Another Perspective on Stock Prices

Asking once again: Have U.S. equities become cheap?

/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)

A Second Opinion

Last Tuesday’s column reckoned that U.S. stocks appear to be neutrally valued. By my assessment, which combined professor Robert Shiller’s CAPE ratio—a version of stock market price/earnings multiples—with my own addition of 10-year Treasury yields, stocks are neither obviously cheap nor openly expensive.

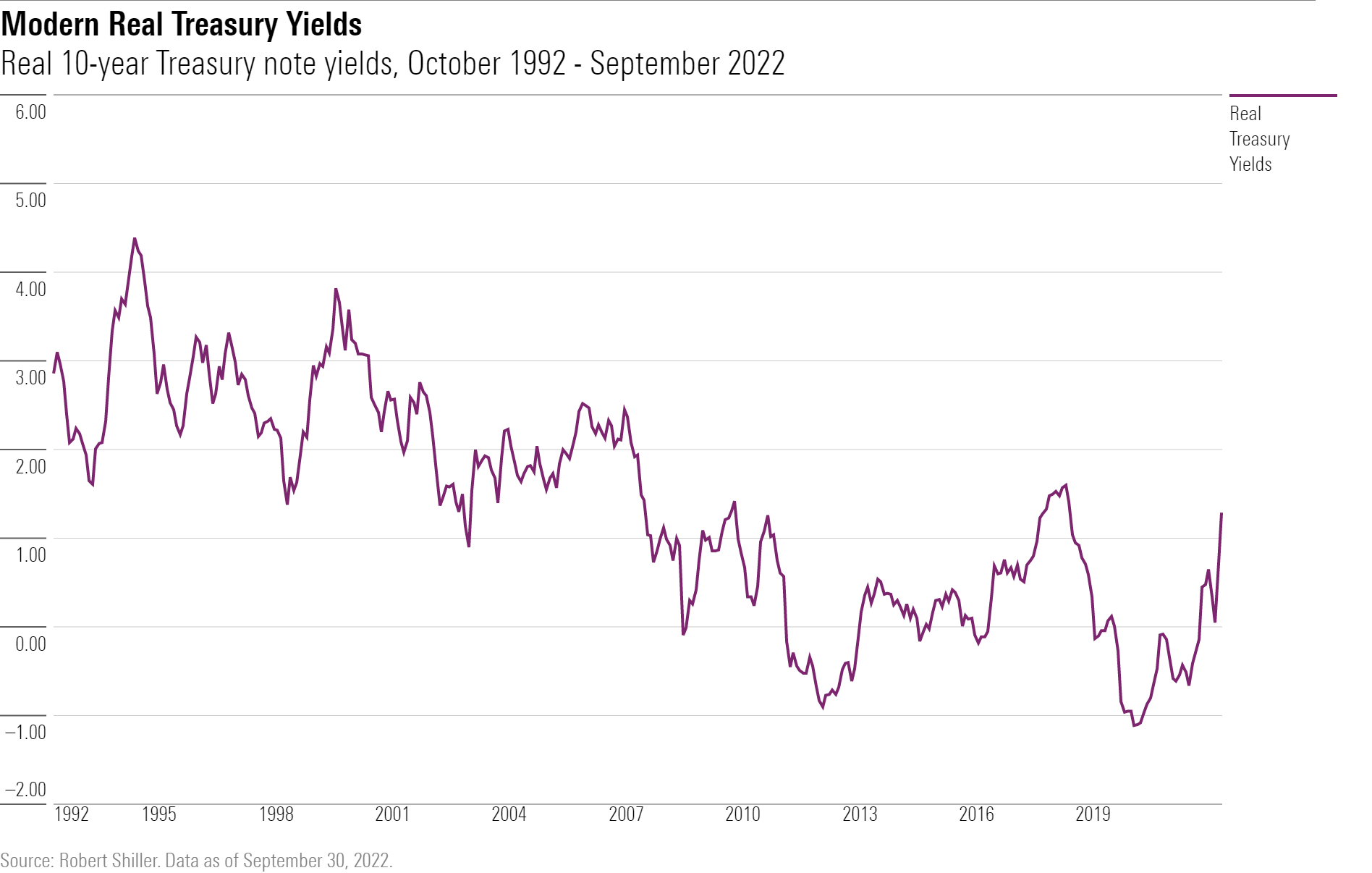

Shortly thereafter, a reader informed me that the professor had anticipated my article, as three years ago he created a statistic called Excess CAPE Yield, or ECY. As with my study, ECY combines the CAPE ratio with 10-year Treasury yields. However, because Shiller does not use prevailing Treasury rates, preferring instead “real” yields, defined as the current yield minus the past decade’s average annualized rate of inflation, his calculation may lead to a different conclusion.

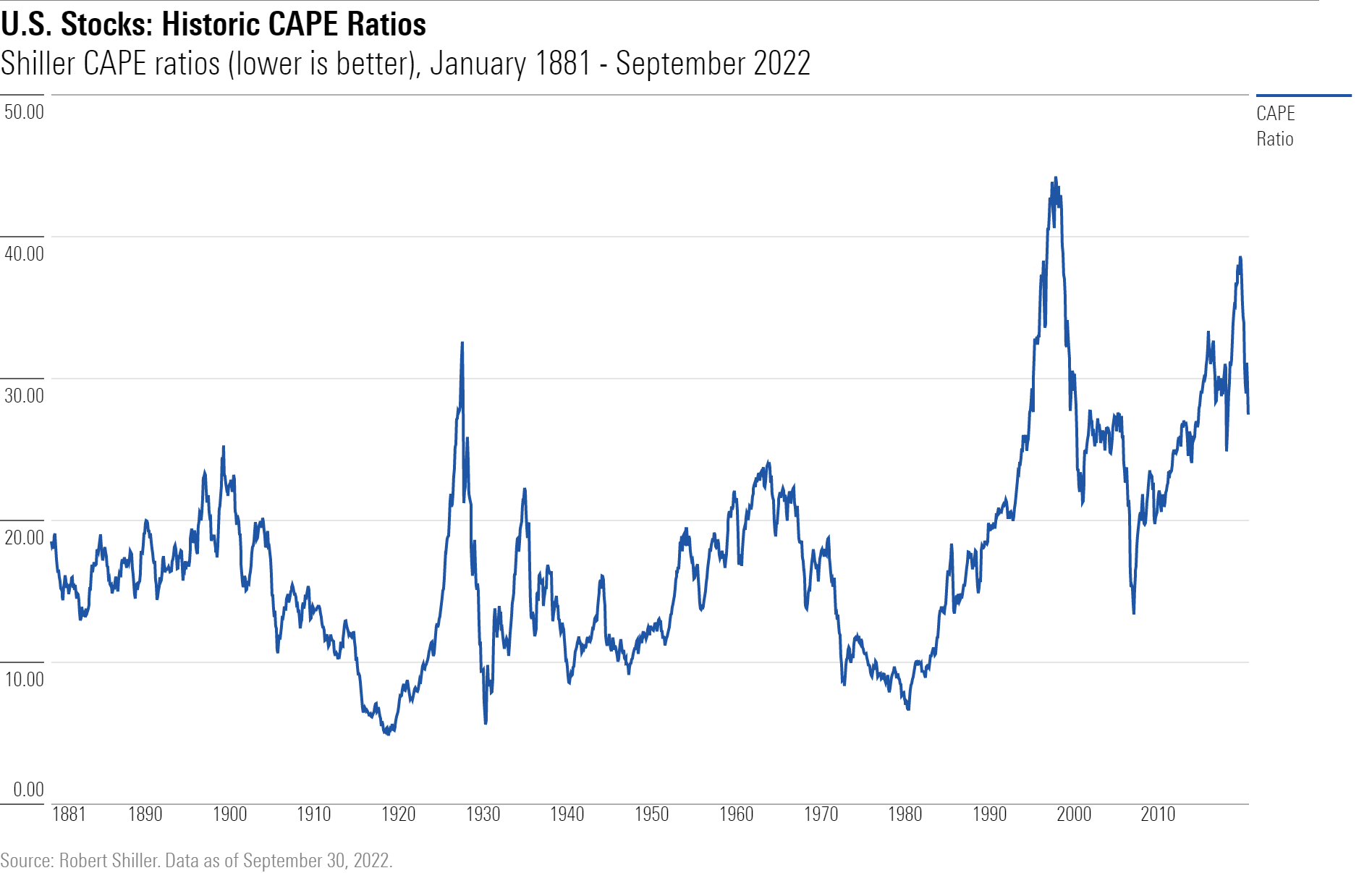

The CAPE Ratio

Let us see. We will start with a repeat of my first exhibit from last week’s article, which shows the long-term results for the CAPE ratio.

By this account, stocks are costly by historic standards but near their typical level over the past three decades. Last week’s article argued that only the recent history was relevant because, over time, investors have re-evaluated stocks, perceiving them as less risky than they did in the distant past. Equity valuations have therefore increased. Although I still believe that claim to be correct, today’s column will provide another justification for a higher CAPE ratio.

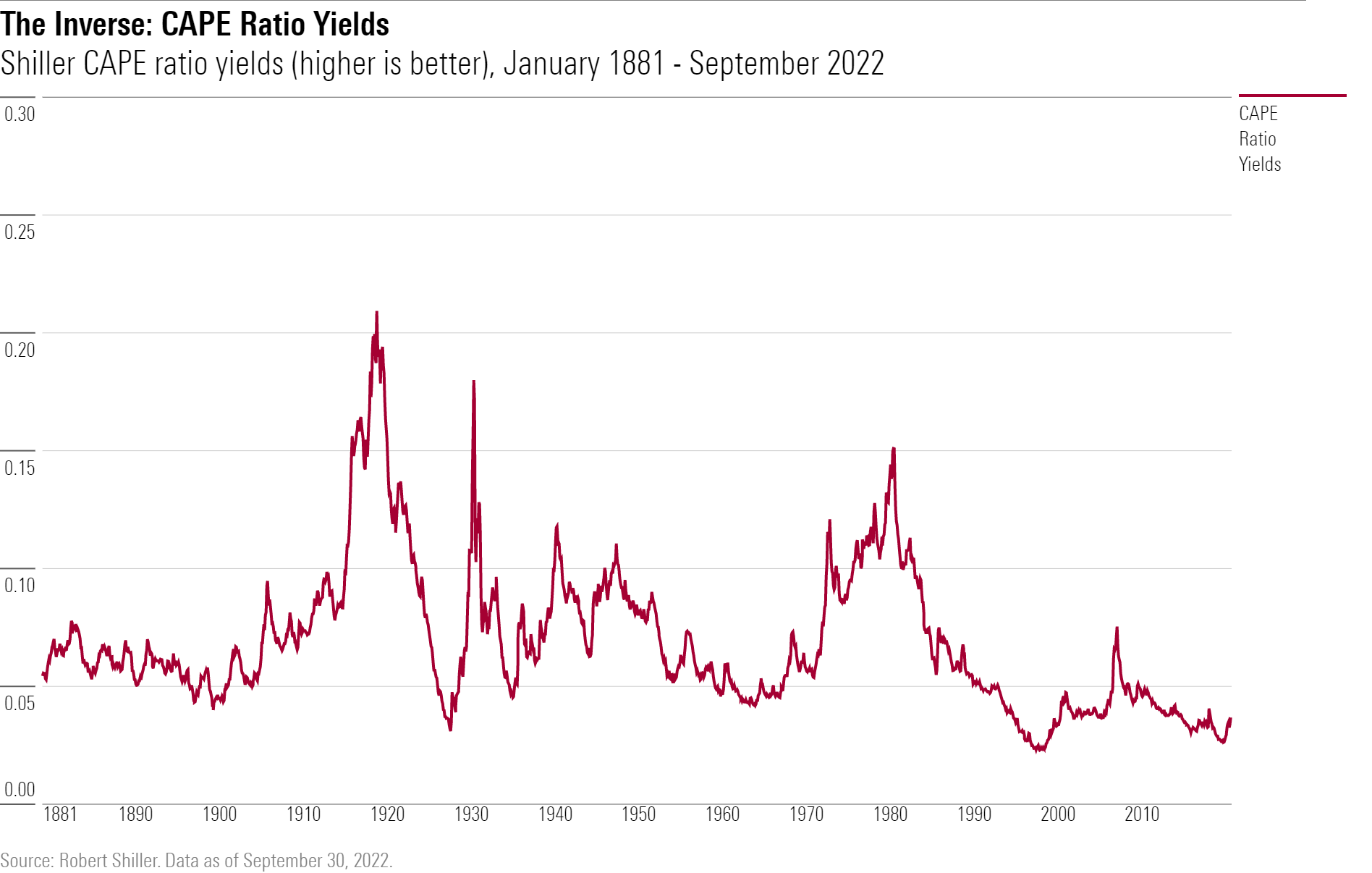

All in due time. For the moment, the next step is to invert the previous chart, by depicting not the CAPE ratio—that is, stock prices divided by earnings—but instead the CAPE ratio yield, which measures earnings divided by stock prices. Doing so places the CAPE ratio on the same footing as ECYs. Both statistics represent yields, meaning that higher results are better and lower ones worse.

At any rate, the following chart tells the same story as its predecessor, except in reverse. Once again, stocks look expensive by the long-term standard but not according to their more recent levels.

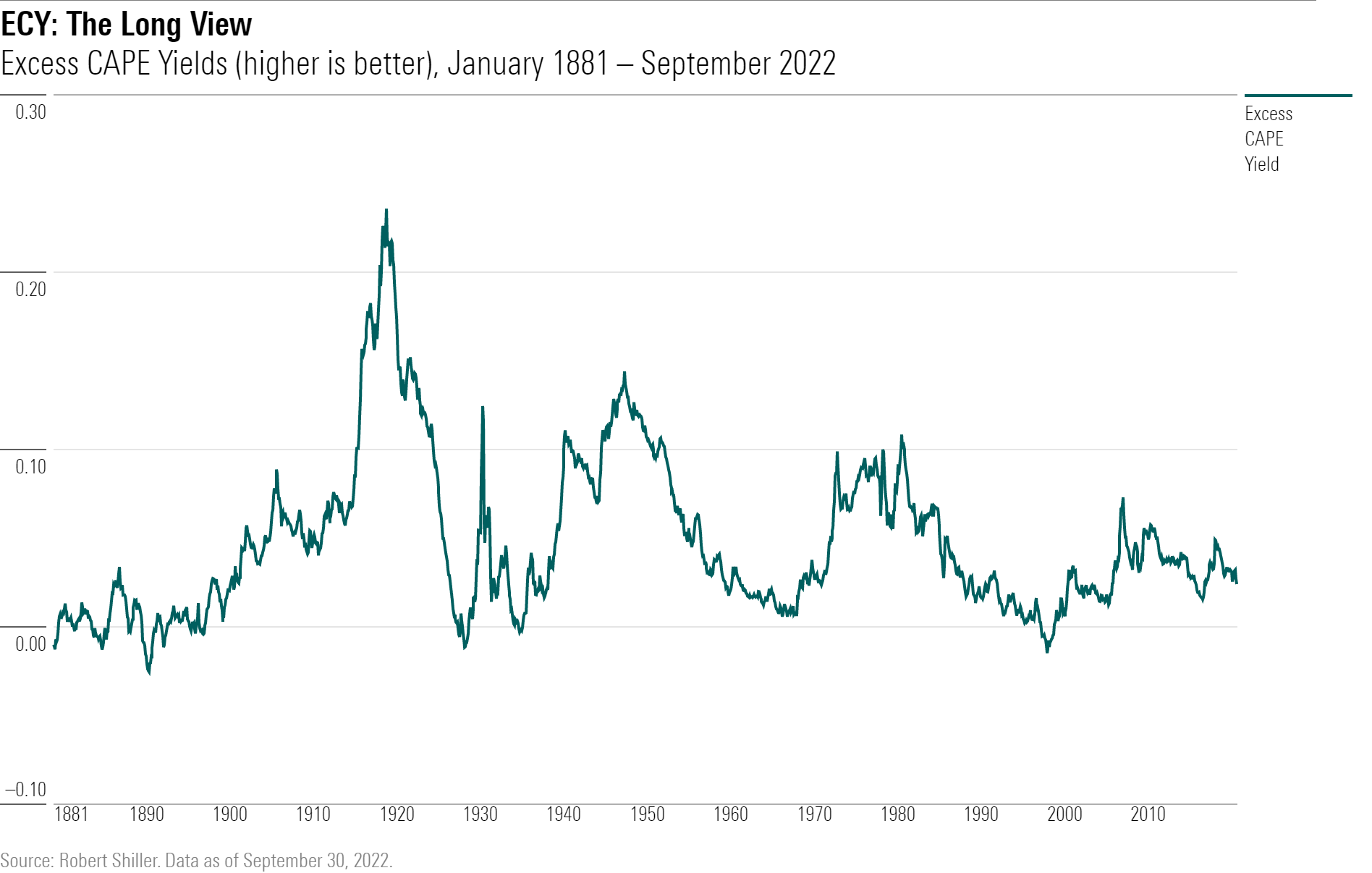

Onto ECYs

Now we can consider Professor Shiller’s ECY statistic. It consists of 1) the CAPE ratio yield shown in the previous exhibit minus 2) the real 10-year Treasury yield. Negative Treasury yields indicate that Treasuries are costly. Consequently, the ECY becomes higher than the CAPE ratio yield. Stocks are more attractive than they otherwise would be because Treasuries are uninviting. In contrast, if the real Treasury yield is strongly positive, then the ECY drops well below the CAPE ratio yield. Stocks become discounted because Treasuries offer fierce competition.

That all sounds a bit complicated, but understanding the ECY line is not; because it merely modifies the CAPE ratio yield, it can be interpreted similarly. High values are good, low values are not. The question thus arises: Does the ECY emulate the CAPE ratio yield in placing below its 150-year average but near its recent norm?

No, it does not.

The pattern is different from before. Whereas the historic CAPE ratio yield consistently exceeded current figures, aside from the Roaring ‘20s, ECYs from the past were often lower. Throughout the late 19th century, for example, the ECY was below today’s levels.

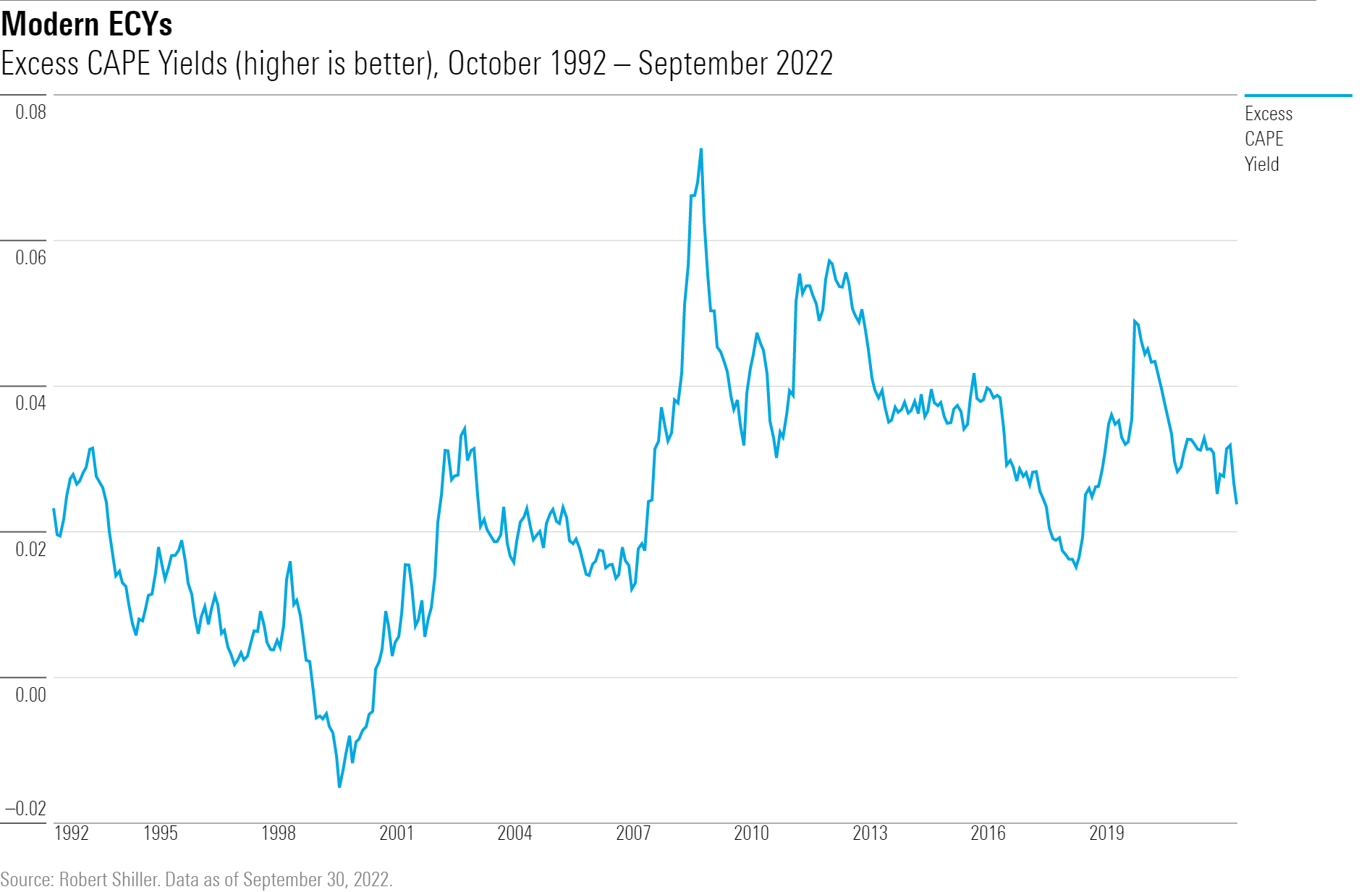

The Past 30 Years

The picture also brightens when evaluating only modern results. As we have seen, the CAPE ratio yield is reasonable by recent standards but not outright low. However, the ECY statistic looks downright alluring, at least as judged by the standards of the ‘90s and early 2000s.

Those were favorable times in which to invest. Admittedly, the new millennium began badly, with a prolonged initial bear market leading several years later to the 2008 financial crisis, but the subsequent rally has fully justified equities. Even after this year’s downturn, Morningstar US Market Index has gained 7.5% annualized over the past quarter century, which equals a cumulative 610%. Such performance is why people own stocks.

Thus, Shiller’s ECY measure produces a happier finding than did my study. As the two approaches appear at first glance to be identical, with each combining CAPE ratios with 10-year Treasury yields, the divergence highlights a peril of investment research. Swapping one seemingly modest detail for another, in this instance nominal Treasury yields for real yields, led to a different verdict.

In Conclusion

One would expect Shiller’s version to be the better guide. For one, Nobel Laureates generally devise better computations than do internet bloggers. For another, using real yields is a theoretically sounder approach than using nominal yields. After all, what matters for investments (Treasury notes or otherwise) is not what they earn before price hikes but rather their after-inflation profits.

However, I am not certain that Shiller’s approach is superior. The problem is that real 10-year Treasury yields have been unstable. As it turns out, the reason that today’s ECY is lower than the totals of the ‘90s and early 2000s is not because of what has occurred with the CAPE ratio but instead because real Treasury yields plummeted after the 2008 financial crisis.

To return to the item mentioned at the start of this column—that decline in real Treasury yields supports a higher CAPE ratio. However, a very large question remains. Does the post-2008 drop in real Treasury yields represent a permanent change, or was it a temporary shift that is now being reversed? We do not know the answer to that query—but it is critical to reading the ECY’s tea leaves.

To summarize what has been a rather complicated argument (full credit to those who have made it this far):

1) Addressing whether stocks are pricey or cheap requires considering the obvious investment alternative: Treasury yields.

2) Unfortunately, making that comparison is tricky. Apparently similar approaches can give different answers.

3) In this case, though, the two verdicts converge. My study suggested that stocks were valued near their normal levels. Professor Shiller’s method initially indicates more optimism, but a closer look reveals that it rests upon the assumption that real 10-year Treasury yields will remain historically low. They may not. And that makes U.S. equities neutrally priced, rather than cheap.

The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/1aafbfcc-e9cb-40cc-afaa-43cada43a932.jpg)