After Earnings, Is Home Depot Stock a Buy, a Sell, or Fairly Valued?

As the company gains traction with professional builders, here’s what we think of Home Depot’s stock.

/s3.amazonaws.com/arc-authors/morningstar/3559e02b-f74d-4a72-a821-b50f61ba05e9.jpg)

Home Depot HD released its third-quarter earnings report on Nov. 14, before trading hours. Here’s Morningstar’s take on Home Depot’s earnings and stock.

Key Morningstar Metrics for Home Depot

- Fair Value Estimate: $263.00

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: Medium

What We Thought of Home Depot’s Q3 Earnings

Home Depot’s third-quarter earnings came in near our forecasts.

Specifically, $37.7 billion in net sales closely matched our $37.8 billion estimate. The firm’s diluted earnings per share of $3.81 eclipsed our $3.72 preprint estimate, leading to 20 basis points of operating margin upside from our forecast.

Results were helped by Home Depot’s strategic pricing tactics and its ability to blunt sales deleverage through enhanced productivity and agile execution (factors that underpin our wide moat rating). The firm’s updated full-year guidance now calls for a 3%-4% drop in net sales (from 2%-5%) and a 9%-11% decline in diluted EPS (previously 7%-13%), largely in line with our respective -3% and -8% preprint estimates.

Unpacking the top-line performance, comparable sales fell 3.1%, driven by a 2.7% downdraft in transactions and flat average ticket growth. Still, strength persisted in the pro segment, and we continue to believe it will serve as the firm’s core growth vector.

In this context, we believe Home Depot’s efforts to better cater to complex pros through expanding its outside sales team, building out capabilities, and enhancing service while leveraging its robust scale and distribution network should drive meaningful share gains in this underpenetrated market, providing confidence in our forecasts of 4% sales growth over the next decade and nearly 16% long-term operating margins.

Home Depot Stock Price

Fair Value Estimate for Home Depot

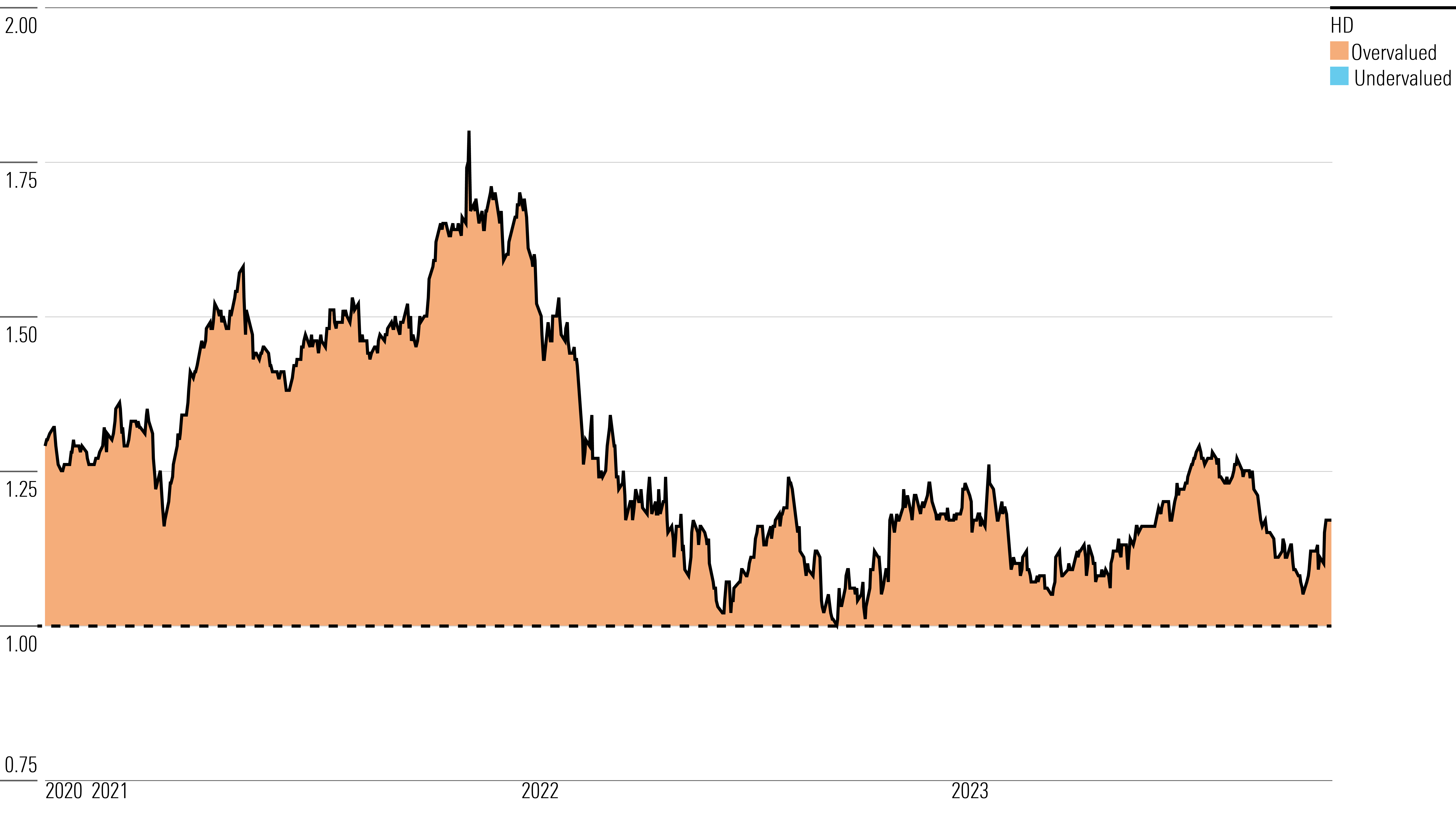

With its 2-star rating, we believe Home Depot’s stock is overvalued compared with our long-term fair value estimate of $263.

Given the maturity of the domestic home improvement industry, we expect demand to largely depend on changes in the real estate market, driven by prices, interest rates, turnover, and lending standards. We project 2.4% average sales growth over the next five years, supported by 2.0% average same-store sales increases and helped by offerings like buy online/pick up in store, as well as better merchandising, which drives market share gains.

Looking at the longer term, we forecast gross margins to expand modestly over the next decade (by 10 basis points from 2022 levels to 33.6%) while the SG&A expense ratio remains flattish (around 17%) as the firm capitalizes on its scale and supply chain improvement initiatives while investing to protect its market leadership. This leads to a terminal operating margin of 15.5%, higher than the 15.3% peak in 2022.

Read more about Home Depot’s fair value estimate.

Home Depot Historical Price/Fair Value Ratio

Economic Moat Rating

We assign Home Depot a wide economic moat, arising from its brand intangible asset and cost advantage.

We think the company’s impressive same-store sales growth, which has averaged 7% over the past 10 years, suggests it has a brand intangible asset. For one, we think its extensive product offerings and services have fostered loyalty. Home Depot moves 30,000-40,000 stock-keeping units in store and 1 million units online, allowing consumers to save time and effort by visiting one shop for all a project’s needs. To continue to engage consumers and keep up with changing demand (like for localization and personalization), the firm leverages consumer data, collaborates with suppliers, and conducts periodic merchandising resets to better refine its assortments.

Home Depot’s ability to negotiate with vendors lets it provide value and instill customer loyalty by passing along a portion of these savings in the form of everyday low pricing, or EDLP. This is a result of negotiating clout due to scale, as savings from bulk purchases facilitate this pricing mechanism. We think EDLP drives a positive flywheel effect, prompting customers to return since they understand the company’s value proposition, driving further scale gains in turn. As evidence, total transactions at Home Depot were 1.7 billion in 2022, up 20% from 1.4 billion in 2013. There’s also the stability of gross margins, which have generally clocked in the 33%-34% range over the past decade—which we believe will persist, as any scale benefits will likely be passed directly on to consumers.

Read more about Home Depot’s moat rating.

Risk and Uncertainty

We give Home Depot a Medium Uncertainty Rating owing to its strong brand recognition, which has helped stabilize sales through the cycle.

Home Depot’s sales are largely driven by greater consumer willingness to spend on category goods, with stable existing-home price growth and decent turnover. Thanks to the maintenance, repair, and operations business (Interline Brands and HD Supply), pro revenue could be less cyclical, as the maintenance side of the business can prove more consistent.

In uncertain economic times, consumers remain in their homes, embarking on improvement projects and boosting do-it-yourself revenue. Alternatively, when home prices rise, the wealth effect generates a psychological boost to consumers, reinvigorating professional sales thanks to a higher willingness to spend on big projects. A diverse consumer base helps normalize revenue even in uneven times. Currently, about half of sales are in the do-it-yourself arena, while the rest are generated by pro customers.

Although new competitors could set up shop on Home Depot’s turf, we think they would be hard-pressed to offer similar prices, as they likely wouldn’t have vendor relationships of the same magnitude. Ultimately, the biggest brands in home retailing will still want the biggest partners for distribution, leaving a new peer in a precarious position when seeking enough of the most sought-after products to satisfy demand.

We believe Home Depot’s biggest risk is a slowdown in the real estate market, signaled by increased home inventories for sale, slower price growth, or higher mortgage rates (up about 170 basis points in the last 12 months).

Read more about Home Depot’s risk and uncertainty.

HD Bulls Say

- Home Depot’s continued investments in supply chain and merchandising should improve productivity and support its market leadership position.

- The company has returned $70 billion to shareholders through dividends and share buybacks over the past five years, above 20% of its market cap. In our outlook, we forecast Home Depot to return nearly $80 billion to shareholders over the next five years.

- The maintenance, repair, and operations market is around $100 billion, and Interline and HD Supply make up a low-double-digit share, leaving meaningful upside up for grabs.

HD Bears Say

- Weak consumer spending, higher interest rates, or an economic downturn could hinder sales for home improvement projects and affect Home Depot’s growth.

- IT and supply chain improvement gains could prove more challenging to achieve, as simpler efforts have already borne fruit. Further productivity efforts could face some implementation risks, creating inconsistent profitability.

- As home improvement demand normalizes, consumers could continue to shift discretionary spending into other discretionary categories, like leisure and restaurants.

This article was compiled by Brendan Donahue.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/ECVXZPYGAJEWHOXQMUK6RKDJOM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/KOTZFI3SBBGOVJJVPI7NWAPW4E.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/3559e02b-f74d-4a72-a821-b50f61ba05e9.jpg)