After Earnings, Is Adobe Stock a Buy, a Sell, or Fairly Valued?

With good results and strong revenue growth, here’s what we think of Adobe stock.

Adobe ADBE released its fourth-quarter earnings report on Dec. 13, after the close of trading. Here’s Morningstar’s take on Adobe’s earnings and stock.

Key Morningstar Metrics for Adobe

- Fair Value Estimate: $610.00

- Morningstar Rating: 3 stars

- Morningstar Economic Moat Rating: Wide

- Morningstar Uncertainty Rating: High

What We Thought of Adobe’s Earnings

- Overall, results were good, coming in ahead of consensus estimates. Net new annual recurring revenue was a bright spot. Adobe’s AI image-generation tool Firefly is drawing huge interest and increasing the number of potential new users.

- Management is confident that good trends from the fourth quarter will continue into the first quarter of 2024. The impact of 2023 price increases was not communicated well; management could have explained more about how this will affect revenue for 2024 and 2025. But overall, the street was too aggressive on the impact of the price increases.

- Adobe is a great company with a wide moat. It called off its acquisition of Figma on Monday, which does not change much for our long-term view, though it creates a chink in the firm’s armor. Adobe will have to switch from a “buy” mentality to a “build” one to bring the Creative Cloud apps to the web and allow multiple users to edit simultaneously.

- Adobe stock is currently fairly valued. The company has a great management team, and we expect revenue to grow nicely over time with modest margin expansion.

- We see better opportunities in Microsoft MSFT, Salesforce CRM, and ServiceNow NOW in the large-cap space, but they are all good holdings.

Adobe Stock Price

Fair Value Estimate for Adobe

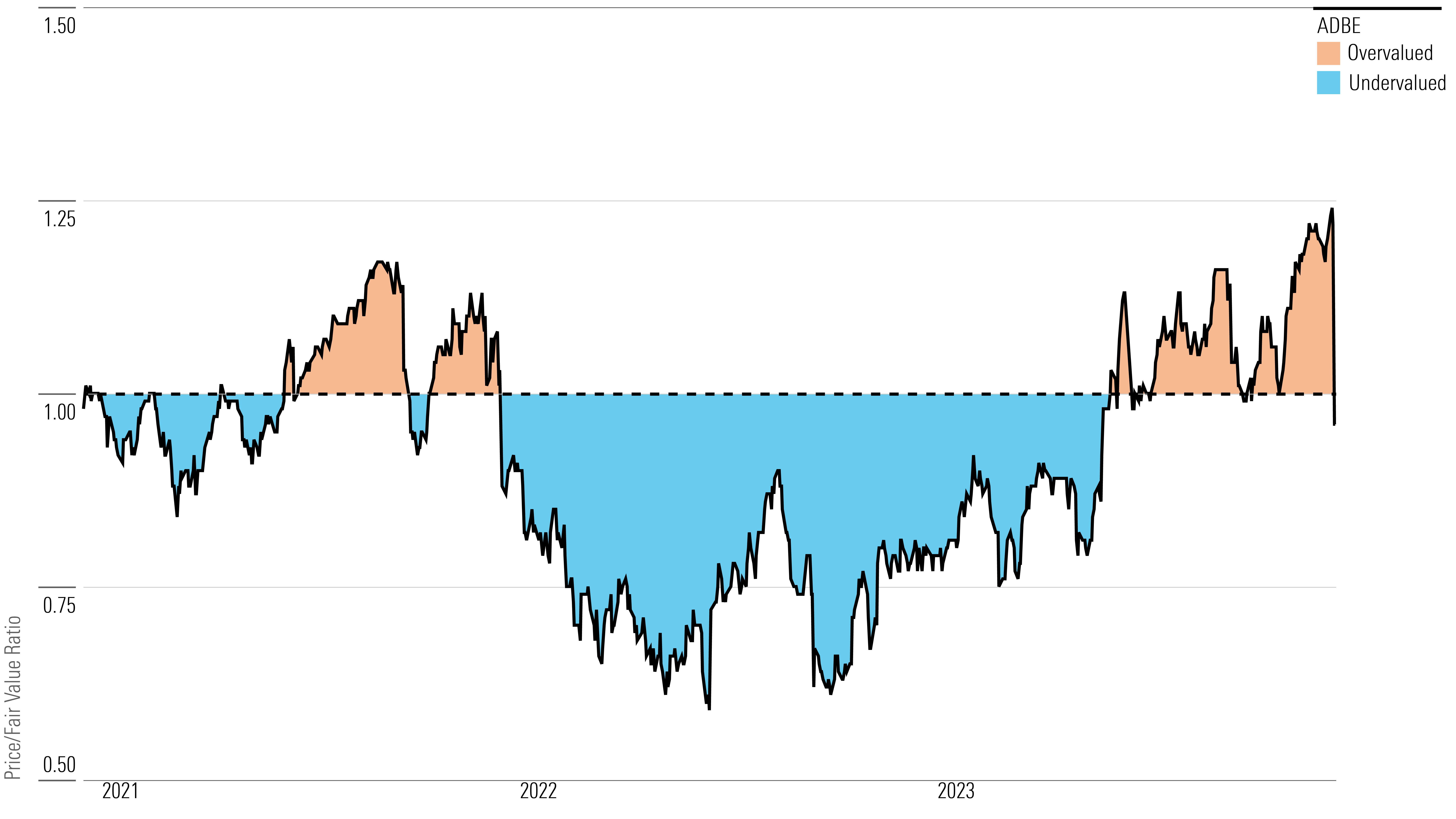

With its 3-star rating, we believe Adobe’s stock is fairly valued compared with our long-term fair value estimate. We have raised our fair value estimate to $610 from $510 per share.

We model a five-year revenue compound annual growth rate of approximately 12%. We foresee solid growth in both digital media and Digital Experience, even as both steadily slow over time. Digital Experience should benefit both from 2023 price increases, which should filter in over several years, and increasing penetration into an enormous market.

We believe Adobe has a relatively frictionless cross-selling opportunity, as creative professionals are already steeped in its products. The desire to consolidate vendors makes the firm an obvious choice for marketing software solutions, and the fact that Adobe’s products are strong should help initially in what we believe is a large greenfield opportunity.

Within digital media, we have been impressed by Adobe’s ability to draw in new users that many did not believe existed. We believe some of this is related to piracy, which is effectively eliminated by the software-as-a-service model.

The company has also had success upselling existing users to higher-priced products and cross-selling acquired technologies, such as Workfront and Frame.io. We believe continued innovation, gathering new users, and upselling existing users in Creative Cloud should help drive strong growth for the next several years.

Read more about Adobe’s fair value estimate.

Adobe Historical Price/Fair Value Ratio

Economic Moat Rating

We assign Adobe overall a wide moat, arising from switching costs and network effects. Looking at the company’s segments, we believe digital media has a wide moat thanks to switching costs and network effects, digital experience has a narrow moat arising from switching costs, and publishing has a narrow moat from switching costs.

Since its introduction in 1989, Photoshop has become the industry standard for image editing software. Rather than remaining complacent, Adobe has consistently invested in the solution, introducing new features and adding applications that could be sold to existing users.

High switching costs are the primary driver of Creative Cloud’s wide moat. While there are many competitive products, it’s so pervasive that replacing it would be an insurmountable barrier, in our view. While Creative Cloud has its issues (particularly premium pricing) and any one organization or freelance professional might be willing to switch, they would find it difficult to work within an industry that has standardized around these tools. Similarly, this helps ensure that when Adobe releases or acquires a related solution, it too becomes widely adopted.

Read more about Adobe’s moat rating.

Risk and Uncertainty

We assign Adobe a High Morningstar Uncertainty Rating. It faces risks that vary by segment.

Creative Cloud’s high market share over the last 25 years means a significant portion of high-margin revenue is at risk (however slight) if a competitor were to make inroads in the space. The dampening of cross-selling opportunities with Digital Experience would likely then be diminished, which would be problematic, as in our view it represents the larger growth opportunity over the next five years. While Adobe is generally considered a leader in the various categories included under its Digital Experience umbrella, it did not create any of these categories, and it does not dominate them the way it does with Creative Cloud.

Adobe has built Digital Experience largely through acquisitions. The recent acquisitions of Magento and Marketo pose risks, as they were on the larger side. Any integration missteps could potentially cause delays in new contract signings.

Furthermore, material missteps could result in substantial write-downs regarding these (or other) acquisitions. While the margin structure may ultimately be lower in Digital Experience relative to Creative Cloud, the company has worked to improve margins over time, and we believe Adobe must continue to drive down costs and expand margins to meet investor expectations.

Read more about Adobe’s risk and uncertainty.

ADBE Bulls Say

- Adobe is the de facto standard in content creation software and PDF file editing—categories the company created and still dominates.

- The shift to subscriptions eliminates piracy and makes revenue recurring while removing high up-front prices for customers. Growth has accelerated and margins are expanding from the initial conversion inflection.

- Adobe is extending its empire in the creative world from content creation to marketing services more broadly through the expansion of its Digital Experience segment, which should drive growth in the coming years.

ADBE Bears Say

- Momentum is slowing in Creative Cloud after elevated growth driven largely by the transition to the SaaS model.

- There is greater uncertainty in Digital Experience, given that this is an emerging space that Adobe neither created nor dominates. Growth could be slower than we anticipate, or margin expansion may not materialize.

- Digital Experience has been built largely through acquisitions, including Magento and Marketo in 2018. This raises the possibility of disruption from inadequate integration efforts and lends credence to concerns that Adobe may overpay for increasingly large deals.

This article was compiled by Bella Albrecht.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TP6GAISC4JE65KVOI3YEE34HGU.jpg)

/d10o6nnig0wrdw.cloudfront.net/04-29-2024/t_d0e8253d77de4af9ae68caf7e502e1bf_name_file_960x540_1600_v4_.jpg)