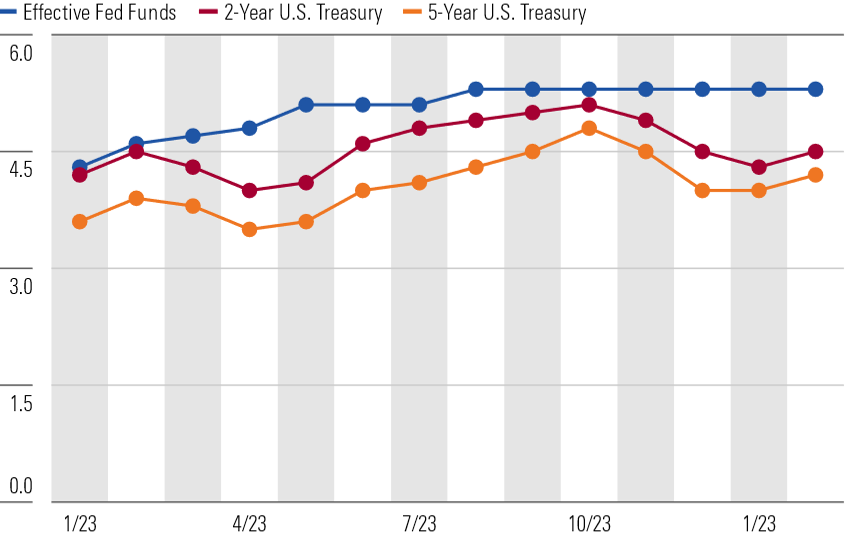

At the March Federal Open Market Committee meeting, participants maintained the target federal-funds rate range at 5.25%-5.50%, and their median projection for the rate at the end of 2024 remained at 4.60%. However, the median rate projections for 2025 and 2026 were higher at 3.9% and 3.1%, respectively, as economic growth has been stronger than expected. Despite the effective rate holding steady for more than two quarters, market expectations for the timing and magnitude of rate cuts have been volatile, as seen in the over-50-basis-point range in the 2-year and 5-year US Treasury rates. Our base case remains that the United States will avoid a recession, inflation will continue to trend downward, and interest rate cuts will come later this year.

We Continue to See the Most Value In Banks and Credit Services

A lower interest rate environment is a headwind for much of the financial sector. Most of these companies are typically asset-sensitive, with the revenue yield on their interest-earning assets repricing more quickly after interest rate changes than the interest rate they pay on their liabilities. This translates to interest revenue falling faster than interest expense when the federal-funds rate and other benchmark interest rates decline.

FOMC Still Projects Three Cuts In 2024 but Fewer Cuts In 2025 and 2026

Over the medium term, we expect balance sheet changes to offset some pressure from lower interest rates. Banks can originate more loans as economic confidence increases. Additionally, fixed-income securities bought when the federal-funds rate was less than 2% are maturing, with the proceeds being invested at a higher coupon rate. We believe investment service firms have much to gain if sweep cash deposits revert closer to their historical levels.

Expectations for the Timing and Magnitude of Rate Cuts Have Been Volatile

Top Financial Sector Picks

MarketAxess Holdings

- Fair Value Estimate: $300.00

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

We expect 2024 to be a better year for growth for MarketAxess MKTX. Last year, the company faced dual headwinds from low corporate bond issuance levels and an unfavorable mix shift creating downward pressure on its average fees. While these factors remain, the company is benefiting from higher trading volume industrywide, and if interest rates fall, MarketAxess will see some relief for its average pricing. That said, the firm continues to face significant competition in the electronically traded US corporate bond market from both Tradeweb TW and the smaller Trumid, and its investment-grade bond market share has been relatively stagnant in recent years. We still see meaningful secular growth drivers, but competition will impede volume growth.

PayPal Holdings

- Fair Value Estimate: $104.00

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Narrow

- Morningstar Uncertainty Rating: High

PayPal’s PYPL shares have fallen about 80% from their pandemic peak to materially below their pre-pandemic price. With market confidence in the stock at a low ebb, we see a potentially good long-term opportunity. While we recognize its near-term headwinds, the company’s long-term fate remains tied to the high-growth e-commerce space, with Venmo providing some additional upside option value. Historically, PayPal has demonstrated it can take shares in this area, and we think it continues to do so overall. We believe the company retains a strong competitive position.

US Bancorp

- Fair Value Estimate: $52.00

- Morningstar Rating: 4 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

The biggest risk to our top banking picks would be surprises on deposit and funding costs or a recession. US Bancorp USB has sold off like some regionals, but we see relatively lower risk since it’s the largest regional. The bank does have slightly higher than average unrealized losses on securities, but we view this more as an earnings problem (lower-yielding assets stuck on the balance sheet) and not a capital one.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-29-2024/t_d0e8253d77de4af9ae68caf7e502e1bf_name_file_960x540_1600_v4_.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/75bbf764-3b6f-4f5a-8675-8f9488c74c04.jpg)