After Earnings, Is MongoDB Stock a Buy, Sell, or Fairly Valued?

With a solid quarter that exceeded our expectations, here’s what we think of MDB earnings and stock.

/s3.amazonaws.com/arc-authors/morningstar/f497c984-8e67-4c32-8c6c-210934e57017.jpg)

MongoDB MDB released its second-quarter earnings report on Aug. 31 after the close of trading. Here’s Morningstar’s take on what to think of MongoDB’s earnings and stock.

Key Morningstar Metrics for MDB

- Fair Value Estimate: $379

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: None

- Morningstar Uncertainty Rating: High

What We Thought of MongoDB’s Q2 Earnings

- Earnings Beat: MongoDB had a solid quarter, exceeding our expectations all around. We were pleased to see that consumption on the cloud Atlas platform was rosier than expected, as we think the firm is wisely focusing on customer acquisition over upfront billing.

- High Retention Rates: The latest results helped support our current thesis. Retention rates remain high, which indicates MongoDB continues to show all the right signs of benefiting from switching costs, even in this current macroeconomic environment.

MongoDB Stock Price

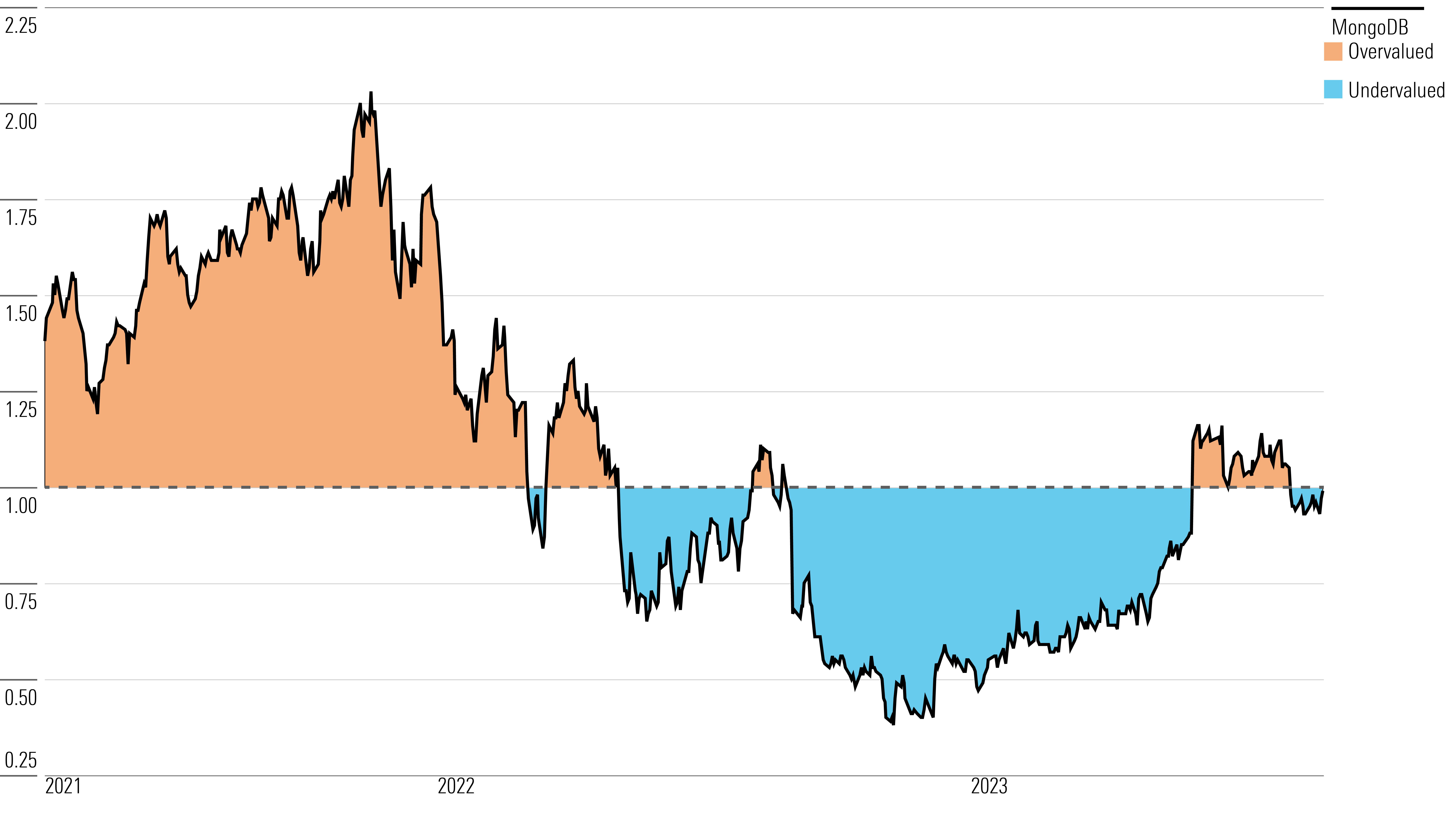

Fair Value Estimate for MongoDB

With its 3-star rating, we believe MongoDB’s stock is fairly valued compared with our long-term fair value estimate.

Our fair value estimate for MongoDB is $379 per share. Our valuation implies forward fiscal-year enterprise value/sales of 17 times and a free cash flow yield of 0%. Our fair value estimate assumptions are based on our expectations for MongoDB achieving a compound annual growth rate over the next five years of 23%. MongoDB is in its infancy but has a massive market opportunity and a large runway for growth ahead of itself, in our view. We expect this substantial growth to be driven by continued shifts of workloads to a cloud environment, prompting the database market to grow robustly, especially NoSQL databases like document-based databases, as companies realize how much easier it is to scale data storage in the clouds. In turn, this implies substantial usage growth per customer for MongoDB. Additionally, we think MongoDB’s database-as-a-service offering, Atlas, and data lake will bring significant new revenue streams to the company—as Atlas revenue eclipsed on-premises sales in early fiscal 2022.

We forecast that MongoDB’s gross margins will stay relatively the same, as the company’s increasing mix of Atlas revenue is somewhat margin-dilutive in the near term. We expect GAAP operating margins to increase from negative 27% in fiscal 2023 to positive 27% in fiscal 2033, as a result of operating leverage as revenue growth exceeds operating expenses.

Read more about MongoDB’s fair value estimate.

MongoDB Price/Fair Value

Economic Moat Rating

We assign MongoDB a no-moat rating. We think the company benefits from significant switching costs with the customers that it has captured thus far. However, the company is still in its customer acquisition phase, and it is unclear that this moat source will lead to excess returns on invested capital over the next 10 years as MongoDB lacks profitability and continues to aggressively spend on sales and marketing.

MongoDB is a NoSQL database. This means that, instead of storing data in tables, like a relational, SQL database, MongoDB stores data in a different format. There are many nonrelational ways to store data, but MongoDB does so by storing data in collections that are known as documents. Document-based formats provide some appealing characteristics, which include the ability to store both structured and unstructured data and its ease of scalability.

While MongoDB is widely considered to be the best document-based database, many competitors exist, like Couchbase and AWS Document DB. The presence of these competitors (and particularly Amazon, which has nearly unlimited resources) restricts us from assigning MongoDB with an additional moat source based on intangible assets.

MongoDB has not yet reached enough size and scale to generate excess returns on capital, even when considering a good portion of its sales and marketing costs as an asset with future benefits, rather than a wasteful expense.

We think it will take a few more years for MongoDB to reach such excess returns, as the company will likely continue to generate operating losses as it continues to invest in customer acquisition. These subpar returns preclude us from assigning MongoDB with a narrow moat rating, but we’ll continue to monitor MongoDB’s ability to attract new business and profit from a potentially sticky customer base in the years ahead.

Read more about MongoDB’s moat rating.

Risk and Uncertainty

We assign MongoDB a High Morningstar Uncertainty Rating because of its place in a technological landscape that has the potential to shift rapidly. However, we do not foresee any material environmental, social, or governance issues on the horizon.

MongoDB faces uncertainty based on future competition. MongoDB runs the risk of Amazon encroaching on its abilities. Currently, Amazon’s DocumentDB service claims it has MongoDB compatibility, so that it can help companies deploy MongoDB at scale in the cloud, similar to MongoDB Atlas. At the moment, DocumentDB has significant limitations compared with MongoDB—with the inability to support rich data types, interoperability with AWS only, and only 63% compatibility with MongoDB—all in contrast to MongoDB Atlas. While many open-source software companies have suffered from Amazon reselling their software on their own platform for a profit (for example, Elastic was repackaged into Amazon Elasticsearch), MongoDB is protected against this risk, as its software license bans Amazon from reselling its software on AWS.

On the ESG front, MongoDB is at risk of compromising the data stored in its database through data breaches. For example, MongoDB offers a number of security features for protecting data, like authentication, access control, and encryption. However, if any of these features were to fail, MongoDB’s brand could suffer significantly and possibly lead to diminished future business.

Read more about MongoDB’s risk and uncertainty.

MDB Bulls Say

- MDB’s document-based database is best equipped to remove fear of vendor lock-in and is poised for a strong future.

- MongoDB’s new data lake could gain significant traction, making MongoDB even stickier, as we believe data lakes have even greater switching costs than databases. In turn, this could further boost returns on invested capital.

- MongoDB could eventually launch its own data warehouse offering, which would further increase customer switching costs.

MDB Bears Say

- Document-based databases could decrease in popularity, as a new NoSQL variation arises, better meeting developers’ needs.

- Cloud service providers, like AWS, could catch up to MongoDB in terms of its rich features.

- MongoDB’s profitability could see only gradual improvements, as the need or relevance in a fast-changing tech landscape could diminish major operating leverage.

This article was compiled by Saaketh Tirumala.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KD4XZLC72BDERAS3VXD6QM5MUY.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/f497c984-8e67-4c32-8c6c-210934e57017.jpg)