Undervalued by 30%, This Stock Is a Way to Play the Energy Transition

We like this wide-moat chip tester. Here’s why.

/s3.amazonaws.com/arc-authors/morningstar/d53e0e66-732b-4d50-b97a-d324cfa9d1f8.jpg)

Chips will be a major ingredient of the transition to net-zero emissions, helping power the electric vehicles and smart infrastructure that will reduce emissions and curb global warming. Lately, though, chips have been on a roller-coaster ride.

That’s highlighting the charms of some of the semiconductor companies that will play critical roles in the carbon transition. One beneficiary of the march to net zero is Teradyne TER, which makes testing equipment for chipmakers. Among other things, Teradyne equipment tests chips that make cars powered by internal combustion engines more efficient and also help power electric cars, subways, trains, and buses. Meanwhile, Teradyne’s robots inspect and maintain commercial wind turbines and help reduce the risk of human injury in warehouses.

We found Teradyne by sifting through the Morningstar US Sustainability Moat Focus Index. The index currently contains 62 stocks with low-to-medium environmental, social, and governance risk and Morningstar Economic Moat Ratings of wide. The ratings and fair value estimates are determined through independent research conducted by the Morningstar Equity Research team.

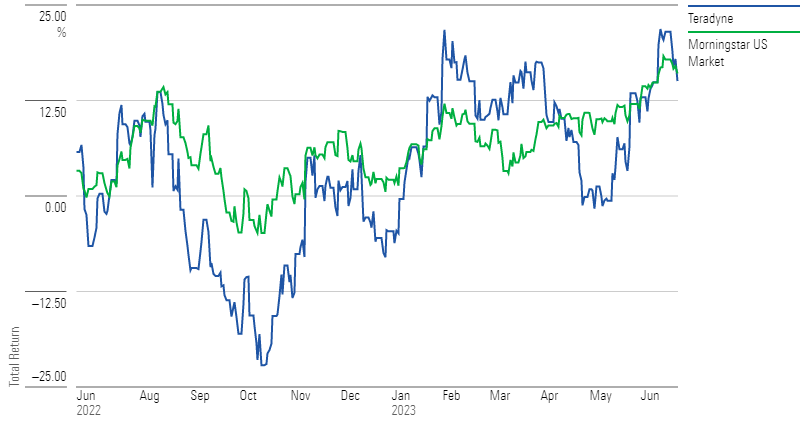

Because the index focuses on companies with moats, it excludes some carbon-transition darlings, such as solar companies. We sorted the companies by cheapness, as expressed by discounts to fair value. So far this year, through June 23, Teradyne is up around 20%, handily beating the Morningstar US Market Index at 13.6%. It also has a low ESG Risk Rating. Yet it trades at 67% of fair value. What gives?

Teradyne Stock Is Reviving

Why Is Teradyne Stock at a Discount?

Industry: Semiconductor Equipment & Materials

Stock Price: $105

Fair Value Estimate: $157

In April, Teradyne’s first-quarter report showed that declines for its wireless and system test businesses “now appear steeper than we had previously forecast,” wrote Morningstar analyst William Kerwin. First-quarter sales declined 18% from a year earlier, with declines in every end market, including systems test, wireless test, and robotics segments amid a downturn in the hard-disk-drive market and weakness in mobile devices and global industrial demand. Nevertheless, demand remained strong in the automotive and industrial chip markets.

What Is Teradyne, and Why Does It Have a Moat?

Teradyne is one of two companies worldwide that can produce testers for the most cutting-edge semiconductors. (The other is Advantest ATEYY).

It provides testing solutions for nearly every semiconductor under the sun. “Teradyne’s ability to design testing equipment for bleeding-edge chips is the biggest driver of its competitive advantage, representing intangible assets that we don’t think are easily replicable,” writes Kerwin.

That makes it a vital supplier to chipmakers. In particular, it has extremely strong relationships with Apple AAPL and Taiwan Semiconductor TSM. “It dominates its industry,” says Kerwin in an interview. “It’s unique on the back end.” Teradyne also sells what are called “collaborative robots” and self-driving vehicles for factories and warehouses.

That dominance has produced robust returns. “Teradyne’s market leadership exhibits itself in industry-leading margins, strong returns on invested capital, and a top market share,” writes Kerwin. More pluses: Teradyne’s ability to generate free cash flow in a capital-intensive business, and its use of extra cash to bolster its market position in robots and other businesses. It had $859 million in cash on March 31. As of the first quarter, semi test accounted for 67% of revenue, robotics for 14.4%, system test for 12.1%, and wireless test for 6.3%.

Teradyne’s Sustainability

Teradyne’s ESG risk is low, according to Morningstar Sustainalytics. Human capital is its biggest material risk. Mirela Lupu, ESG research team lead, technology, media and telecommunications for Morningstar Sustainalytics, ticks off Teradyne’s charms. Lupu notes that management has anticipated and addressed potential ESG problems and is also “disclosing a lot” on ESG measures.

Teradyne’s financial strength also gives management ammunition to address any additional ESG risks that may arise. “Because the company has strong financial performance, it’s more prepared to mitigate risk,” says Lupa. Indeed, Sustainalytics dubs Teradyne in the top-rated companies in its industry in terms of ESG risk.

By 2025, Teradyne aims to achieve 100% renewable energy to cover U.S. scope 2 emissions; it’s setting up a road map to use 100% renewables to reach this goal. For example, it’s targeting 100% renewables for the Philippines this year, which accounts for a large chunk of Teradyne’s emissions. It reports emissions and other data to the Carbon Disclosure Project annually. Those emissions goals hold even as it acquires new companies.

Teradyne has other solutions for global warming. Its robots maintain wind turbines, for example. The company believes its robots help reduce waste in manufacturing processes and are more flexible than traditional industrial robots. That helps companies move from “mass production to tailor-made and high-mix, low-volume production, which gives businesses the ability to adapt to consumer needs while avoiding waste and overproduction,” says Teradyne.

What’s Next for Teradyne?

Over the long haul, Teradyne’s prospects look bright. Speaking at a JPMorgan conference in May, Rick Burns, Teradyne’s president of semiconductor test, said three key technologies are driving automotive demand: autonomous driving, high voltage technology, and battery management.

More chips and increasingly complicated uses and packaging mean more testing. Teradyne is a “beneficiary of a tectonic shift to a computing era, with tens of billions of Internet of Things devices shipping annually,” wrote Jefferies analysts led by Vedvati Shrotre in an April 27 note. For such products as robotics, “these applications have zero-defect requirements.”

Kerwin says he expects Teradyne’s results to bottom out this year, and to see “an immense rebound in 2024″ as chip test demand revives. The company has said it expects earnings per share of $7.50 to $10 in fiscal 2026. That suggests double-digit compound annual growth, Kerwin says. “Investors will require patience for 2023, but we reaffirm our belief that shares of this testing behemoth are seriously undervalued.”

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/d53e0e66-732b-4d50-b97a-d324cfa9d1f8.jpg)