33 Undervalued Stocks for 2020

Here are our analysts’ top ideas in each sector for the new year.

/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)

For the new list of Morningstar’s top analyst picks, read our latest edition of 33 Undervalued Stocks.

U.S. stocks finished 2019 with a remarkable 31% return, as measured by the S&P 500. Not surprisingly, we think stocks are about fairly valued bui: The median stock in our North American coverage universe traded at a 3% premium to our fair value estimate at year’s end.

The share of 1- or 2-star stocks has surpassed those earning 4- and 5-star ratings: 32% versus 21%, observes Jeffrey Stafford, Morningstar's director of North American equity research, in his latest stock market outlook. The energy, consumer cyclical, and communication-services sectors look the least expensive.

Here are some specific undervalued stocks across sectors that are among our analysts' best ideas.

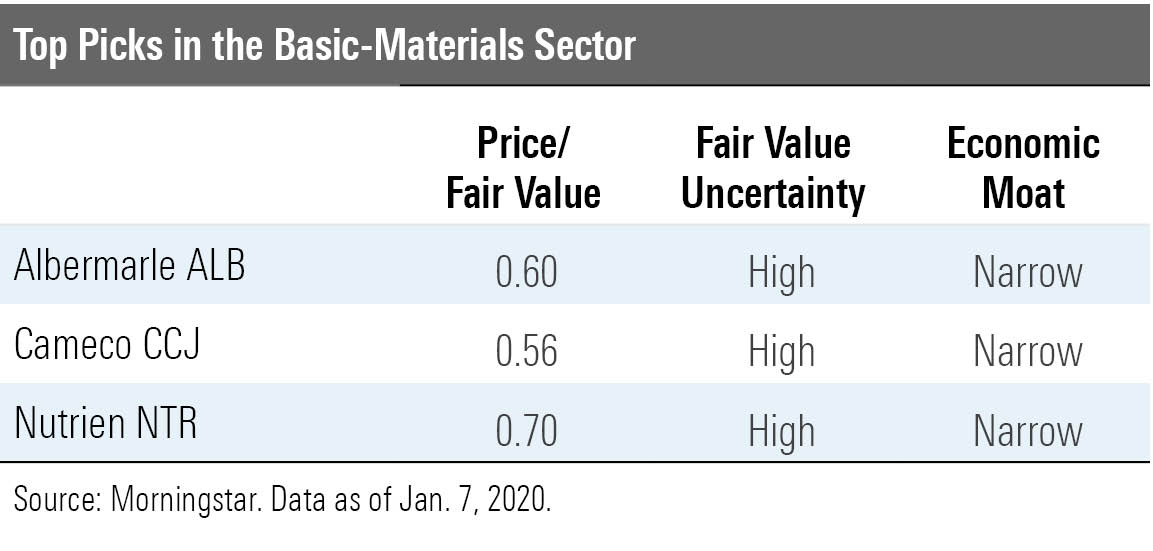

Basic Materials After underperforming the broader market in 2019, about 30% of the basic-materials stocks we cover are trading in 4- and 5-star range, reports director Kris Inton. He points out that the bargains cluster in industries that face what he calls "idiosyncratic challenges."

For instance, potash demand declined in 2019 because of flooding in North America and weak palm oil prices in Southeast Asia; we expect a rebound that'll drive prices up to our long-term forecast of $310 per metric ton. Uranium also took a hit last year, with spot prices falling to $24 per pound; we expect prices to recover to $65 per pound by 2022.

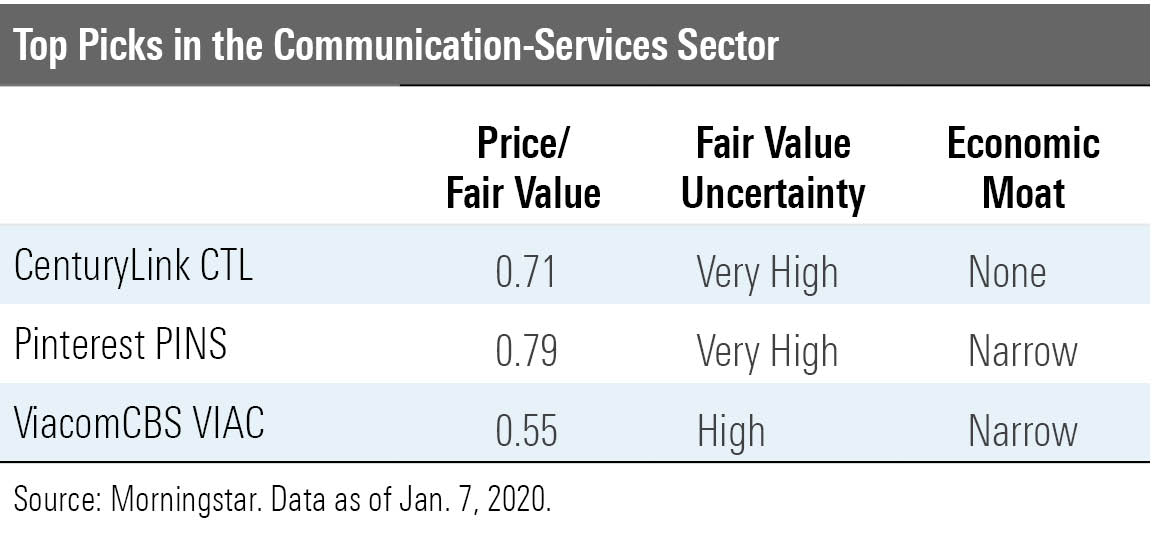

Communication Services The communication-services sector had a stellar 2019. We're not seeing value among the traditional large telecom players, though. Rather, media is the sweet spot of opportunity, says director Mike Hodel in his latest sector report.

"We think that excitement around the looming streaming wars has led some investors to discount the ability of smaller firms to compete," he argues. We, in contrast, think many smaller names are well positioned to benefit as the big platforms seek out differentiated content. We think there's value among smaller names in the Internet content and information industry, too.

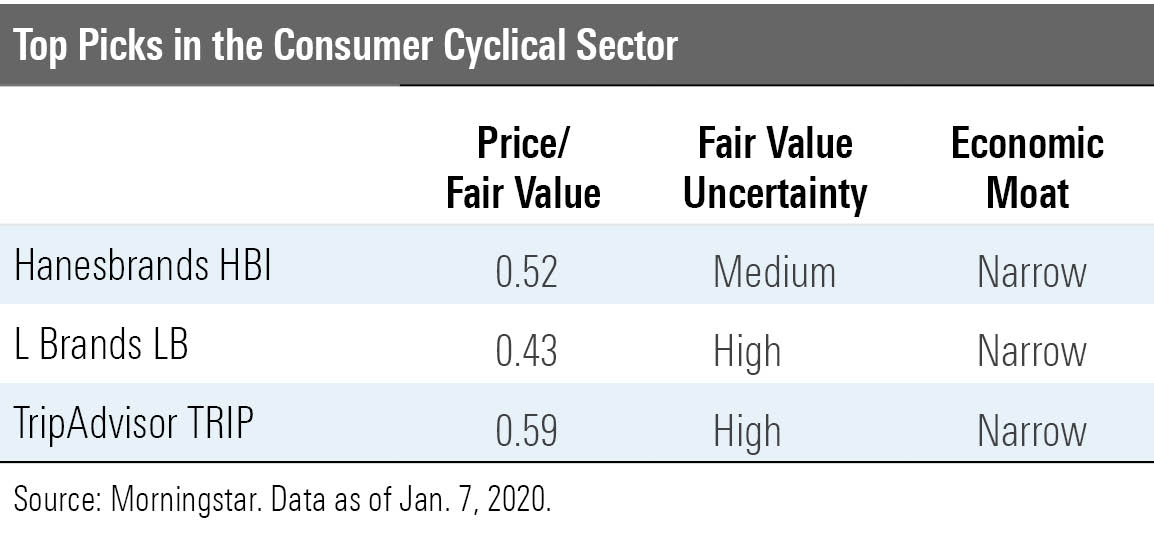

Consumer Cyclical The sector underperformed the broader market in 2019 and finished the year about fairly valued, observes director Erin Lash, with nearly three fourths of the stocks trading at 1-, 2-, or 3-star levels. The packaging industry is particularly overvalued, trading at a 22% premium to our fair value estimates.

Bargain-seekers can find opportunities in the travel and leisure industry. Global uncertainty is plaguing the industry, explains Lash, with many names trading at double-digit discounts to our fair value estimates.

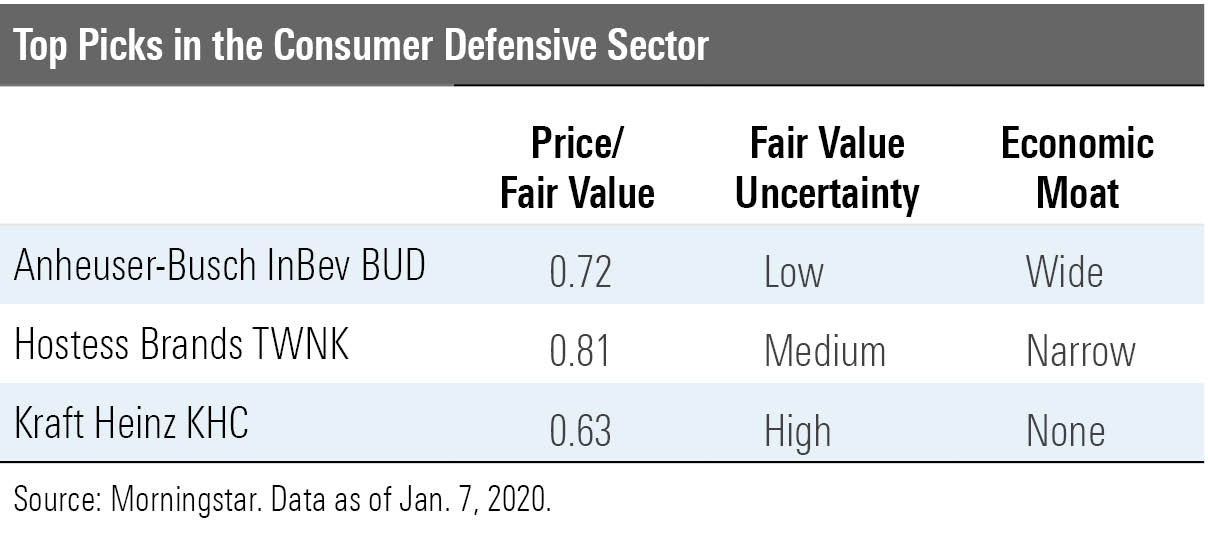

Consumer Defensive The consumer defensive sector is overvalued, reports director Erin Lash: The median stock in our coverage universe is trading at an 8% premium to our fair value estimate. Defensive retail names are especially rich, with the median stock trading at a 20% markup. However, the tobacco and alcoholic beverage industries appear undervalued.

E-commerce remains a key theme in the sector, disrupting manufacturers and retailers alike. Some segments are more resilient than others, however. For instance, we think discount/dollar stores and off-price apparel retailers are less at risk, given that their customers often need to minimize absolute dollar costs--their purchases would be too costly to ship, explains Lash.

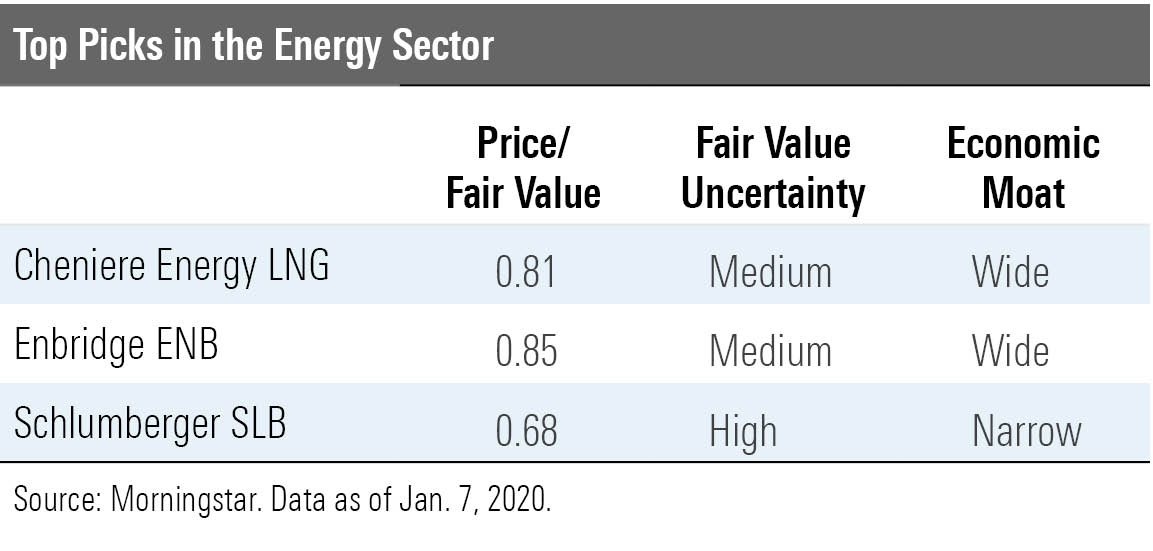

Energy The energy sector is the most undervalued heading into the new year: The median stock in our coverage universe trades at a 10% discount to fair value, says director David Meats in his quarterly wrap-up. Oilfield-services stocks look particularly attractive, trading at a 16% discount to fair value. But we see buying opportunities among all industries.

“We think $55 is the fully loaded cost for the marginal barrel of oil that will balance global supply and demand in the long run, and we expect this marginal barrel to come from a U.S. shale well,” remarks Meats. Moreover, we think the market underestimates the buildout and utilization of U.S. liquefied natural gas export facilities; $2.80 per thousand cubic feet is the midcycle level that we think will induce the right level of activity, he concludes.

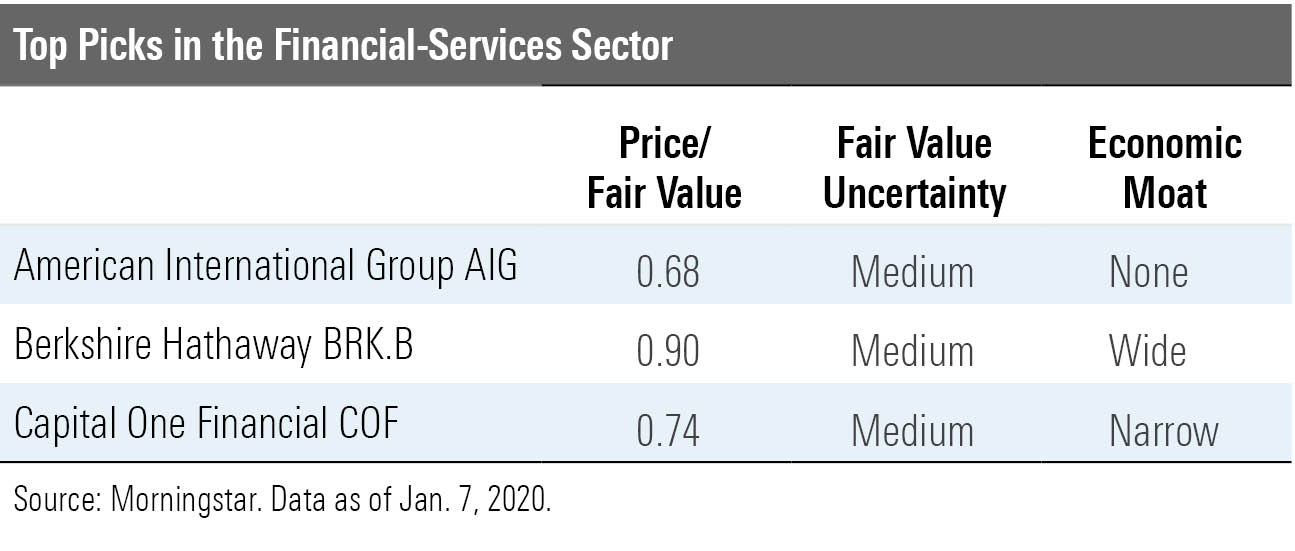

Financial Services Financial-services stocks outperformed the broader market in 2019; the average financial-services stock that we cover is trading at a slight premium to its fair value. That's a stark contrast to one year ago, when many financial-services names were undervalued by as much as 15%, reminds director Michael Wong.

"We believe that much of the outperformance of financial stocks over the previous quarter and year stems from investors having a better sense of the headwinds facing the sector," argues Wong in his quarter-end wrap. "Coming into 2019, many investors were worried about a downturn and how low U.S. interest rates might fall. With the U.S. stock market up about 27% for the year, it seems the market had overestimated the likelihood of a recession in 2019."

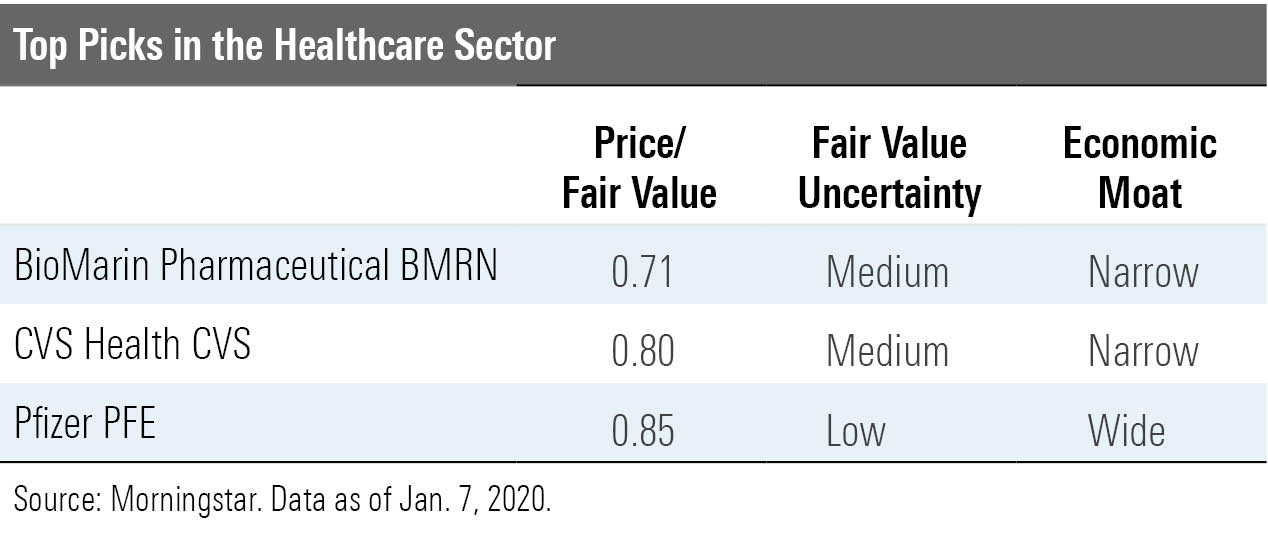

Healthcare Healthcare stocks underperformed the broad market in 2019, yet we think the sector overall is about 5% overvalued today.

"We believe concerns around potential changes in U.S. healthcare policies have become more elevated, with politicians increasing rhetoric for the upcoming presidential election," explains director Damien Conover in his report. "The heightened fears around potential healthcare policy changes have increased the sector's uncertainty and weighed on healthcare's relative performance."

Not surprisingly, there are values to be found in the biotech and drug industries. Although we think that some form of healthcare reform may be on the horizon, a major overhaul is unlikely, asserts Conover. As such, we expect drug pricing power to hold steady.

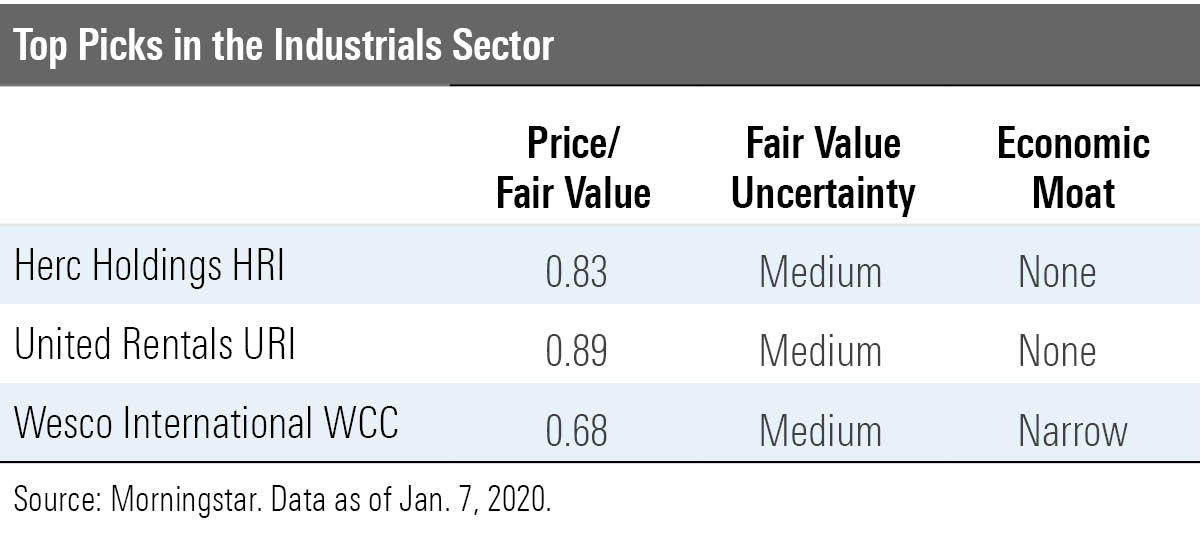

Industrials Despite worries about global economic growth and trade tensions, industrials stocks managed to keep pace with the broad market in 2019. The median stock in the sector is about 6% overvalued, notes director Brian Bernard in his quarterly wrap.

There are some opportunities among stocks in the business-services and farm/machinery industries. Moreover, we view the sector as healthy despite growing concerns of a global economic slowdown, adds Bernard.

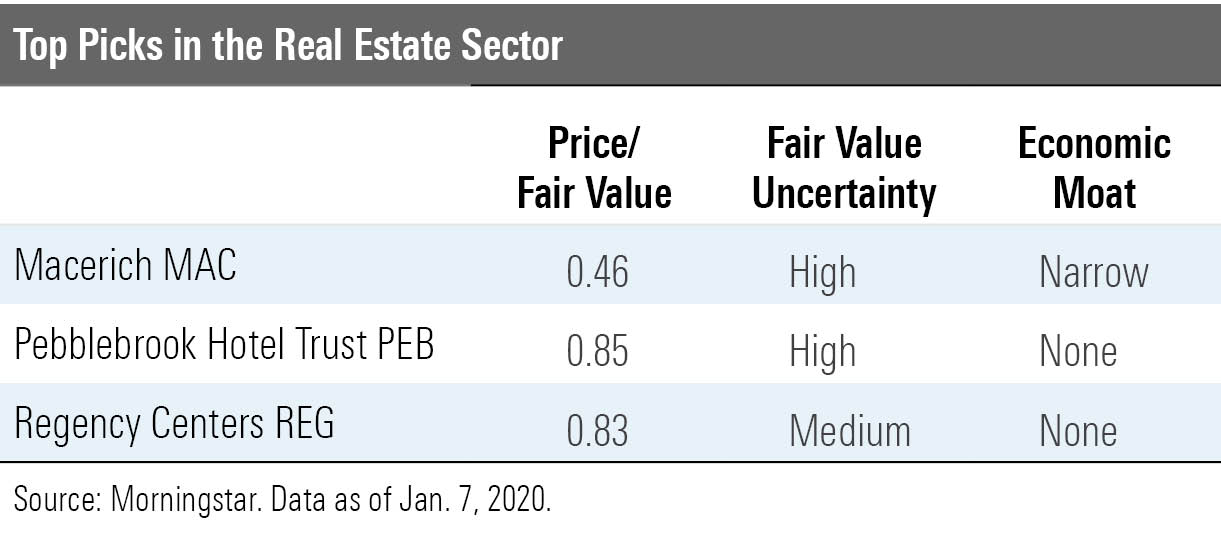

Real Estate Real estate stocks were having a solid 2019 until the fourth quarter: As economic concerns waned, real estate names became slightly less attractive, says analyst Kevin Brown. Nevertheless, the sector remains about fairly valued: The median stock in our coverage universe trades at a 3% premium to our fair value estimates. Malls and hotels present opportunity.

Real estate stocks are notoriously sensitive to interest rates.

"We believe that the relative performance of real estate often mean-reverts during periods of interest-rate stability, and the correlation with long-term performance isn't as strong," explains Brown. "Therefore, we believe investors should concentrate on real estate fundamentals to find companies that will outperform."

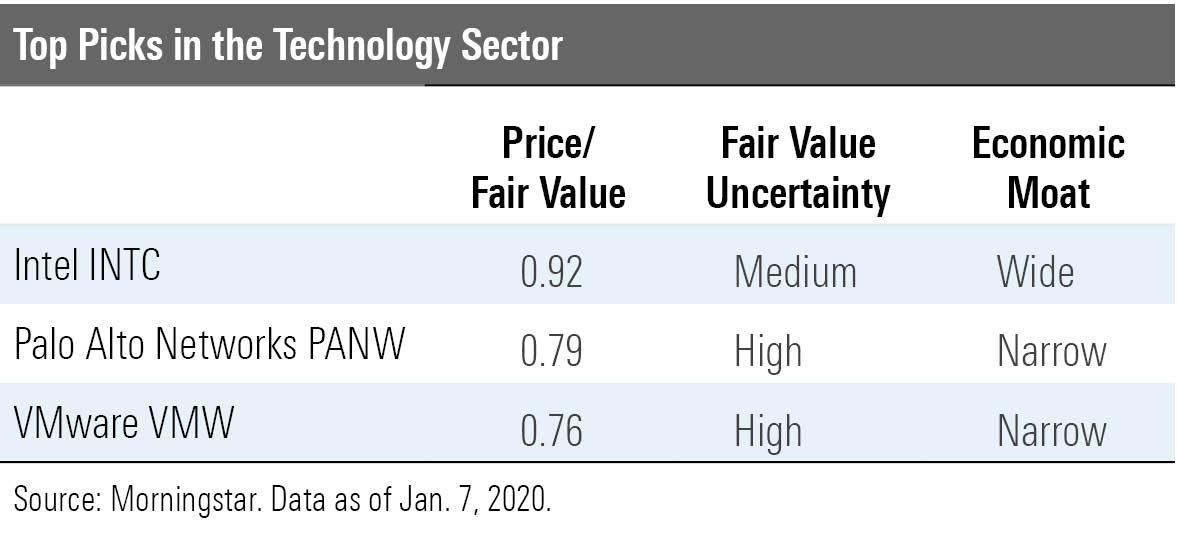

Technology Tech stocks surged in 2019, outperforming the broad market by more than 16 full percentage points. The median technology stock that we cover is 11% overvalued, notes director Brian Colello in his quarter-end report. No subsectors are undervalued, he continues, and semiconductors and software concerns are among the least attractive from a price perspective.

A top trend in the sector remains cybersecurity.

"The cybersecurity vendors we cover have formed economic moats by becoming part of the lifeblood of customers, and we believe the potential disruption associated with changing from these vendors is not worth the risk," maintains Colello. "We think the $100 billion-plus cybersecurity market will grow at a five-year compound annual growth rate of 9%."

Utilities "Utilities head into 2020 flying high," argues strategist Travis Miller. "Perhaps too high." The sector finished 2019 trading at a 16% premium to our fair value estimates.

Indeed, utilities are well positioned with strong balance sheets, secure dividends, and good growth potential, agrees Miller. But we think long-term investors should exercise caution.

“Utilities face fundamental risks besides interest rates,” points out Miller. “Energy efficiency is cutting into electricity and gas demand. Large investment needs require access to capital. Regulatory support could fade if customer bills rise. We think most U.S. utilities can grow earnings and dividends 5% to 7% for several years, but that won’t be enough to sustain 20% annual returns and continued valuation expansion.”

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RNODFET5RVBMBKRZTQFUBVXUEU.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/LJHOT24AYJCHBNGUQ67KUYGHEE.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/V33GR4AWKNF5XACS3HZ356QWCM.jpg)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/35408bfa-dc38-4ae5-81e8-b11e52d70005.jpg)